Uncategorized

Twists and turns in Ecuador and Argentina

admin | December 13, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

An appetite for yield should dominate emerging markets investing in 2020 with particular focus on high beta benchmarks, such as Ecuador and Argentina. Pricing on debt from each of those countries discounts varying probabilities of default and recovery—for Ecuador, whether it averts default, and for Argentina, whether it offers reasonable recovery value. Policy risk looks set to pick up intensity early next year with political transition in Argentina and a legislative calendar focused on economic reform in Ecuador. On those issues, sentiment diverges. Ecuador looks likely to maintain IMF relations and lower debt rollover risks while Argentina struggles to determine a realistic economic plan for debt repayment capacity and recovery value. The right call on each of those should have significant impact on emerging markets returns.

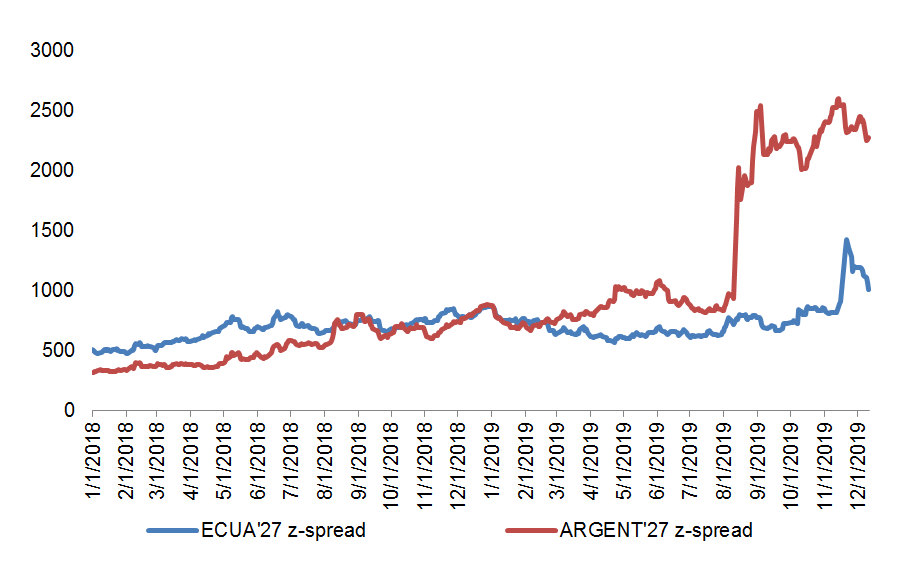

Exhibit 1: The market’s views of Ecuador and Argentina have diverged

Source: Bloomberg Barclays EM USD total returns

Ecuador’s comeback on reform agenda

The economic team in Ecuador is still recovering from the initial shocks of failed implementation of reform. The team met defeat in the legislature on economic reform and defeat in the streets after trying to make subsidy cuts. There is no room for failure on the second attempts. The team pushed through fast track tax reform with further momentum on labor reform, capital markets reform, budget reform and central bank and finance reform. President Moreno also seems determined to deliver on fuel subsidy cuts with sufficient socialization to avoid a repeat of the October protests from indigenous groups and labor unions. It’s telling that a center-left administration endorses orthodox economic reform with broad-based political support to defend economic stability and dollarization. The IMF remains supportive. It has confirmed disbursement of the delayed second and third program tranches and seems flexible so long as there is progress on economic reform. The success on a second round of tax reform reaffirms expectations of legislative support for the reform agenda into next year. This should allow for further normalization of Ecuador’s debt pricing from still-distressed levels.

Argentina’s struggle to determine growth model

Argentina is also entering a new phase after an uncertain and lengthy political transition and is often cited as an important surprise factor for 2020. The question is whether it’s a positive or negative surprise for bondholders’ potential recovery value. There is open discussion of default from budgetary cash flow stress and almost zero liquid FX reserves. The economy suffers from large gross financing needs, insufficient intra-government financing, informal suspension of IMF relations and chronic capital flight with almost zero liquid foreign exchange reserves. There has already been a forced maturity extension of local treasury bills. Argentina continues to prioritize liquidity relief as the outgoing Macri administration has been forced to rely upon direct monetization from the central bank. There are huge challenges ahead for the Fernandez administration. The new economic team will set the context for recovery value. It’s hard to expect pragmatic reform when the economic team reflects ideological loyalty to Kirchnerismo. If Kirchnerismo discourages growth through foreign direct investment and refuses to cut back spending entitlements necessary for a primary fiscal surplus, what provides the future savings for debt repayment?

Argentina can either convince the 75% majority of bondholders to voluntarily “extend and pretend” and forfeit debt service for two years to five years or shift toward a pragmatic stance and embrace the pension reform necessary for a structural primary fiscal surplus. Neither of these scenarios seems likely. If the IMF doesn’t endorse debt re-profiling, then it would discourage bondholder participation in re-profiling debt and discourage the IMF to re-profile their loans. The bondholders may be motivated to seek some compromise that averts a haircut on capital; however the IMF as a creditor would be less flexible and would likely insist on the debate between haircut and/or primary fiscal surplus to reassure for their own repayment. There is still a potential compromise solution with flexibility from creditors; however this requires pragmatism from the Fernandez administration. The recovery value of 50% to 55% remains the compromise scenario under a successful negotiation.

Third time’s a charm on relative performance?

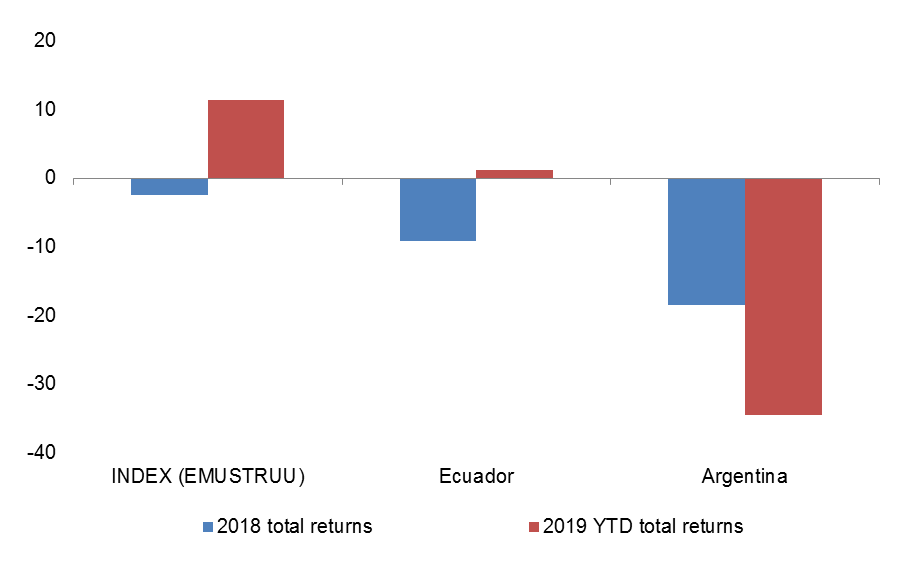

Despite a strong start to the year for each year in 2018 and 2019, both Argentina and Ecuador have again been the worst EM performers. The current distressed prices for Argentina provide some technical support. There is reluctance to sell near historical recovery value of $40 and expectations that the Fernandez administration will avoid a large debt haircut and likely litigation backlash. However, attractive risk/reward only starts at pricing closer to $30 in light of difficult (IMF) creditor negotiations, the large gross financing needs and the uncertain debt repayment capacity. The alternative scenarios that argue for recovery value closer to $50 to $55 are either convincing the 75% majority of bondholders to “extend and pretend” for a few years or shifting towards a pragmatic stance and embracing the pension reform necessary for a structural primary fiscal surplus. These are low probability scenarios. The bottom line is that current market prices are vulnerable to high execution risk and pessimism that weak economic growth and weak commitment to fiscal discipline will constrain debt repayment and argue for a haircut on external debt.

Exhibit 2: Ecuador and Argentina have underperformed broader EM

Source: Bloomberg Barclays EM USD total returns

Prospects for Ecuador look better with solidarity for fiscal consolidation and flexibility from the IMF as progress continues on the economic reform agenda. This momentum should continue into early 2020 with submission of more reform bills, progress on fiscal consolidation, cutbacks in current spending and revenues from the asset monetization program. This should allow for normalization from the current curve inversion with 10-year benchmark bonds gradually recovering back to 10% from current levels near 12%.

The surprise risk for next year should focus on the distressed credits as an important influence for EM returns, especially considering the compressed spreads and difficulty of repeating the impressive 12.8% year-to-date EMBIG-D returns. On the approval of tax reform, Ecuador should maintain IMF relations that are critical for liquidity and rollover risks. Argentina looks likely to struggle in its IMF relations next year as debt negotiations commence to seek relief from cash flow stress from creditors.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.