Uncategorized

A shift in bank supply and foreign demand

admin | December 13, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

Momentum from a strong year in corporate debt looks likely to roll into 2020. A tighter supply of bank debt and a shift in foreign demand, especially for ‘BBB’ exposures, could shape returns for some sectors of the market.

A drop in net supply of bank debt

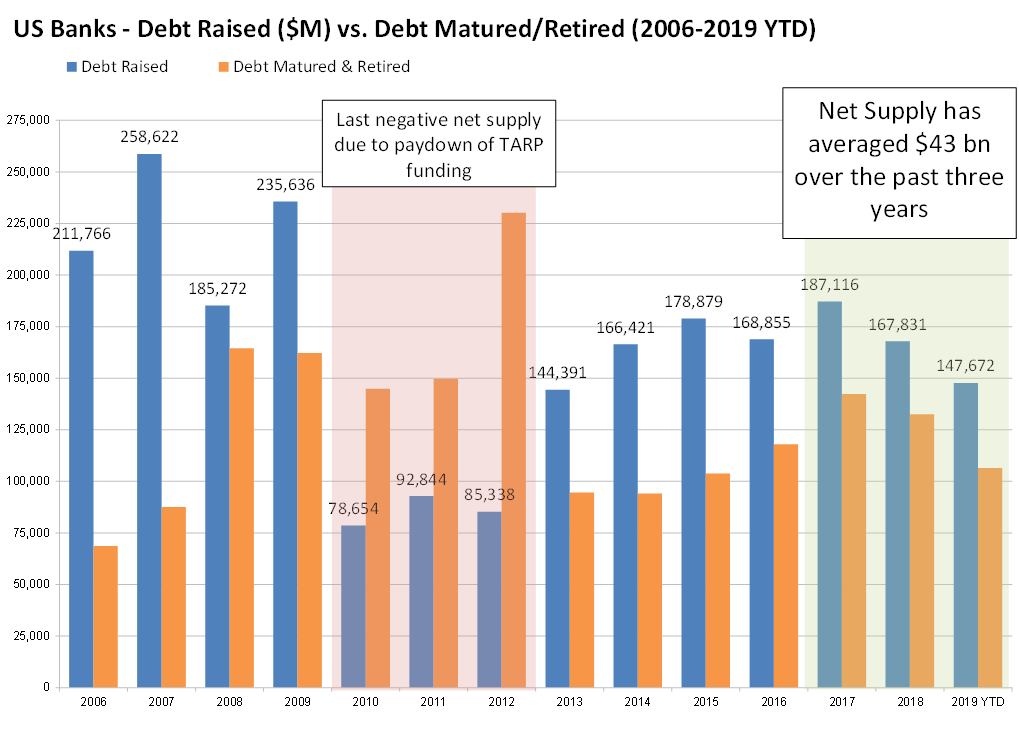

Banks represent 22% of the investment grade corporate index, with the bulk of that volume coming from the Big 6 domestic money center banks—JPM, WFC, BAC, C, GS and MS. The segment has had significant influence over total investment grade volume for the past decade, as the largest banks continue to recapitalize globally to meet revised regulatory standards such as Dodd-Frank, Basel III, TLAC/MREL, and so on (Exhibit 1).

Exhibit 1. US banks have been providing consistent excess net supply since 2013

Source: Amherst Pierpont, S&P Global Market Intelligence (SNL)

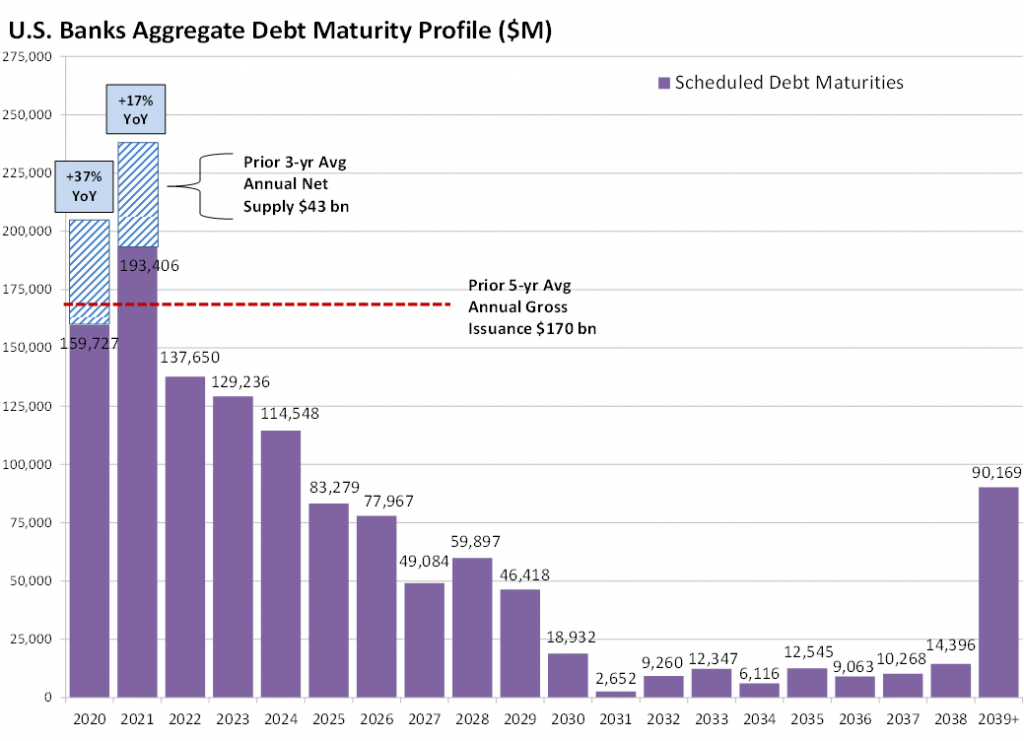

With domestic TLAC rules now effective, all the major money center banks are positioned with excess regulatory capital entering 2020. With domestic banks facing a sizable maturity wall over the next two years, net supply in the segment stands a good chance of falling off substantially compared to recent years and possibly even move to a net negative position in USD paper in the coming year or beyond (Exhibit 2). Banks have worked to term out maturing debt ahead of schedule. In order to match the average net supply of the three prior years, US banks would need to see a 37% increase in gross issuance in 2020 and 17% in the following year.

Exhibit 2. US banks will likely fall short of recent net supply

Source: Amherst Pierpont, S&P Global Market Intelligence (SNL)

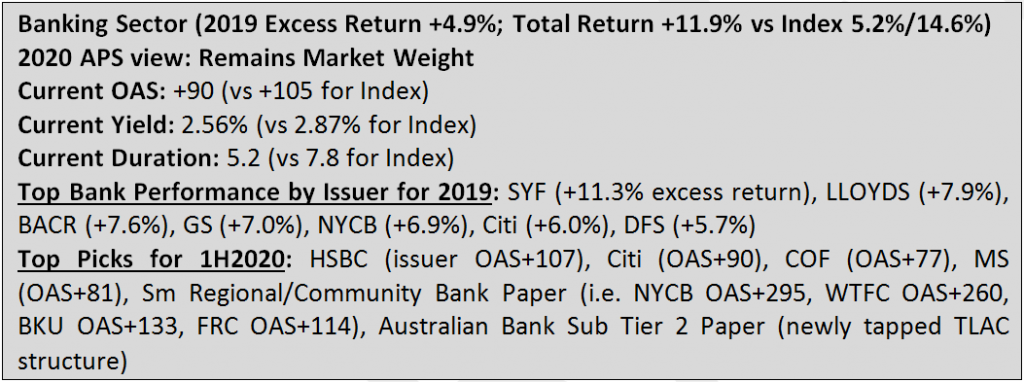

A near-term reduction in net supply should lend support to spreads in the sector, even if IG paper sees limited spread compression and muted returns in 2020 following the tremendous performance throughout 2019. Nevertheless, investors should keep banking sector exposure at a market weight to start the year reflecting a number of considerations:

- The overall tightness of spreads in the sector (current OAS +90 vs +103 for the Index), particularly among the increasingly scarce regional banks;

- Increased relative supply from Yankee banks that are still in earlier phases of their own recapitalization processes, bringing new structures of Senior Non-Preferred (Tier 3) or Tier 2 (mostly AU) TLAC-eligible debt; and

- That there still remains a steady stream of gross issuance among US issuers to meet near-term maturities that will limit scarcity value in the earlier months of the year, as banks have been stacking a large portion of their annual issuance in the first four months.

- The 2020 election uncertainty with regard to bank regulation; as the past three years have been seen as extremely favorable (more so from an Equity standpoint than credit) with regard to banks having more flexibility and less onerous regulatory requirements. We inherently see more stringent application of bank regulations and capital requirements as a longer-term positive to Bank credit quality, but recognize that the near-term (and share prices) is often more influenced by perceptions that looser regulations bolster profitability/returns.

SUMMARY:

An eventual shift in foreign demand argues for a defensive ‘BBB’ strategy

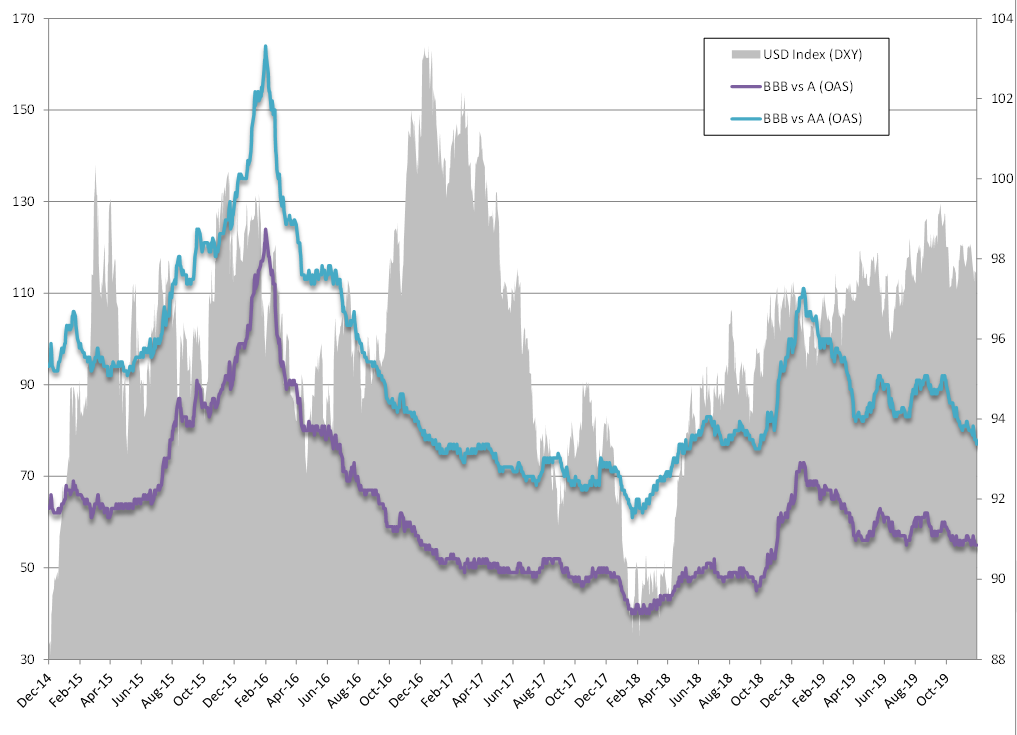

One of the main contributors to the performance of corporate bonds over the past several years has been the increased demand from investors outside the United States. Global investors have been seeking additional yield and the relative strength of the US dollar amidst the endless onslaught of central bank easing (Exhibit 3). This trend has not only driven spreads tighter throughout most of the past decade, but also enabled corporate issuers to access record amounts of funding, driving a greater portion of aggregate credit quality of the IG universe into lower-rated categories (BBB). A big part of that trend has been facilitated by the vast amount of available capital at insurance companies in the Asia/Pacific region (Exhibit 4). Regulators in those areas have also facilitated the trend by easing controls and allowing their local operators to invest larger amounts in lower-rated credit.

Exhibit 3. BBB to A/AA corporate spreads against the USD index

Source: Bloomberg LP, Bloomberg Barclays Corp Agg Index

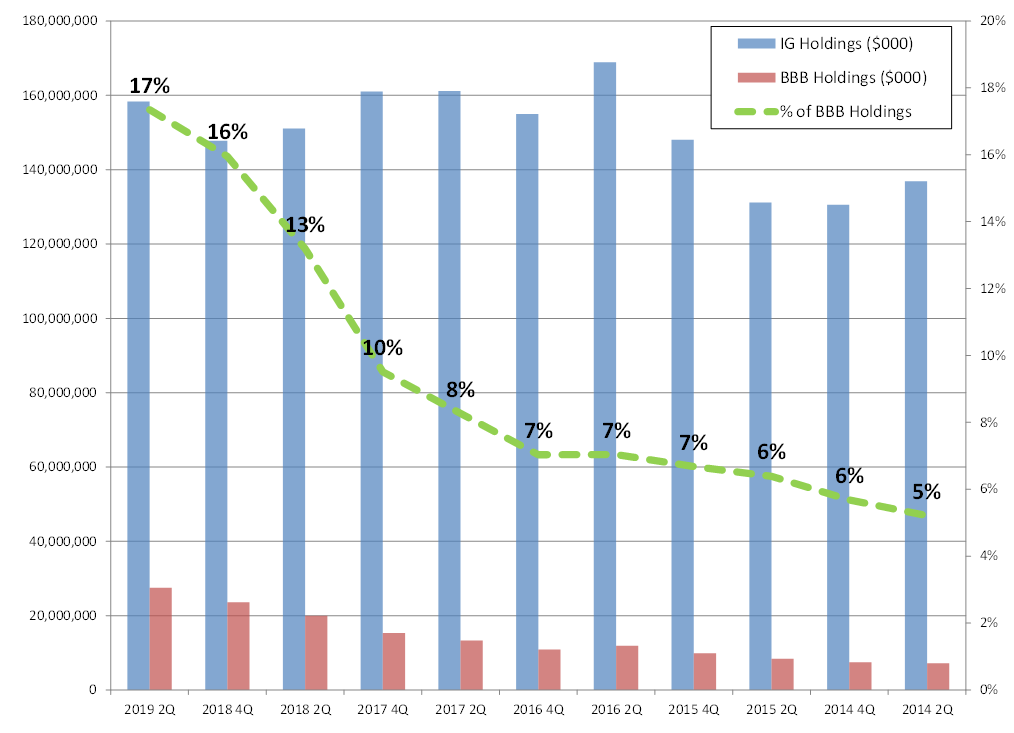

Exhibit 4. Asia/Pacific insurance has helped drive demand for ‘BBB’ credit

Note: Using the second largest Insurance company (Nippon Life – $691 bn in Total Investments) as a proxy for recent trends in Corp credit amongst operators in Asia/Pacific, the investment portfolio demonstrates a dramatic uptick in BBB credit holding relative to total IG investments.

Source: Amherst Pierpont, S&P Global Market Intelligence (SNL), Nippon Life Company Filings

These trends should largely continue into 2020, with foreign insurance companies maintaining heightened demand for USD credit and preference for higher-yielding instruments. However, given the relative tightness of spreads and the breakneck performance in corporates in 2019, foreign insurance companies could continue to ease up their allocation to the asset class. Furthermore, as large portions of USD corporates are held by Asian insurance companies on an unhedged basis—a de facto play on a strengthening US dollar—concerns about the lack of inflation and stubbornly low rates could cause some global investors to reassess or at least ease off their more aggressive allocation to the US corporate bond sector on an unhedged basis. None of these factors appear to portend an immediate near-term back-up in spreads, but could contribute to a more passive environment for corporate debt and the prospect for more muted returns in 2020. As ‘BBB’ spreads move closer to historic tights versus their ‘A’ and ‘AA’ counterparts, justification for more defensive trading strategies could be only several months away and a prevailing strategy for the majority of the coming year.

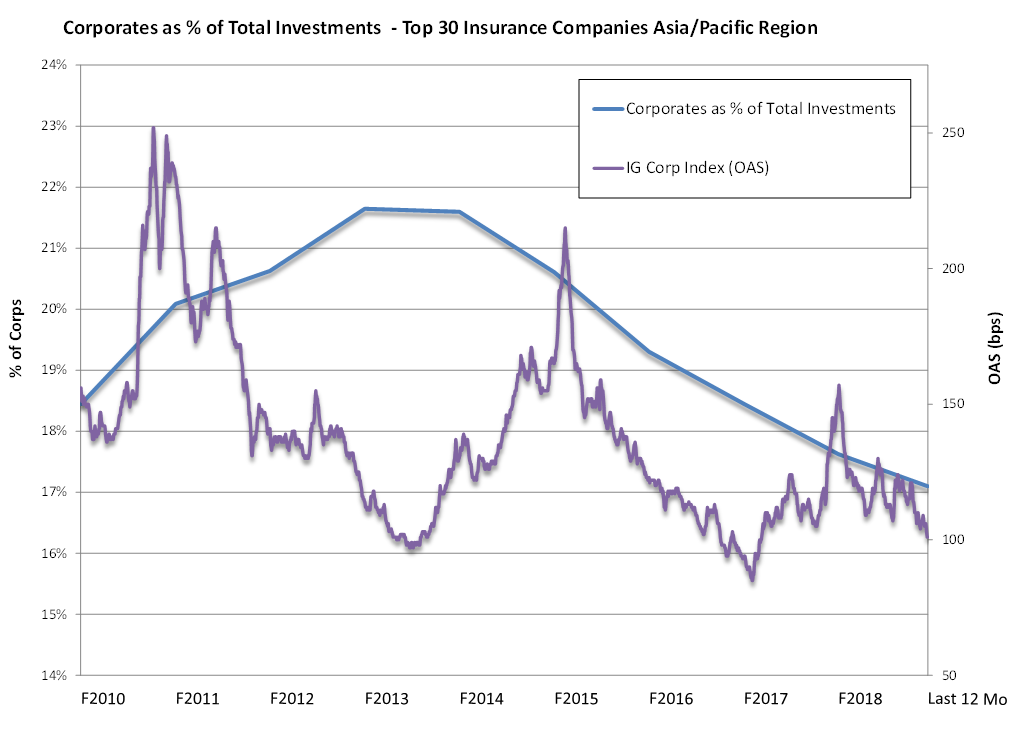

Exhibit 5. Insurers have trimmed corporate exposure as spreads have tightened

Note: Insurance Companies in the Asia/Pacific Region have had increased appetite for USD spread product and available yields in the Corporate Bond market; but have demonstrated some sensitivity as spreads (and available overall yields) have compressed.

Source: Amherst Pierpont, Bloomberg Barclays Corp Agg Index, S&P Global Market Intelligence (SNL) – data based on availability in individual companies’ corporate filings over the demonstrated period

The underlying consensus

This year has been a banner year for corporates, with the IG Index delivering among the best returns in risk assets with Total Return of over 14% (tracking to 15% annualized) and excess return over Treasury debt of more than 5%. This represented the second highest performance in the past 20 years, only falling short of the more than 18% return generated in the year immediately following the height of the Financial Crisis. The favorable environment for credit helped stoke more new issue supply than the market had anticipated, particularly among high yield and lower-rated IG issuers, who pounced on the ideal atmosphere to access funding. Through the first 11 months of 2019, the investment grade market has brought roughly $1.22 trillion in USD debt, just around 5% below last year’s $1.25 trillion and likely to close flat on a gross basis, with the supply net of maturities likely to fall in the mid-to-low $400 billions for the year.

High grade issuance struck a particularly opportunistic tone in the second half of the year. The market saw less required or M&A funding outside of the $30 billion ABBV deal and instead saw yet another round of balance sheet engineering deals. Deals tied to early tender offers, redemptions and pre-funding maturities further out the curve increased considerably throughout the closing months of 2019. With that in mind, we think 2020 will likely bring the significant decrease in net supply that much of the market had been anticipating for this year. There are currently no sizable M&A deals in the queue for the IG market; and while several sectors still appear poised for further consolidation, strategic M&A could be topping out in other areas within the IG sector.