Uncategorized

King County Housing Authority seeks to expand affordable housing program

admin | October 18, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

Building or preserving affordable rental housing in high cost urban areas has become a primary focus for many state and local housing authorities. King County Housing Authority in Seattle, with $60 million of funding provided by Microsoft, recently used eminent domain and negotiated sales to acquire five multifamily properties in an effort to protect and retain affordable housing stock for low- to moderate-income renters. There is another $165 million of funding commitments from Microsoft which could potentially be deployed for similar purchases. In minutes from a recent board meeting, KCHA indicated they would like to expand the program to other corporate partners. Workforce housing has long been supported by Freddie Mac and Fannie Mae. The footprint of exposure is fairly well defined in King County, though future programs or adoption of the strategy by other jurisdictions could increase reverberations for agency CMBS investors.

Agency support for workforce housing

The multifamily housing programs of Freddie Mac and Fannie Mae have long been committed to promoting rental housing affordability for low- to moderate-income workers and families. Workforce housing can be found everywhere, but is often concentrated in urban areas or in surrounding communities of employment centers. Freddie Mac characterizes workforce housing on its website as:

- Privately-owned and -operated properties, with limited amenities.

- Affordable to renters with lower incomes, for example firefighters, teachers, service and hourly wage workers, and young families.

- Any property type but most often garden style.

- Typically at least 15 years old.

Freddie states that the sector is important because:

Around half of all renters are cost-burdened, meaning that they spend more than 30 percent of their income on housing. The burden is much heavier for many lower-income households. And when more of their income must go toward housing, they have less to spend on other necessities – like food, clothing, and health care – let alone to save or to spend elsewhere

So, while we’ve always supported affordability, housing for this part of the population has become more of a focus for us. And the Federal Housing Finance Agency (FHFA), our conservator, agrees. Much of our funding for workforce housing is excluded from the purchase-volume cap that FHFA sets for us each year. We’re proud to support renters nationwide, and to help improve their quality of life.

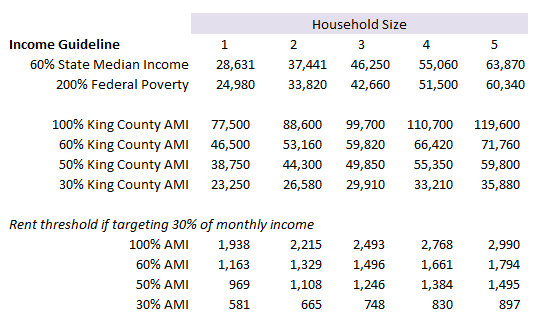

Workforce or affordable rental housing is typically defined based on the area median income (AMI) in conjunction with household size (Exhibit 1). A benchmark of 60% to 100% of AMI is often used as a proxy for moderate-income households, where affordability is targeted as approximately 30% of monthly income covering rent.

Exhibit 1: Area median income and approximate rent thresholds for affordable housing in King County

Note: State and area median income data by household size from KCHA. Rent thresholds calculated by Amherst Pierpont Securities assuming 30% of monthly income is spent on rent. Rent-burdened households as those that spend more than 30% of their monthly income on rent. Source: KCHA, Freddie Mac, Amherst Pierpont Securities

Acquisition of the first five properties by KCHA was completed in September 2019. As announced in Seattle Times article, this was financed partially through a grant from Microsoft (excerpt below, emphasis added):

The funding includes $60 million loaned to the housing authority from Microsoft, $20 million from King County and $140 million in bonds from the housing authority. The partnership is among the first originating from the Redmond tech giant’s $500 million pledge announced earlier this year to address homelessness and develop affordable housing throughout the region.

This project is part of Microsoft’s focus on the middle-income population, or those earning between $60,000 to $120,000 a year, aid Jane Broom, senior director of Microsoft Philanthropies, and the company’s belief that communities should have people at all income levels and job categories, said Jane Broom, senior director of Microsoft Philanthropies. Microsoft said it would loan $225 million to help developers facing high land and construction costs build and preserve “workforce housing” on the Eastside.

In King County, a family of 5 earning $120,000 per year is consistent with 100% AMI and could support $3,000 per month for affordable rent.

King County looks to expand affordable housing program

The King County Housing Authority (KCHA) had a board meeting on Monday, October 14th, 2019. At that meeting they released the minutes from the September board meeting where they discussed future acquisition strategies – presumably for more low- to moderate-income multifamily properties – based on the financing received from Microsoft.

Excerpt from Minutes of KCHA Board Meeting, September 14th, 2019, edited for brevity, emphasis added (page 5 of 6 as numbered, page 8 of 185 in packet):

EXECUTIVE DIRECTOR REPORT

We are working on finalizing the permanent financing for this year’s acquisitions. … The two remaining moving pieces are getting the bonds to market quickly to take advantage of the current rate environment, and concluding negotiations with the Microsoft Corporation. We are optimistic that this is moving in the right direction. We will know in the next two weeks as to whether we have a deal with Microsoft. We have asked them for “concessionary” capital that will provide gap financing for acquisition debt not covered through project cash flow.

If we are successful with Microsoft, the next challenge will be to develop a strategy for marketing this model beyond Microsoft. This is where we will circle back to the Commissioners to discuss future acquisition strategies and for advice and contacts in the corporate community as we work to make this model replicable.

For an overview of how the recent acquisitions of multifamily properties from use of eminent domain in King County have impacted the agency CMBS market, please see the recently published piece in APS Portfolio Strategy, Assessing risk from use of eminent domain.

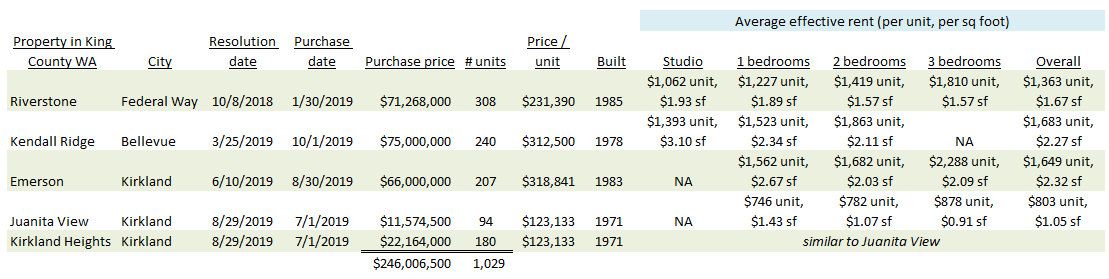

Of the properties already acquired by KCHA (Exhibit 2), three fall clearly into the moderate-income workforce housing sphere based average effective rents – there Riverstone, Kendall Ridge and Emerson apartments. Not surprisingly, the loans for all three were in Fannie DUS pools or Freddie K-deals. The Juanita View and Kirkland Heights properties have rent levels more consistent with low-income housing. Both of those properties were acquired via a negotiated sale as part of a portfolio. If there were outstanding loans on the properties they were not in agency securitizations.

Exhibit 2: Properties recently taken by eminent domain or negotiated sale by King County Housing Authority

Note: The Riverstone, Kendall Ridge and Emerson apartments were all taken by eminent domain; while the Juanita View and Kirkland Heights properties were acquired in a negotiated sale. Source: KCHA, CoStar, Amherst Pierpont Securities.

The footprint of exposure in agency CMBS

There is $5.1 billion of exposure in Fannie DUS pools and $3.8 billion in Freddie K-deals to multifamily properties in King County. Those gross exposure numbers don’t take into account the rather clear affordability footprint that KCHA is targeting for workforce housing, the relative proximity to transit, or the loss of affordable housing due to escalating rents and presumably gentrification in specific neighborhoods. The reasoning is outlined in their resolution authorizing acquisition of Kendall Ridge Apartments, one of the apartment complexes it took via eminent domain. Each of the resolutions targeting a property has virtually identical language.

There is an increasingly serious shortage of affordable housing in King County, which the King County Housing Authority is charged with addressing pursuant to its mission of providing quality affordable housing opportunities equitably distributed within King County; and

It is a goal of local government and the Housing Authority to further fair housing in the region affirmatively, in part through preservation of existing affordable housing opportunities in areas with significantly appreciating housing costs; and

Kendall Ridge Apartments is a 240-unit apartment complex located at 15301 NE 20th Street, Bellevue, Washington, in an area of King County where rents are increasingly unaffordable to low-income households.

- Rents at the Property are expected to continue to escalate, making the Property and Bellevue increasingly less affordable to low income households;

- There is a growing loss of affordable housing within transit corridors and around light rail stations in King County;

- Access to reliable public transportation is a critical resource for low income households, providing access to work, services, school, shopping, cultural and other activities for these residents;

The Housing Authority has identified acquiring and developing housing along planned mass transit corridors and areas with frequent high capacity transit as a strategic priority to ensure the long-term availability of low-income housing near reliable public transportation; and

The Property is located within a transit corridor and close to light rail where rents are increasingly unaffordable to low-income households;

Acquisition of the Property by the Housing Authority will serve the mission of the Housing Authority and the housing goals of the region through an approach that is considerably less expensive than constructing the same number of new housing units.

Unfortunately there is not a robust way to screen the agency exposure for the rather narrow footprint of multifamily housing that KCHA appears to be targeting at this time. Moreover, Microsoft’s initial financing round of $60 million has been exhausted, though that amount was only a partial use of a larger $225 million commitment, leaving $165 million of funds if all of them are dedicated to preserving workforce housing instead of new building. Also, KCHA clearly intends to try to raise more money to fund the program from other corporate sponsors. Agency CMBS investors are encouraged to monitor their holdings for King County loans, in conjunction with the affordability criteria outlined above.