Uncategorized

Argentina | Restructuring simulations

admin | October 18, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

The debate about liquidity and solvency relief in Argentina should begin soon after elections. And the Uruguay debt restructuring of 2003 will likely offer a roadmap. It was offered under friendly terms with a menu of either a 5-year maturity extension or a benchmark bond. There was no explicit haircut on capital and liquidity relief came from some combination of terming out maturities and partial interest capitalization. Participation was high. But it is unclear whether the incoming administration in Argentina can follow the Uruguay map.

The high participation rate for Uruguay relied on a 90% minimum threshold requirement, exit consents and relatively friendly terms. It came against a track record of effective policy management and an investment grade credit. The context for Argentina is quite different with collective action clauses a substitute for other coercive tactics and much higher uncertainty on debt repayment capacity. That should imply higher exit yields post restructuring under the friendlier scenarios. It’s still an active debate about illiquidity versus insolvency and whether a Fernandez administration credibly can commit to medium-term debt repayment capacity. There is a clear tradeoff between fiscal discipline and debt relief as we await the post-election discussion on whether the Fernandez administration reaffirms the Uruguay restructuring terms.

Our simulations somewhat replicate the menu for Uruguay with a 5-year maturity extension as well as 4-year partial interest capitalization (PIK’33) against the opposing scenario of an additional 30% haircut on principal. The exit yields are a critical determinant for recovery value with a range of 10% to 12% the most realistic under the assumptions of policy moderation as opposed to the alternative reformist policy bias that would normalize yields. It’s also important to assume more aggressive liquidity relief with interest accrual for the large gross financing needs and limited access to capital. This argues for not just maturity extension but also partial coupon accrual (similar to the PIK’33 Uruguay benchmark bond alternative or the Argentina Discount bond). There are clear relative value considerations, though we caution that campaign promises may adjust under the reality of the economic crisis post elections which could then argue for notional haircut. This shifts our investment strategy towards risk/reward options under various alternatives with an emphasis that friendly/unfriendly scenarios are more relevant for determinant of total returns. Our preference is for the ARGENT’26 and ARGENT’36 for the combination of relatively low cash prices/higher coupons that offer potential for relative outperformance under binary scenarios.

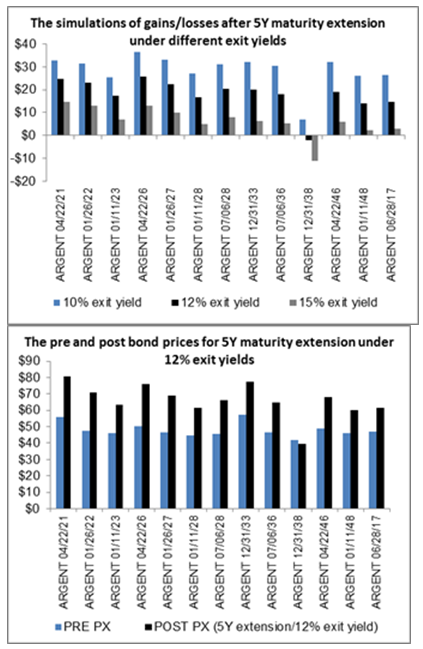

Exhibit 1: Argentina debt simulation – 5-year maturity extension

Source: Bloomberg and Amherst Pierpont Securities

Scenario: a 5-year maturity extension

The 5-year maturity extension scenario is the most friendly but least likely if we assume only a moderate as opposed to reformist Fernandez administration. This would also require a slightly higher exit yield of 12% on the uncertainty of medium term debt repayment capacity. There would be almost universal significant upside across the curve with the exception of the Par bond under the constraint of the low coupon/longer maturity. It’s still not clear how officials would treat the Par/Discount bonds as they were not initially targeted for restructuring; however it seems difficult to legally exclude these bonds on a selective default basis. The best risk/reward skews towards the shorter tenors with the highest coupons with perhaps the ARGENT’2026 more attractive versus the high cash price of the ARGENT’2021. There should still be core preference for lower cash price bonds on the uncertainty at an early phase with high mark to market risks. We do not expect a scenario similar to PdVSA (2015-2017) when Venezuelan authorities remained current on debt service much longer than expected with pull to par of the shortest tenors. There is a pre-emptive bias to quickly seek liquidity relief against the precarious liquidity ratios of low net FX reserves. The treasury cashflow stress suggests difficulty on remaining current until the April 2021 amortization. Our bias remains for the higher coupon bonds at similar cash price to similar maturities for the outperformance to the upside in Uruguay restructuring scenarios (ARGENT’36 versus ARGENT’46).

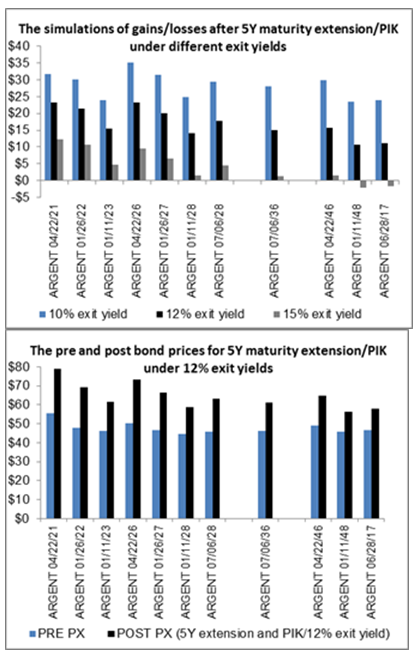

Exhibit 2: Argentina debt simulations – 5-year extension with partial interest capitalization

Source: Bloomberg and Amherst Pierpont Securities

Scenario: 5-year maturity extension and partial interest accrual

The more realistic scenario assumes more aggressive liquidity relief through partial interest capitalization. If we simulate cashflow similar to the Uruguay’33 PIK then this allows for gradual increase in cash coupons over 4 years as well as a 5Y maturity extension. There are near infinite different combinations though the concept is to seek some reasonable interest relief via both coupons and maturities (and we exclude the Par and Discount bonds for their unique characteristic of interest accrual and low coupons that further complicates under this scenario). There are still potential significant upside gains across the curve under a similar 12% exit yield again biased towards the shorter tenors but the ARGENT’26 still offering the best risk/reward.

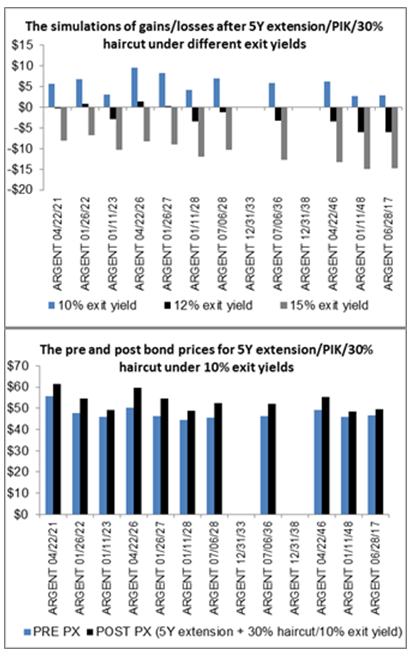

Exhibit 3: Argentina debt simulation – 5-year maturity extension with partial interest accrual, 30% haircut

Source: Bloomberg and Amherst Pierpont Securities

Scenario: 5-year maturity extension, partial interest accrual, 30% haircut

It becomes increasingly complicated if the debate shifts from liquidity to solvency relief; however the potential for a lower exit yield of 10% would fully offset a theoretical 30% haircut on principal. This could argue for a bullish overall investment strategy for potential upside under some reasonable scenarios of a moderate haircut on principal as well as liquidity relief on interest accrual and maturity extension. There are less relative value considerations under this alternative with the shorter tenors more vulnerable and the intermediate sector of the curve still offering the best risk/reward with positive returns dependent upon a near normalization in exit yields to 10% (similar to Ecuador) for the solvency relief post restructuring and average recovery values above 50. This is the closest to a breakeven scenario that would still suggest upside from current prices with an optimistic 10% exit yield on the assumption of a somewhat stable muddling through scenario on policy management.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.