Uncategorized

Aircraft lessors provide compelling spread versus IG corporates

admin | October 11, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

Finance Companies have topped the Bloomberg Barclays IG Corp Agg Index year-to-date with 6.18% excess return versus +3.39% for the Index, second only to Gaming (+6.87%) and Wirelines (+6.28%). BBB-rated Aircraft Lease company 7- to 10-year paper has produced excess returns of roughly 9-11%, with roughly 6-8% from 5-year paper.

Aircraft lease bonds outperformed as concerns about the fallout of safety issues with Boeing’s 737 Max aircraft have tempered over the past several months, and operators produced several quarters of strong operating results with good industry dynamics for growth going forward. For the lessors, subsequent cancellations of 737 Max orders are likely to be offset with new orders for similar, competing aircraft. Recent pricing pressures at major domestic airlines are offset by continuing strong demand for new aircraft and fleet needs of international carriers.

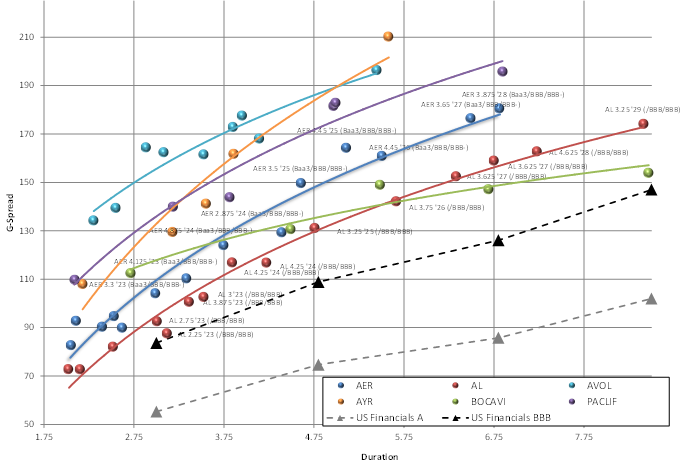

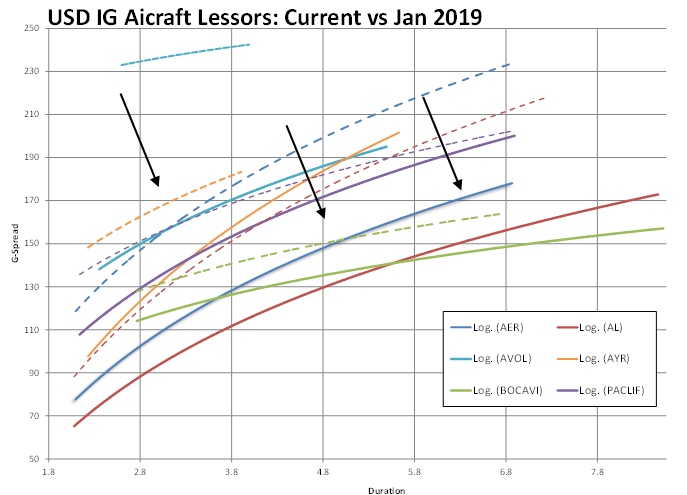

A snapshot of current spreads (Exhibit 1) show that IG aircraft lessors still offer yield/spread pick-up to the broader financial segment. Higher quality lessors, such as Air Lease (AL), offer roughly ~25-30 bp of spread pick-up to aggregate BBB Financials. Curves also offer good relative steepness in intermediate paper compared to most finance credits. Fundamentals are currently very constructive in the aircraft leasing industry, as backlogs remain robust and supply/demand dynamics are favorable to the financiers. Spreads have tightened sharply year-to-date, particularly since April as Boeing fears subsided (Exhibit 2).

Exhibit 1: IG Aircraft Lessors

Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

Air Lease (AL: BBB/BBB; KBRA A-) is an industry bellwether, with the youngest fleet (average age <4 yrs), and one of the industry’s larger lease portfolios (~320 aircraft, with commitments for 343 more for $24 billion as of 2Q19). The Air Lease management team includes industry icons Steven Udvar-Hazy and CEO John Plueger, the former of which originally founded ILFC and more or less created the industry.

Spreads have tightened sharply year-to-date, particularly since April as Boeing fears subsided (Exhibit 2).

Exhibit 2: IG Aircraft Lessors – current spreads vs beginning of the year

Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

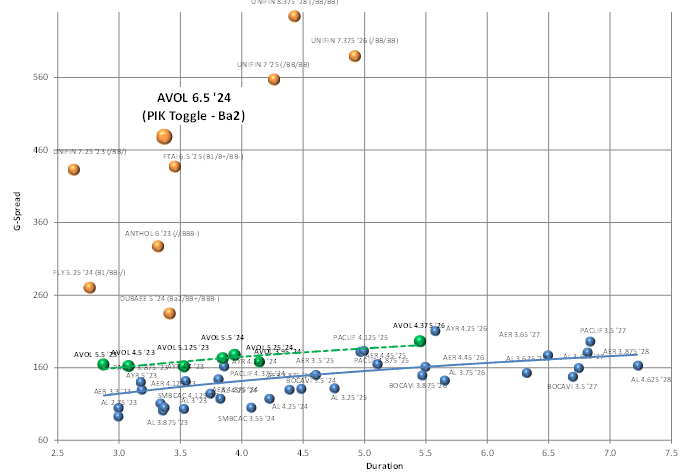

There is a unique opportunity in the market – a recent structured new issue from Avolon Holdings Ltd. that boasts IG credit with HY structure. The issuer is Global Air Lease Co. Ltd (GALC; new entity within Avolon Holdings Ltd), AVOL 6.50% 9/15/24 (5NC2, CUSIP: 37960JAA6) that has a senior AVOL rating of Baa3/BBB-/BBB- and a GLAC rating of Ba2/NR/NR. The 6.50% coupon has a PIK rate of 7.25%. AVOL 5NC2 PIK Toggle notes trade at roughly +450-500 bp to the curve, in-line with true HY issuers in the aircraft and commercial finance space (Exhibit 3).

Exhibit 3: IG and HY Aircraft Lessors / Commercial Finance

Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

Corporate structure

GALC is a newly formed entity that specifically holds Bohai Leasing’s 70% shareholder interest in the Company. Avolon was purchased by China-based Bohai Leasing Co Ltd in 2016 for $2.5 billion. Bohai is 51% majority-owned by Hong Kong-based and privately-held HNA Group. Late last year, Japanese commercial finance conglomerate ORIX Corp (ORIX: A3/A-/A-) bought a 30% equity stake with high voting rights in AVOL. The PIK Toggle notes are therefore considered structurally subordinated to the rest of the outstanding AVOL debt stack, due to the ownership relationship between Bohai versus the newer minority stake holder ORIX. The subordination, plus the PIK Toggle structure, account for the two-notch lower rating (Ba2) at Moody’s. The 5NC2 notes were issued in late July with the Paid-in-Kind Toggle feature, which enables the issuer to defer coupon payment until maturity at the higher “penalty” rate of 7.25%.

AVOL has one of the strongest aircraft portfolios in the industry, second only to AL. It is the second largest globally with 504 owned aircraft and 49 managed as of year-end. The company had commitments in place for 398 additional aircraft. AVOL boasts a very young fleet with an average age of 5.0 years – second only to AL among IG lessors. Remaining lease terms were 6.9 years on average as of 1Q19. The aircraft are 64% narrowbody and 36% widebody, with concentrations among popular models, such as the A320 CEO and NEO, the B737 NG and the A330. Exposure to the Boeing 737 MAX is currently only 6 aircraft, although it does account for 135 of the commitments. Their fleet is 58% Airbus and 37% Boeing. In the 1Q19, the company sold 20 of its aging aircraft (average age of 8 years).

No single airline accounts for over 5% of AVOL’s annual revenue, offering a diversified lessee base of 150 customers. Revenue is also diversified by geography with just over 50% from Asia Pacific, 26% in Europe/MENA and 22% in the Americas. To the extent there is residual/ongoing fallout from the Boeing 737 Max priced into the sector, that would present as an opportunity to add exposure; in short, there does not appear to be a high degree of risk from long-term cancellations in the program, and any near-term disruption will be offset by the potential leasing of alternative aircraft.

AVOL achieved investment grade ratings from all three rating agencies for the first time this year, when they issued the three-part $2.5 billion unsecured deal in April, using $1.2 billion of the proceeds to pay down secured debt and term out their debt profile. Unencumbered assets increased by $2.3 billion to $11 billion (of $27.5 billion total assets) as a result, offering a much more impressive base of assets that would be available to access for liquidity if necessary. Secured debt now makes up only 37% of total assets, which is a vast improvement to the liquidity profile, and instead has increased unsecured debt outstanding from $7.4 billion to over $12 billion including term loans. The company believes this leaves them with over $5 billion in available liquidity, including cash, restricted cash flows and undrawn secured debt. AVOL has negligible debt maturing prior to 2022, and a $2.5 billion revolver available until that year as well.

AVOL trades wide to the sector in part due to its foreign ownership, which means different reporting restrictions from other issuers in the segment. Avolon was purchased by China-based Bohai Leasing Co Ltd in 2016 for $2.5 billion. Bohai is 51% majority owned by Hong Kong-based and privately-held HNA Group. Given the current political unrest between the two regions, this creates a potential uncertainty with regard to AVOL; as well as the potentially opaque nature of the ultimate equity parent company, although HNA Group does report public financials. Late last year, Japanese commercial finance conglomerate ORIX Corp (ORIX: A3/A-/A-) bought a 30% equity stake with high voting rights in AVOL. The investment came with a shareholder agreement with Bohai that stipulates among other things that AVOL be managed as an investment grade company, and that dividends cannot exceed 50% of net income. This arrangement helps mitigates the risks of the Bohai/HNA ownership.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.