Uncategorized

A shift in liquidity rules could trim bank demand for Ginnies

admin | October 11, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

The Fed on October 10 eased liquidity and capital rules for a range of larger banks, opening the door to some significant portfolio rebalancing. Capital One, Charles Schwab, PNC Financial and US Bancorp seem most effected. Relaxed liquidity regulations coupled with Fed operations to push more excess reserves into the system may cause Ginnie Mae MBS spreads to widen and could ease some of the recent pressure on repo markets.

Changing the rules of engagement

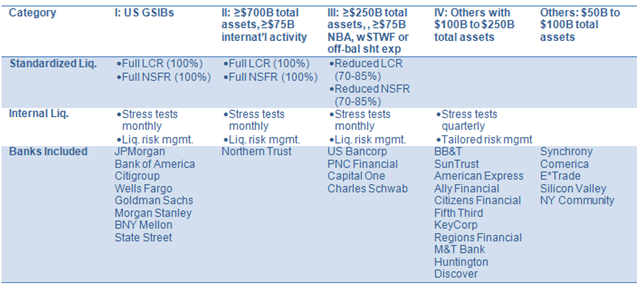

The Fed approval of rules proposed nearly a year ago will re-categorize banks from the current US Basel III designations of Global Systemically Important Banks (G-SIBs), advanced approach and modified approach banks into five categories. Among other things, the changes ease stress testing, liquidity and funding regulations for banks less than $700 billion in total assets in varying degrees. The most meaningful impact comes from relaxed liquidity rules for banks between $250 billion and $700 billion in total assets. These banks will see their required stores of liquidity reduced by anywhere from 15% to 30%, while banks between $50 and $250 billion will be exempt from both liquidity and funding requirements.

Basel III and specifically the Liquidity Coverage Ratio (LCR) has shaped bank demand since before the rule was proposed in the summer of 2013. The LCR rule was a game changer in terms of both the size and composition of bank portfolios as they put a premium on assets like Treasuries and Ginnie Mae MBS. These assets were relatively scarce across large bank portfolios prior to implementation but became integral after LCR prescribed that 60% of a banks’ total liquidity store come in the form of cash, excess reserves, Treasuries or Ginnie Mae MBS and CMOs.

The move will lighten the LCR burden for four institutions and remove it for an additional 16. Banks that are likely to get the largest amount of relief are institutions like US Bancorp, PNC, Capital One and Charles Schwab who collectively hold more than $350 billion in HQLA across cash, excess reserves and permissible securities as of last quarter. A 30% drawdown in their requirements would translate to more than a $100 billion decrease in demand. The combined BB&T and Suntrust entity would also receive a 15% to 30% decrease in their LCR needs but that is actually greater than the unmerged banks, which would have no LCR requirements given the fact that they are less than $250 billion in total assets apiece. (Exhibit 1)

Exhibit 1: The Fed’s proposed liquidity requirements reshuffles bank liquidity mandates

Note: NBA = nonbank assets, wSWTF = weighted short-term wholesale funding Source: Federal Reserve, Amherst Pierpont Securities

The move by the Fed will likely stymie future demand for Level I High Quality Liquid Assets (HQLA), particularly Treasuries and Ginnie Mae MBS and CMOs. Bank demand for Ginnie Mae multifamily securities like project loan CMOs may be less affected as banks will likely still use them to satisfy CRA requirements.

It is difficult to predict whether banks will actively sell HQLA after the changes to liquidity rules. Large stores of HQLA are locked up in held-to-maturity (HTM) portfolios. Breaking HTM to sell a portion of a bank’s HQLA stock would require the bank to mark all HTM assets to market – a huge deterrent to active sales. Additionally, while all classes of HQLA have to mark-to-market gains as of the end of last quarter, banks may be reluctant to sell in the face of deposit growth fueled by low interest rates. Furthermore, there are additional concerns other than LCR in terms of asset selection, moving out of HQLA into private label or ABS would likely have some implications for internal liquidity metrics and Fed stress testing.

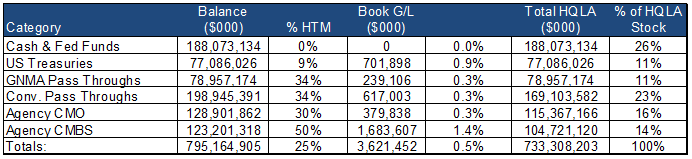

While passive deleveraging of HQLA through pay downs and reinvestment into higher yielding assets looks like the more probable scenario, banks may engage in some active selling. Ginnie Mae MBS and CMOs look particularly susceptible to potential sales for a couple of reasons. Two thirds of affected banks’ Ginnie Mae pass through holdings, totaling just over $50 billion, are in AFS portfolios and have an average gain of roughly one third of a point (Exhibit 2). Additionally, recent Fed operations to suppress volatility in the repo markets have injected billions of dollars of excess reserves into the system daily. These excess reserves count towards a bank’s stock of Level I HQLA and could suppress demand for Ginnie Mae MBS further as long as these operations remain in place.

Exhibit 2: Composition of affected banks stock of HQLA

Source: SNL Financial, Amherst Pierpont Securities

A shift in interest rate risk

Capital One, Charles Schwab, PNC Financial and US Bancorp along with some foreign banks operating in the US such as HSBC, TD Bank, RBC and others will also be able to take more interest rate risk in their available-for-sale portfolios without posing risk to regulatory capital. Under current rules for these banks, any mark-to-market gains or losses in AFS portfolios flow directly into regulatory capital. Under the newly approved rules, these banks can now elect to filter gains and losses out of regulatory capital. If these banks make this election, they will be able to add duration to their portfolios without risk of impairing capital as interest rates move around.

Ultimately we would expect any impact of the latest changes to be relatively modest and slow moving. The Fed proposed the October 10 rules roughly a year ago with limited opposition. The rules take effect 60 days after publication in the Federal Register. Given this, the move by the Fed may already be priced in as Ginnie/Fannie swaps were relatively unchanged after the announcement. Ultimately, this likely gives banks more latitude to draw down reserve balances at the Fed and have modestly more latitude with regards to their investment choices, likely favoring conventional over Ginne Mae MBS.