Uncategorized

Risks for legacy securitizations in the LIBOR transition

admin | September 27, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

The global effort to move away from LIBOR after 2021 has probably moved faster and further than many suspected when the UK’s Financial Conduct Authority first announced it. But the process may be saving the hardest part for last. The effort has largely focused so far on replacing LIBOR in new transactions, but no market arguably has a bigger challenge with existing transactions than securitization. A sizable share of LIBOR-indexed securitizations last beyond 2021, and the mechanisms for replacing the index are variable and rigid.

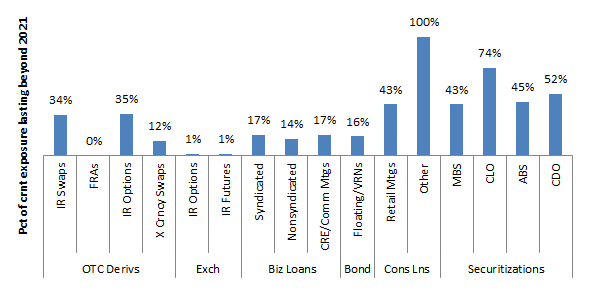

No market, beyond some categories of consumer loans, has a longer tail of LIBOR exposure beyond 2021 than securitization (Exhibit 1). MBS, ABS and CDOs each show 40% to 50% of recent exposures lasting beyond 2021, with CLOs showing nearly 75%. Other major markets have exposure of 35% or less.

Exhibit 1: Securitization has substantial exposure to LIBOR beyond 2021

Note: Data shows percent of gross notional exposures as of year-end 2016 that last beyond 2021. Based on The Alternative Reference Rates Committee, Second Report, March 2018, Table 1, available here.

Most securitizations never anticipated a permanent end to LIBOR. Although the language governing LIBOR settings varies across securitizations, may follow a common waterfall: set the index off of the British Bankers Association official LIBOR mark, set the index off readings from major UK or European banks, set the index off readings from New York banks and, if all else fails, revert to the last LIBOR setting. Reverting to the last LIBOR setting would obviously convert many securitizations from floating- to fixed-rate. The potential change in asset value and interest rate risk, and the potential for conflict of interest between different classes of a securitization, are clear. It would not be pretty.

The mechanisms in most securitizations for negotiating changes also vary across deals. For most MBS and ABS, any change that would affect deal cash flows must be approved by all investors. The rules across CLOs vary widely. An informal and unsystematic shows some CLO documents requiring unanimous consent from all investors, some a majority of interests in each deal class, some a majority of interests in a controlling class and some a majority of interests in the ‘AAA’ class.

Possibly more problematic than differences in the amendment process is the rigid process for communicating among interested investors. Most securitizations rely on DTCC for that, and only a deal trustee has authority to communicate to investors through DTCC. DTCC, in turn, sends communications to a range of securities custodians who then pass it on to investors. Assuming the communication reaches a decision maker, an investor that objects to a proposed change in the index has no way to communicate back through DTCC directly to other investors. The investor would have to contact the trustee and persuade the trustee to relay any objections or suggests. Negotiation becomes a process of iterating through DTCC, which could require a long timeline.

Investors in existing securitizations would have to negotiate a potentially wide range of details even if SOFR were the preferred LIBOR substitute. If no forward market existed after 2021 in term SOFR, investors may have to agree on a backward looking window. A backward window would involve decisions about opening and closing conventions for the window before resetting the coupon, handling the rate over weekends, using a simple average of SOFR in the window, a compound average or a median. If a forward market existed after 2021 in term SOFR, investors would still have to agree on the fair spread. Iterations on these details could be extensive.

Based on the number of speaker panels at the recent ABS East conference in Miami that directly or indirectly addressed the LIBOR transition and based on the conversations in the hallways, the securitization market is starting to recognize the complexity of the process. If there is an easy path, it is not clear.

At some point, investors in securitization will need to consider the risk in legacy LIBOR exposure. It is conceivable that other markets will move ahead. Derivatives counterparties often will negotiate the transition in the context of an ongoing trading relationship that could smooth the process. Borrowers and lenders in the loan market also will likely negotiate as part of a continuing relationship. Between different investors in a securitization, the relationship is largely transactional. Progress could be slow. Securitization could find itself approaching the end of 2021 without enough time to find a good solution.

* * *

The view in rates

The FOMC clearly believes another cut or two in fed funds should be enough to help growth and eventually tip inflation back towards its 2% target. The market still thinks the Fed eventually will go further. The rates of inflation and growth implied by 10-year notes and TIPS remain relatively low, and the curve remains relatively flat. Fundamentals suggest much better growth, and the Fed still has fed funds, forward guidance and QE left to fight low inflation. Trade has become the favored bogey for explaining the gap between Fed and markets, and trade is an influence difficult to predict. The best position: neutral on rates.

The view in spreads

The market has done a far better job of pricing a Fed inclined to create easy financial conditions, and most credit spreads have tightened. MBS has lagged credit. Financial conditions have eased since early August, according to most benchmarks, with lower rates and recent stock market gains contributing. The market sees another cut in fed funds by December. Low rates should help cash flows on corporate and consumer balance sheets.

The view in credit

The credit markets also have struggled to price risks to growth, but rather than price average growth the way rates markets might, credit has had to price for the tail event—recession. Recession seems unlikely in large part due to the readiness of the Fed, the ECB and other central banks to backstop growth. The Fed’s linking of policy to trade risk is among the more explicit examples. The drop in rates broadly and the likely continuing drop in short rates have helped. Fundamental corporate credit is soft with debt-to-EBITDA elevated and EBITDA-to-interest-expense below average. The weakest credits should feel a slowing economy, but without recession, the averages should remain good.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.