Uncategorized

Downside risk limited in Brighthouse 30-year paper

admin | September 27, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

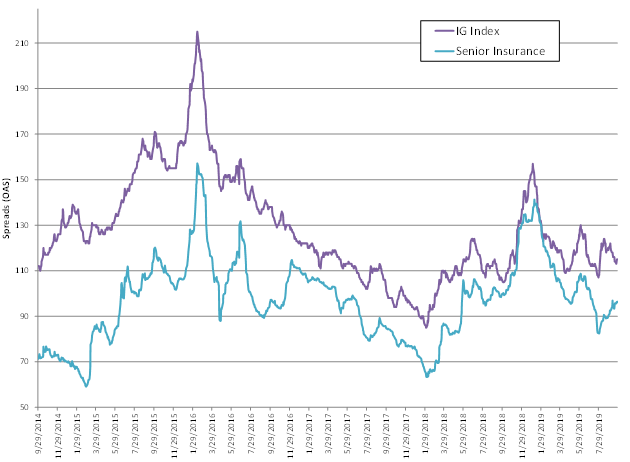

As investment grade spreads have moved tighter over the past several years, the gap between broad IG corporates and IG insurance has narrowed – indicating that investors can rotate more allocation into the sector at a lower give-up in spread than has traditionally been required.

Exhibit 1: IG index OAS vs IG insurance OAS – 5-year trend

Source: Bloomberg Barclays IG indices, Amherst Pierpont Securities

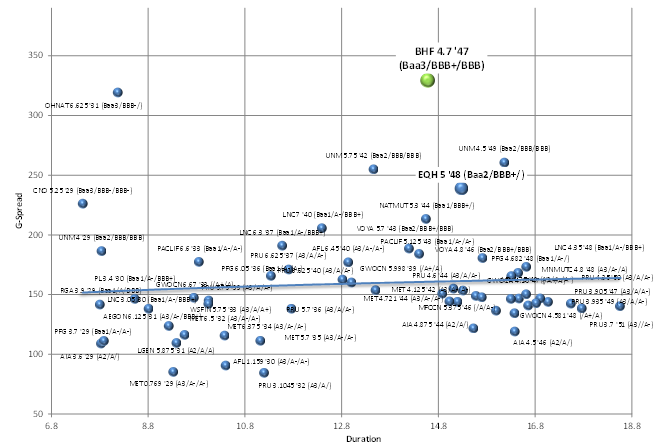

Even as overall corporate spreads have rallied year-to-date in higher beta issuers/sectors, Brighthouse Financial (BHF:Baa3/BBB+/BBB) continues to trade with the most spread in all of the IG life space – and arguably among the highest in broad financial senior paper. While some of the negative perceptions about the credit are warranted, the risk premium on the name sufficiently compensates investors for the reasonable downside in valuation. Bonds offer a roughly ~90 bp pick to closest peer EQH (Baa2/BBB+), which has a somewhat comparable risk profile.

Exhibit 2: IG life insurance 10- to 30-year paper, senior unsecured

Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

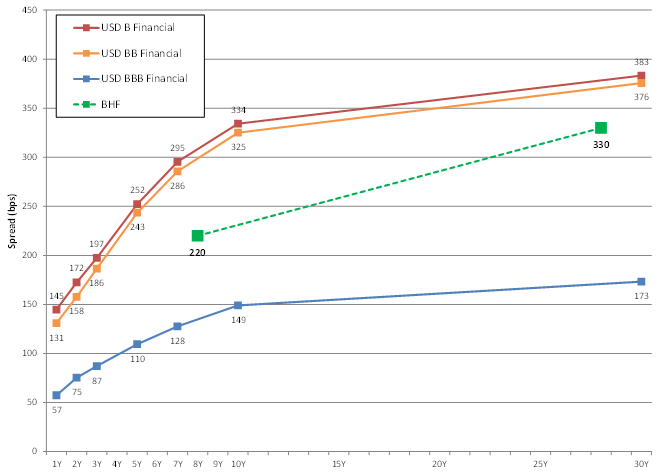

Although there are limited 30-year bonds outstanding to substantiate, Bloomberg fair value curves for high yield 30-year paper—whether single B or BB, industrial or financial—all indicate that BHF ‘47s are already trading very close to where the market would likely value a crossover or BB-rated issue with a comparable credit profile. While we do not expect BHF spreads to improve materially relative to the rest of the life insurance sector in the near-term, the downside trading risk appears limited, while the available yield for a BBB IG issuer (>5.3%) remains too compelling to ignore.

Exhibit 3: USD spread curves – BHF vs broad financials (B, BB, BBB)

Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

Risks associated with BHF credit have been well documented since it was first spun out of MetLife and issued debt for the first time in 2017. Perceptions are that the company is materially exposed to the double whammy of rate sensitivity and also being among the more sensitive credits within the IG life insurance segment to equity market volatility given BHF’s exposure to variable and fixed annuity product. An increasing percentage (the majority) of annuity sales are being generated through its newer flagship Shield suite of products, which a) are generating strong results among retail investors and b) have significantly less tail risk than some of the legacy products within the industry.

Other negative perceptions on BHF credit concern the valid disappointments of bondholders with management’s communication since its debut in the public debt markets. Specifically, the company saw capital levels weaken and overall credit quality deteriorate shortly after its initial offering. More recently, BHF management communicated a further slant to a more shareholder friendly posture – which they demonstrated through recent preferred and term loan issuance that helped fund their increased repurchase authority. On the positive side, this increase in leverage remained structurally subordinated to the long-term senior debt, but the negative reaction by bondholders is understandable. Nevertheless, even in a pessimistic scenario where cash flow deteriorates over the near-term—pushing leverage to non-IG levels—at current values investors’ downside is limited to the prospect of a downgrade to BB/crossover territory.

Exhibit 4: USD yield curves – BHF vs broad financials (B, BB, BBB)

Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

Although there has not been a very long track record to cite for standalone BHF since it debuted in 2017, the company’s cash flow generation has been far more consistent than investors give them credit. BHF generated roughly $3 billion in free cash flow in 2017, 2018 and over the last twelve months.

Front-end liquidity also appears very strong. BHF’s first real senior debt maturity is the BHF 2027s ($1.5 billion). In the interim they have only about $1.1 billion in smaller term loan maturities thru ’24, for which they have a $1 billion revolver available, in addition to just under $4 billion in cash.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.