Uncategorized

Argentina | Difficult economic transition

admin | September 27, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

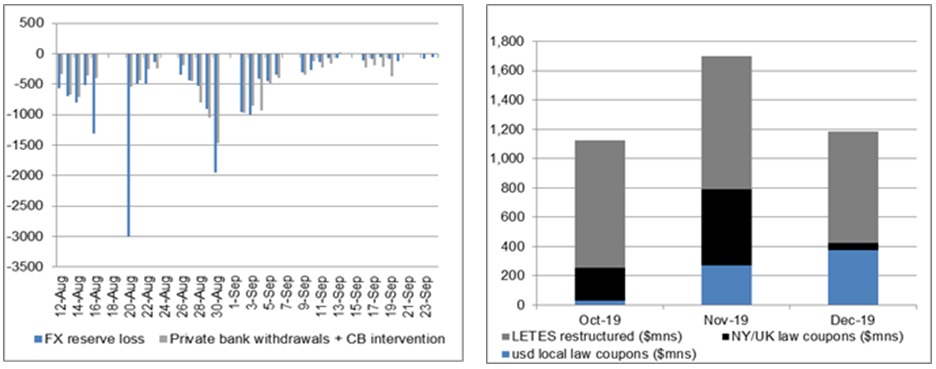

Argentina remains in limbo with cash flow stress under the Macri administration and only a slow economic transition with the Fernandez administration. The effectiveness of liquidity management will determine policy flexibility for the next administration. Capital controls have discouraged capital flight and encouraged exporter supply with foreign exchange reserve losses decelerating to around $100 million a day—despite persistent foreign exchange intervention and bank deposit withdrawals. But Argentina’s liquidity situation continues to worsen.

Argentina still needs liquidity to meet a consistent schedule of US dollar coupon and amortization payments. Export flow is insufficient to cover imports, tourism and debt service over the next few months, especially as declining foreign exchange reserves may re-accelerate US dollar demand. President Macri looks likely to remain current on domestic and external debt liabilities with the domestic debt restructuring legislation delayed until after the elections. The net foreign exchange reserves of $10.7 billion (9/15) would need to cover $2.6 billion in local law and NY law coupon payments and $2.5 billion of LETES from October to December 2019. This suggests manageable cash flow dynamics through year end even without the $6.3 billion of IMF disbursements.

Despite the recent high level meetings between the IMF and Argentina, IMF disbursements look unlikely until there is clarity on the economic program after the political transition. It will require highly efficient economic transition to negotiate with the IMF and bondholders to avoid an accidental default for the low $10.6 billion net reserves against high priority $7.2 billion in payments next year including $4 billion of NY/UK law coupons, $CHF400 million amortization, $2.3 billion provincial debt service and $500 million for YPF debt service. The domestic debt restructuring logically should be the first on the agenda soon after elections considering the $7.8 billion in US dollar equivalent coupons and $25 billion in US dollar equivalent amortizations in 2020. This explains the recent proposal sent to the legislature that sets the legal framework for a domestic debt restructuring via collective action clauses.

Exhibit 1: The pace of FX reserve loss slows Exhibit 2: USD claims on treasury payments

Source: Amherst Pierpont Securities

The initial reaction from the opposition suggests that the domestic debt restructuring will only occur after the elections. The Macri administration most likely focuses on liquidity and crisis management with all major initiatives including IMF and bondholder relations delayed until after the political transition. The logical sequencing of events should include a domestic debt restructuring and then negotiations with the IMF to develop a coherent economic plan as the basis of discussions of debt repayment capacity with external bondholders. How prepared is the Fernandez administration to quickly negotiate with the IMF and bondholders? This will define whether it’s an orderly or disorderly default next year. Is it possible to restructure debt prior to an IMF accord or fast track negotiations with the IMF or creditors?

The high level meetings between Argentina and the IMF arranged for more meetings on October 14; however acting MD David Lipton states that the situation is “extremely complex” and “the resumption of a financial relationship may have to wait awhile.” It would require a minimum of reworking the targets and DSA assumptions—not yet knowing the cash flow or solvency relief from creditors—for the SBA if not a complete conversion to an EFF to re-profile the heavy amortizations. The IMF relations cannot be avoided for the heavy net repayment schedule of $20 billion in 2022 and $22.6 billion in 2023. The active discussions may facilitate negotiations on the political transition; however it would be difficult for the IMF to resume the program without the full backing from the next administration. Perhaps the preliminary discussions could reduce the political costs; however it should still prove difficult to commit to a primary fiscal surplus that includes pension and labor reforms. The IMF relations are important for providing a credibility boost on economic policy management and access to credit (minimum of the $12.32 billion remaining of the current program) for a country that will struggle with large gross financing needs post restructuring.

Is it possible that negotiations with external bondholders commence prior to an IMF agreement? The recent headlines suggest that there have already been “friendly” bondholder proposals and informal discussions with the Fernandez team. The market cannot rule out preemptive debt restructuring that only focuses on liquidity relief; however it would require high exit yields on the still heavy debt burden and the uncertainty of medium term debt repayment capacity. This would still allow for potentially much higher recovery value compared to current prices–around 65 under assumption of coupon step up/accrual similar to the Discount bond, 15-year maturity extension, 5-year amortization structure with 14% exit yields. This would also imply more difficult IMF negotiations that emphasize more rigorous fiscal adjustment that reassures for medium term debt repayment capacity. There is a clear debate on whether it’s a liquidity crisis—politician’s narrow focus on near term problems—or a solvency crisis—a more realistic medium term assessment after pronounced foreign exchange weakness and downside risks to trend GDP growth. Meanwhile, bond prices remain in a consolidation range awaiting clarity from the Fernandez team post elections on how efficiently and effectively they can manage the economic transition and difficult internal negotiations with politicians as well as external negotiations with creditors.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.