By the Numbers

Financing options for transitional CRE loans

Mary Beth Fisher, PhD | September 9, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

Transitional loans occupy a specialized niche in commercial real estate finance, and the sources of funding for these loans continues to evolve. Although banks continue to do some lending in the sector, new regulations categorize transitional loans as high volatility commercial real estate (HVCRE) exposures, which results in significantly larger capital charges than those assessed against loans on stabilized properties. Beyond banks, sponsors and borrowers have several options for financing which range from relatively transparent to somewhat opaque:

- Lending via securitization – any type of transitional loan originated and underwritten by a REIT, commercial mortgage finance or private equity fund where financing is raised via securitization. A CRE CLO securitization channel is most frequently utilized for transitional loans, with the originator remaining the servicer on the loans and typically retaining the unrated and equity classes.

- Lending via agency securitization – multifamily transitional loans originated by a REIT, commercial mortgage finance company or bank, with underwriting done by Freddie Mac. Diversified pools of typically lite-transitional loans are securitized by Freddie Mac, with the class A securities guaranteed by the agency.

- Direct lending from portfolio investor – typically a REIT, insurance company, mutual fund or private debt investor with a specialized real estate lending group. The loans are not intended for securitization, but instead are retained in portfolio and serviced by the lender. Some banks provide term financing for pools of bridge loans similar to warehouse lines. This channel provides the greatest flexibility, and is frequently utilized by borrowers and investors to accommodate loans for larger, more complex transition plans.

This piece briefly reviews the factors that differentiate transitional lending from standard commercial real estate finance; provides an overview of the three financing channels; and includes a CRE CLO primer for investors in an appendix.

The transitional lending niche

Transitional lending is a catch-all term for a specialized type of financing sought to renovate, upgrade or reposition a commercial real estate property. These transitional or bridge loans are utilized as short-term financing to fund significant redevelopment or renovations for property that requires repairs and updates to attract new tenants, renew expiring leases, increase revenues, or repurpose space for a different use. Bridge loans are not considered permanent financing by lenders or by regulators. Borrowers repay the loans when renovation or leasing is complete and the stabilized property is either sold or the loan refinanced into a long-term loan with a traditional lender. By nature these are higher-risk, higher-interest rate loans that gravitate towards specialized lenders with sophisticated backgrounds in renovating commercial real estate.

Real estate developers that undertake building renovations and lenders who finance them both tend to have experienced, dedicated teams that manage transitional projects. Transitional real estate projects require developing two sets of financial statements – evaluating the building, its cash flows, market value and loan metrics “as is”; and projecting the cash flows, change in market value and new loan metrics “as stabilized” – that is, once the renovations have been completed and the occupancy and rent levels have presumably reached those of market peers.

Loans for transitional projects often require flexible terms, include provisions for future funding commitments, and provisions for maturity extension. The renovation projects themselves require careful monitoring for progress and conformance to business plans. Lenders often need the ability to work out issues with assets, adjust rates or make other modifications over the term of the loan.

Bridge loans are expensive for banks

Financing for commercial real estate comes from a variety of sources, but over 50% of it historically has come from US banks. New bank regulations recently implemented under Basel III categorize most transitional loans as High Volatility Commercial Real Estate (HVCRE). An HVCRE designation imposes a 150% risk weighting, compared to a 100% risk weighting for traditional commercial mortgage whole loans, and a 50% risk weighting for residential mortgage whole loans. Although banks may continue to be competitive in the bridge loan sector, it has become significantly more expensive from a capital perspective to originate the loans and hold them on the balance sheet.

Lending via securitization

The short-term nature, flexible financing requirements, and careful monitoring and servicing required of most bridge loans makes them unsuitable as collateral for standard CMBS securitization via a REMIC. A static pool of transitional loans can be financed via a CRE CLO vehicle using a REMIC, and Bancorp Bank does utilize them, but they are the exception to the rule. REMIC vehicles most commonly used in traditional CMBS securitizations impose significant restrictions on the composition of mortgage assets and the ability to replace assets after the closing date. REMIC status also prevents any material management of pool assets or modification of loans.

CRE CLOs

The need for a securitization structure that could accommodate the more flexible terms of bridge loans intersected with a desire for active management and ongoing reinvestment of transitional loan pools. These objectives were met by changing the tax structure of the underlying securitization vehicle.

Transitional loan securitization via CRE CLOs is usually done under the taxable mortgage pool (TMP) rules of the tax code, as opposed to the REMIC structure utilized both in conduit CMBS and Freddie Mac’s multifamily pass-through certificates. A detailed description of the differences in tax treatment is beyond the scope of this note, but an excerpt from a law article, The Taxation of CRE CLOs, provides a brief overview (the complete article can be found here):

In many ways, CRE-CLOs are a more flexible financing option than real estate mortgage investment conduits (REMICs), the traditional vehicles for commercial mortgage-backed securitizations. Unlike REMICs, CRE-CLOs may hold mezzanine loans, ‘‘delayed drawdown’’ loans, and ‘‘revolving’’ loans (and, in some cases, preferred equity), may borrow against a managed pool of assets, and may have more liberty to modify and foreclose on their assets.

CRE-CLOs are special purpose vehicles that issue notes primarily to institutional investors, invest the proceeds mainly in mortgage loans, and apply the interest and principal they receive on the mortgage loans to pay interest and principal on the notes that they issue. CRE-CLOs allow banks, real estate investment trusts (REITs), and other mortgage loan originators to sell their mortgage loan portfolios, freeing up capital that they can then use to make or acquire additional mortgage loans. By issuing multiple classes of notes with different seniorities and payment characteristics backed by a pool of mortgage loans, CRECLOs appeal to investors that may not be willing or able to invest directly in mortgage loans.

CRE CLO structures, rules, investment criteria, subordination levels and the like can vary significantly from deal to deal. This has minimal impact on borrowers but requires climbing a rather steep learning curve for investors.

For borrowers

Transitional lending via non-agency securitization is open for all CRE property types, and can encompass larger, more complex renovation projects on multifamily properties that fall outside of agency criteria. Both bank and nonbank lenders originate transitional loans, pool and finance them via securitization. The choice of securitization vehicle has little impact on borrowers. At this time the securitized transitional loan market is predominantly CRE CLOs as opposed to traditional CMBS.

Most CRE CLO deals have a single entity that underwrites all of the loans and a related entity that acts as deal manager.The originator typically retains servicing on the loan and works with the borrower monitoring progress and performing due diligence throughout the property rehabilitation. One wrinkle is that it’s not unusual for borrowers to seek loan modifications or refinance loans during the renovation period if interest rates fall, additional funds are required to address changing needs, or projects have transitioned into a stage of lower risk. Most CRE CLOs require servicer or special servicer approval for a performing loan to be modified and remain in the pool. Instead of modifications, issuers may refinance the loan under new terms and the deal manager can sometimes reacquire the loan during the reinvestment period as long as it meets eligibility criteria. To the extent that such a refinance introduces any additional paperwork or complexity for the borrower, it might result in a headache, but it’s probably somewhat less onerous than refinancing the loan with a new underwriter. Some recent CRE CLOs have sought more flexible deal terms that allow modifications of performing loans and refinances to occur and retain the loans in the pool.

For investors

CRE CLOs offer investors the opportunity to add exposure to transitional loans in commercial real estate. The deals tend to offer shorter-term, wider spread, floating rate securities, with greater subordination across the capital structure than those available in traditional CMBS. The diversification across property types available in CRE CLOs is also considered by some investors to be an important risk mitigant compared to the multifamily-only transitional loans in agency securitizations. For a complete discussion of the product, please see Appendix A: CRE CLO primer for investors.

Lending via agency securitization

Freddie Mac’s multifamily business purchases mortgages secured by apartment buildings with five or more units. The loans are sourced from a nationwide network of preapproved lenders who have substantial lending experience and established performance records. The agency uses a prior-approval underwriting process, then completes the underwriting and credit reviews of the mortgages using in-house staff. The total multifamily book of business was $313 billion as of 1Q 2019, with $13.4 billion of new business activity and $14 billion of multifamily loans securitized into K- and SB-deals in the quarter. Freddie Mac offers several specialized financing programs for multifamily transitional loans.

Value-add loan program

Freddie’s value-add loan program is for experienced developers/operators who are rehabilitating a multifamily property with upgrades in the range of $10,000 to $25,000 per unit. The targeted properties have no more than 500 total units, are in good locations, require modest repairs, and may benefit from new or improved management to bolster property performance. These lite-transitional loans are floating rate, interest only for three year terms, with the potential for one or two 12-month extensions. Loans are subject to a maximum loan to value (LTV) of 85%, and a minimum debt coverage ratio (DCR) of 1.10x – 1.15x, among other conditions. Appraisals include both as-is and as-stabilized values, and underwriting must support a 1.30x DCR and 75% LTV based on the as-stabilized value.

Freddie securitizes the value-add loans into their K-I deals. The agency guarantee applies to the class A securities only, as class B, C and X are not guaranteed by Freddie Mac. The floating rate coupon on the class A securities of a recent deal issued in August 2019, the FREMF KI04 A, was 1-month Libor + 36 bp.

Moderate rehab loan program

There is also a moderate rehab loan program for multifamily properties that require more significant rehabilitation. These loans are divided into an interim phase that lasts for 2-to-3 years while the renovations are ongoing, then transition into a permanent phase for 7 to 10 years. During the interim phase the loans are typically interest only, uncapped, then either transition fixed or require caps during the permanent phase. These loans are intended for multifamily properties that require $25,000 to $60,000 of renovations per unit, and are in strong rental markets. Conditions include up to 80% as-is LTV, a minimum 1.20x DCR based on as-is net operating income, among others.

Freddie finances the moderate rehab loans via the whole loan investment fund (WILF). Complete details comparing the value-add and moderate rehab loan programs can be found here on Freddie Mac’s website.

Q-series program

Freddie Mac also has used the Q-series program to securitize pools of transitional loans on multifamily properties that are originated and underwritten by a third party. These Q-series deals are similar to the K-I deals in that the guarantee applies to the class A securities only. These deals can allow for some additional flexibility in the underlying collateral. For example, lease-up loans are a type of transitional loan which are considered somewhat less risky as the renovations or construction project is already complete, and the building is in the process of attracting tenants or increasing occupancy. These bridge loans would not strictly conform to underwriting criteria for Freddie Mac’s value-add program but can be included under a third party securitization. An example of a recent issue is the FREMF 2019 KLU1, a $717 million sized deal of 16 loans.

For borrowers

Freddie Mac largely works through a pre-approved network of lenders for their multifamily programs, including those for transitional loans. The agency buys multifamily loans from lenders in their network and completes the underwriting and credit review process in house. In the value-add and moderate rehab programs, the underwriting process can be intense and getting final approval may take longer than going through a non-agency program or lender. The value-add program has no lock-out periods: the borrower may prepay the loan at any time, but must pay a 1% exit fee. The fee is waived if the borrower refinances with Freddie Mac.

Similarly to residential mortgages, agency-guaranteed transitional loans will typically offer the lowest cost of financing for borrowers who can meet their stringent criteria.

For investors

Agency CMBS investors generally benefit from regular issuance from the GSEs, a fairly liquid secondary market supported by a variety of broker-dealers, and some market transparency provided by aggregate summary statistics of price levels and volume in FINRA’s structured trading activity reports.

The class A securities have Freddie’s guarantee for timely payment of interest and ultimate payment of principal, and are often AAA-rated. Other investment grade classes will usually be rated by one or more credit rating agencies.

Lending from a portfolio investor

Comprehensive details of nonbank lending – size of the market, breakdown of asset types financed, loan terms and borrowers – are somewhat opaque, but it’s possible to construct a reasonable outline. Amherst Pierpont’s special report, Outside the bank’s front door: lending as a part of portfolio strategy, reviews the size and scope of the overall market, and discusses the investment case for lending by nonbank portfolios.

In the transitional lending space, many nonbank lenders – including insurance companies, private equity funds, hedge funds and REITs – engage in direct lending, in addition or as an alternative to financing originations via securitization. Reasons for doing so include higher yield, better portfolio diversification, more control over collateral, and the ability to scale up positions. Nonbank lenders often get help funding these originations via warehouse lines or a newly emerging bridge lending facility from commercial banks.

Warehouse lines

Traditional warehouse lines provide short-term financing for pools of collateral for terms up to 18 months. Bank regulators typically treat warehouse lines as revolving lines of credit, giving them a 100% risk-weighted classification, partly because the risk exposure for the line is much shorter than the term of the loan. Financing terms vary, but often lines of credit are subject to haircuts by the bank so the nonbank lender has to advance some of its own capital; the collateral can be marked to market which can cause the borrower to advance more cash; there are recourse terms to the borrower in the event a loan goes bad; and the warehouse provider can review loan documentation prior to advancing funds, and reject collateral or loan modifications to existing collateral.

Bridge lending facilities

A new type of bridge lending facility has emerged that is similar to a warehouse line, but also incorporates some of the advantages of financing via securitization. These new facilities have lending terms that are matched to those on the mortgage loans, the collateral is not required to be marked to market, and recourse terms are typically lower than those of warehouse lines.

An excellent article in the July 19, 2019 edition of Commercial Mortgage Alert (subscription required) provides an overview of these facilities, and discusses some of the counterparties (excerpt from page 1, continued on page 19):

In recent weeks, Morgan Stanley set up a $900 million facility backed by a pool of loans originated by KKR. It’s the second such arrangement for KKR, which previously closed on a $1 billion facility from an unidentified provider. Both are backed by fixed pools of bridge loans originated by KKR’s mortgage REIT. They don’t require revaluing collateral loans to reflect shifts in market values.

Invesco Real Estate obtained a similar, $400 million facility backed by a pool of bridge loans it originated, also from Morgan Stanley. The bank is currently seeking to syndicate a $300 million portion of that “note-on-note” facility.

Morgan Stanley also is expected to divide up the $900 million KKR facility. An unidentified group of insurance companies is taking down $400 million of that debt, and another $300 million is likely to be syndicated to other lenders. Potential participants are being told the pricing is around 175 bp over Libor.

These new facilities are currently being set up for large, well-established commercial real estate investors with deep experience in transitional lending; with additional participants entering via syndication. The bridge loan facilities and additional participations tend to match the terms of the underlying debt to the terms of the loans, avoiding the rollover risk of the traditional warehouse lines.

For borrowers

The choice of financing channel – securitization versus a traditional warehouse line versus a new bridge loan facility – has relatively minor impact on borrowers, but there are circumstances when it can become consequential. A borrower pursuing a modification whose loan has been securitized into a managed CRE CLO may find themselves jumping through additional hoops. New loans or modifications to existing loans are typically subject to eligibility criteria which requires a ruling by a ratings agency that it will not result in a downgrade. This is also a risk in a traditional warehouse line where the bank can review documents and has the authority to approve or reject the modification.

For investors

Portfolio lenders have the greatest amount of flexibility and control over the kinds of loans they make, the extent and complexity of the transition or rehabilitation to be undertaken for the property, the loan terms and advance rate. They also can finance their portfolio via private lines of credit, warehouse lines or bridge loan facilities, selling senior or pari-passu participations in their loans, or with corporate level debt or preferred equity. Additional debt may be permitted in the form of mezzanine financing.

The advantages for the lenders are that these facilities don’t bear the overhead costs of securitization, which include fees paid to ratings agencies and trustees; the facilities are typically lower recourse; it’s easier to modify loans and complete large, multi-faceted transition projects; and there is no need to build a diversified pool to satisfy ratings agency criteria.

Appendix A: CRE CLO primer for investors

Fixed income investors looking for exposure to commercial real estate have long invested in commercial mortgage-backed securities, or CMBS, but a new form of exposure has come into play in the last few years. Issuance of commercial real estate collateralized loan obligations, or CRE CLOs, reached $13.9 billion in 2018, up significantly from just a few years ago. CRE CLOs come with a different mix of loans, a different deal structure and generally wider spreads than CMBS, offering possible diversification or a better fit for some investment portfolios. In particular:

- The collateral is primarily comprised of 1- to 3-year, floating rate bridge loans on transitional assets. Many of the loans are extendible for up to two years and may include provisions for future funding commitments.

- Static and managed deals often include a ramp-up period of up to 6 months; managed deals include a reinvestment period typically from of 1- to 3-years, though some last for the life of the deal.

- Deal structures benefit from significantly more subordination at every rating level than is typical in conduit CMBS.

- Managers must satisfy extensive eligibility criteria when adding new assets to the pool.

Issuance and investors

CRE CLO issuance more than doubled from 2017 to 2018, from less than $7 billion in 2017 to nearly $14 billion in 2018. That increase was driven by several factors:

- Investor preference for short-duration floating rate notes during a time when the Fed was increasing interest rates, leading yields to rise and the yield curve to flatten.

- A hunt by investors for higher yields and an appetite for somewhat riskier collateral, when commercial real estate spreads in CMBS remained tight.

- REITs offering a competitive cost of financing compared to bank warehouse facilities or other traditional lenders.

Issuance in 2019 is projected to meet or surpass that from 2018. Average deal size is trending a bit higher at $680 million in 2019 versus $589 million in 2018 and $472 million in 2017, based on deals rated by Kroll Bond Rating Agency. Sponsors are showing a strong preference for managed as opposed to static deals. Since the latter half of 2018, more deals include ramp-up periods frequently up to 180 days, with a relatively larger percentages of collateral – in some cases 25 – 30% – to be added during the ramp.

CRE CLO purchases tend to span the spectrum, but are heavily weighted towards real money investors. Insurance companies, banks, and pension funds prefer the shorter duration, AAA-rated notes. Less credit restricted asset managers will often buy the lower AA and A rated pieces and hedge funds prefer the higher yielding BBB and below paper which can be attractively financed in the repo market.

The loans underlying CRE CLOs

CRE CLO vehicles are primarily collateralized by non-recourse, first lien, whole mortgage loans on transitional assets.

Transitional loans also usually come with future funding commitments. These commitments are contractual obligations of the original lender to provide the additional funds up to a specified amount, typically based on the successful completion of specific phases of the renovation, upon meeting various performance goals, or on a contingency basis to fund e.g. leasing costs. The future funding commitments are not obligations of the issuer and it is not required that future participations be added to the pool. However, the future funding commitments when made are pari passu participation interests in the mortgage loan. These future funding participations and funded companion participations are often added to the pool during the ramp-up or reinvestment period if there are sufficient funds available, the asset satisfies the eligibility criteria, the reinvestment criteria, and any other requirements as applicable regarding acquisition or disposition. The issuer is under no obligation to add these participations to the pool.

Prepayment protections can include lockout periods, yield maintenance, prepayment penalties and extension fees, and future financing commitments. According to Kroll Bond Rating Agency (KBRA) rated CRE CLO transactions, 40% of underlying CRE CLO loans paid off within 2 years and 89% of loans paid off in advance of their initial maturity, based on data since 2017.

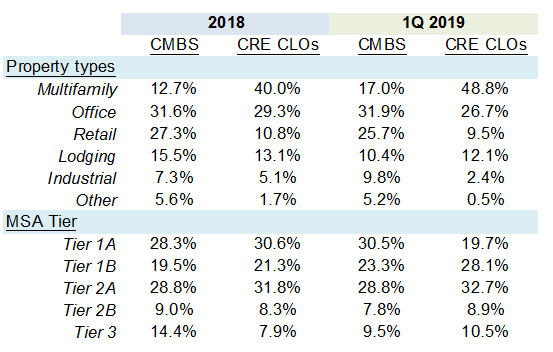

CRE CLO asset pools tend to be geographically diverse, similar to those in conduit CMBS, though multifamily properties comprise on average 40% of collateral in 2018 vintage deals compared to 13% of non-agency CMBS (Exhibit 1). Retail properties are also less frequent in CRE CLOs, making up on average only 10% of the collateral over the past five quarters compared to being 25% of that underlying CMBS.

Exhibit 1: Property type and geographical diversity of CRE CLOs vs CMBS

Source: All comparative data is for private label CMBS conduit and CRE CLOs rate by Kroll Bond Rating Agency (KBRA).

Differentiation between CRE CLOs and CMBS

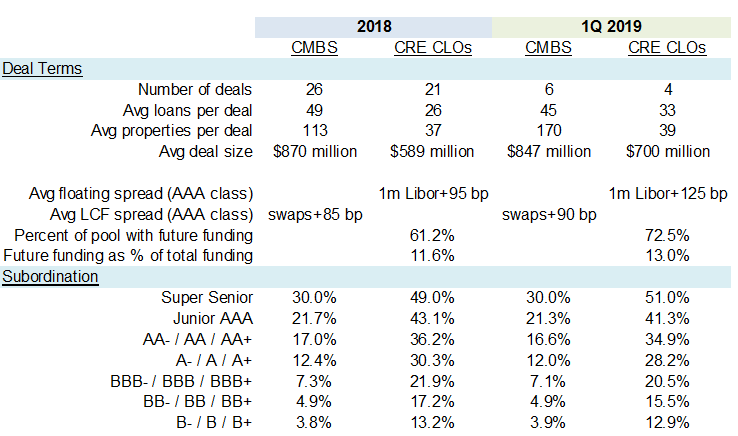

CRE CLOs tend to offer higher spreads, much shorter duration, and provide greater subordination across equivalently rated tranches compared to conduit CMBS (Exhibit 2). The increased risks inherent in the bridge loans comprising CRE CLO collateral are apparent in the higher LTVs at origination, lower debt service coverage ratios while the properties are in transition, and the presence of future funding commitments attached to a majority of the loans.

Exhibit 2: Deal terms and subordination in CRE CLOs vs CMBS

Source: All comparative data is only for private label CMBS conduits and CRE CLOs rated by KBRA.

CRE CLO structure overview

CRE CLO asset pools can be static or managed, though sponsors are trending towards more managed deals. Structural features often include ramp-up periods that vary from 90- to 180-days, and managed deals contain reinvestment periods that typically last from 24- to 36-months, where the manager can reinvest any principal proceeds in new mortgage assets provided the assets and the pool satisfy a variety of predefined criteria. Managed deals offer additional spread to investors to compensate for the potential uncertainty of negative credit drift during the reinvestment period. This risk is much lower than that of corporate CLOs as there are strict eligibility criteria for the new asset, diversity requirements that the pool must meet, and note protection tests that the pool must be able to pass when the new collateral is added.

Sponsors typically take a 15-25% first loss position in the pool by retaining the speculative grade notes and all of the preferred shares/equity. The top of the capital structure is rated by Moody’s, and all investment grade through high yield tranches are rated by Kroll. Weighted average life at origination across a typical deal will vary from 1.5 years for the Aaa tranche to 5 to 7 years for the B- tranche.

Ramp-up period

Ramp-up periods can be a feature of both static and managed deals. In recently issued deals ramp-up periods vary from 90- to 180-days. The assets acquired during the ramp-up period may or may not need to be pre-identified as of the closing date. The percentage of the principal balance of the pool that is to be added during the ramp-up period also varies widely by deal – with some deals that have ramp-up periods adding as little as 3% of total collateral, and others adding as much as 20% of total collateral during the ramp. Assets added during the ramp-up period have to satisfy the eligibility criteria outlined in the offering documents.

Reinvestment period

Managed deals include defined reinvestment periods, where proceeds from principal payments can be reinvested in new assets. The reinvestment periods range from 1- to 3-years, though some can last for the life of the deal.

There is a substantial amount of variability across deals as to what assets can be added during the reinvestment period. Similar to the restrictions during the ramp-up period, some deals only allow pre-identified assets to be added during reinvestment. These will frequently consist of future funding participations and companion participations of loans already in the pool. It has become more common in recent deals for managers to have the flexibility to add assets that have not been identified by the closing date. The assets added during the reinvestment period are still required to satisfy the eligibility criteria.

Eligibility criteria

Eligibility criteria for adding assets to CRE CLO tends to be detailed, extensive and deal specific. Broadly speaking, the eligibility criteria for adding new assets during ramp-up or reinvestment can include, but are not limited to:

- Limits on the amount of each property type that is allowed to be in the pool.

- Geographic concentration limits by state.

- Loan size limits and dispersion index minimums.

- LTV maximums and DSC ratio minimums.

- Maintaining a minimum weighted average spread to 1-month Libor, a maximum weighted average life of all loans, and limiting the maximum term of a loan extension.

- Confirmation from KBRA that the addition of the loan will not cause a downgrade of any of the notes.

There is also an entire suite of legal and definitional criteria that the loan must meet to be eligible for inclusion. For an exhaustive list please consult KBRA and the offering documents for each deal.

Note protection tests and mandatory redemptions

There are various circumstances under which the CRE CLO notes can typically be redeemed or called. Although these may vary somewhat in their particulars, deals commonly include both a mandatory redemption trigger and a clean-up call.

A mandatory redemption will occur when any note protection test(s) as outlined in the offering documents is(are) not satisfied. The note protection tests are evaluated on all measurement dates. Measurement dates include the closing date, on the date of acquisition or disposition of any mortgage asset, prior to each payment date, on any date when a mortgage asset goes into default, and on any date at the request of the rating agencies or two-thirds of the holders of any class of notes.

The note protection test(s) include a test for overcollateralization of the offered notes in the form of a minimum par value ratio. The par value ratio is generally calculated as the net outstanding portfolio balance divided by the sum of the aggregate outstanding amount of the offered notes. Minimum par value ratios vary considerably across deals, but fall roughly in the range of 115% – 135%.

Additional note protection tests can include a minimum interest coverage ratio. A little more than half of currently outstanding CRE CLOs include a minimum interest coverage ratio as a note protection test. The interest coverage ratio is roughly defined as the expected scheduled interest income of the mortgage assets and eligible investments, divided by the expected interest payable on the offered notes. Like the par value ratio, the interest coverage ratio is evaluated on all measurement dates. The minimum interest coverage ratio in deals where one is defined is usually 120% or 1.20x.

If either the calculated par value or interest coverage ratio falls below the minimum on any measurement date, on the following payment date interest proceeds are used – in accordance with the priority of payments – to pay down or redeem the principal on the offered notes until the relevant note protection test can be passed.

Callability

The deals are typically subject to clean-up calls, where the entire deal can be called when e.g. the outstanding principal balance is 10% or less of the original aggregate outstanding amount. Given the extensive level of subordination in CRE CLOs, by the time a clean-up call is executed all of the investment grade notes or offered notes will likely no longer be outstanding.

A note on ratings

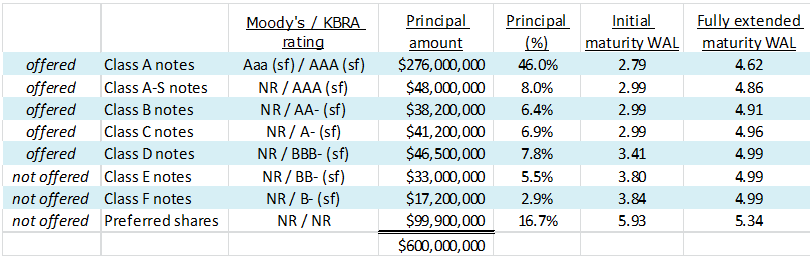

Virtually all CRE CLOs have the Class A notes rated by Moody’s, and most have the Class A through Class F notes rated by Kroll Bond Rating Agency (KBRA). The notes rated investment grade are the notes offered for sale, those rated below investment grade and the preferred shares (which are not rated) are not offered. An example of a typical CRE CLO deal structure is shown in Exhibit 3.

Exhibit 3: Deal structure of BDS 2018-FL3

Source: Preliminary offering memorandum, dated 12/3/2018.

The following language regarding the methodology used by Moody’s and KBRA to assign ratings appears in the offering memorandum (excerpted from page 153 as numbered):

The ratings assigned to the Notes by Moody’s and KBRA are based upon its assessment of the probability that the Mortgage Assets will provide sufficient funds to pay such Notes, based largely upon the Rating Agency’s statistical analysis of historical default rates on debt obligations with various ratings, expected recovery rates on the Mortgage Assets, and the asset and interest coverage required for such Notes (which is achieved through the subordination of more junior Notes).

The ratings of the Notes take into consideration the characteristics and credit quality of the Mortgage Assets and the structural and legal aspects associated with the Notes and the extent to which the payment stream from the Mortgage Assets is adequate to make payments required under the Notes. The ratings on the Notes do not, however, constitute statements regarding the likelihood or frequency of prepayments, both voluntary and involuntary, on the Mortgage Assets, the degree to which the payments might differ from those originally contemplated, the tax attributes of the Notes or the possibility that Noteholders might realize a lower than anticipated yield. The rating applicable for each Class does not address the likelihood of receipt of any Defaulted Interest Amount. In addition, a rating does not address the likelihood or frequency of the receipt of prepayment premiums, spread maintenance, yield maintenance charges or net default interest. A securities rating does not assess the yield to maturity that investors may experience and, in general, the ratings address credit risk and not prepayment risk.

Conclusion

CRE CLOs provide investors commercial real estate exposure to transitional assets. Lending on properties undergoing significant renovation is migrating away from banks due to the increased capital charge associated with these so-designated high volatility commercial real estate loans. Bridge loan collateral is generally ill-suited for conduit CMBS securitization due to the strict constraints on modifications or replacement of mortgage assets in REMIC vehicles. The closest competitor is Freddie Mac has a securitization channel for value-add loans on multifamily properties. By comparison CRE CLOs provide steadier issuance across a larger number of deals, greater diversity of property types, increased spread, and the ability to invest across the investment grade ratings stack. Commercial real estate investors can diversify portfolios by including CRE CLO exposures that are shorter-duration, floating-rate notes, offering wider spreads and higher levels of subordination than typical CMBS.