Uncategorized

Weighing the impact of politics

admin | September 6, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

Politics has always shaped US markets, but usually through policies that affect the economy. These days, the delivery is often more direct. Most recently, new administration proposals to reform mortgage finance could directly affect markets for MBS and CMBS, among others. There’s only one way to invest in markets buffeted directly by politics: get inside the beltway.

The US mortgage market has arguably been the most politicized market in US finance for decades. Since the 1930s, housing crises driven by either credit or interest rates have steady increased government involvement. Out of the Great Depression came the Federal Home Loan Bank System, the Federal Housing Administration, the original incarnation of Fannie Mae and, after World War II, mortgages guaranteed by the Veterans Administration. Problems funding mortgage loans in the 1960s brought an updated version of Fannie Mae along with newly created Ginnie Mae and Freddie Mac. The interest rate volatility of the 1980s drove mortgage financing out of banks and into the capital markets. And the 2008 financial crisis has pushed nominal control of mortgage finance largely into the hands of regulators including the Federal Housing Finance Agency, the Consumer Financial Protection Bureau and the US Treasury.

The entanglement of government with mortgage finance in the US makes handicapping real policy change an insider’s game. US housing, like housing in many countries, is a product partially subsidized by the government. And every member of Congress has a healthy share of constituents that get tangible benefits from this. Beyond voters, entire parts of the economy run under the assumption that mortgage finance policy continues. Those parts are represented by the Mortgage Bankers Association, the American Bankers Association, the National Association of Realtors, the National Association of Home Builders and a host of organizations lobbying for affordable housing, just to name a few. These organizations represent businesses in almost every congressional district. Those businesses have money. And they have lobbyists.

So, here’s the calculus: if a policy proposal creates any winners or losers, who lines up on either side, how much political currency can they and their allies bring to the fight and will that be enough to influence the process. All of these are answerable questions, but not by most investors just reading the newspapers. The people and organizations involved in the fight will have a sense of where the chips may fall.

The most investable parts of the new mortgage finance reform proposal all revolve around decisions that the Federal Housing Finance Agency, the Consumer Financial Protection Bureau and the US Treasury could make alone or in concert. The FHFA and the CFPB are both insulated from political pressure. The FHFA, for example, gets annual funding not from Congress but from assessments on Fannie Mae, Freddie Mac and the FHLBanks.. And the agency director can only be fired by a sitting president for cause. The CFPB gets funding from Federal Reserve banks, and its director, too, can only be fired for cause. That insulates but does not eliminate political pressure. Both organizations rely in some part on other parts of government to get things done.

The FHFA could unilaterally decide to reign in Fannie Mae and Freddie Mac guarantees on loans with high debt-to-income ratios, or tighten the underwriting of cash-out refinancing. It could try to cap the enterprises’ share of the multi-family housing market. It could allow REITs to come into the FHLBank system through captive insurers. These decisions would affect the supply and pricing of agency and private MBS and CMBS, and the size and profitability of US REITs. The potential market impacts are clear.

There’s the impact, and then there’s the probability of the event. Sketching the impact is easy. Figuring out the probability is hard. That’s where getting inside the beltway and seeing the constituencies involved makes the difference. For investors thinking about positioning against the latest proposals for mortgage finance reform, the hard part starts now.

* * *

The view in rates

The value of convexity for the rest of 2019 has not diminished. Implied US rate volatility came off as expected after Jackson Hole but still stands near the highest levels since early 2016. Trade tensions give volatility plenty of room to run. It is hard to predict the next twist in trade and, consequently, shifts in potential Fed policy and rates. Good investors should only take risks they can understand and manage, and prudence argues for being neutral on rates. Convexity should continue to perform well. Long positions in volatility should pay.

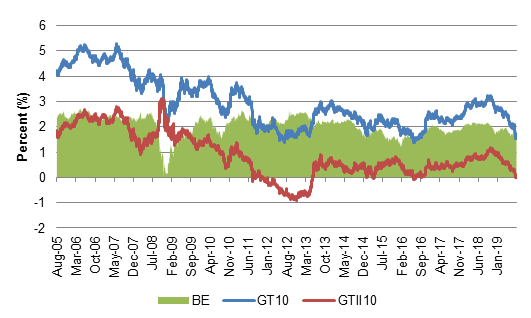

It is intriguing to think that the bullish flattening and inversion that has been in motion since January could continue. Longer US rates are moving far faster than the Fed. The Fed is focused on the US economy, the long end may be more focused on the global economy. QE and foreign flows into US debt have also distorted the curve and could continue distorting it. The 10-year point on the curve is currently priced for nearly 0% real rates and 156 bp of inflation. Real rates are poised to go negative on rising trade tensions, and nominal rates would likely track lower, too.

Exhibit 1: The market is pricing for 0% 10-year real rates and 156 bp of inflation

Source: Bloomberg as of 8/20/19, Amherst Pierpont Securities

The view in spreads

All spread products show sensitivity to market volatility, making directional calls on spreads more difficult than usual. Corporate spreads look the most vulnerable, consumer ABS and private MBS the next in line and agency MBS the least vulnerable. Agency MBS is likely to see a wave of prepayments, putting supply pressure on TBA benchmarks. Investors in spread products have to be able to ride out the likely higher spread volatility ahead for the balance of the year.

The view in credit

Fundamental credit could be vulnerable in parts of the corporate market sensitive to trade such as technology and communication, energy and commodities. Industries with a domestic US focus look better. Households look even better. Low interest rates have spurred mortgage refinancing, which should further reduce household debt burden. Low rates should also give some support to home prices, which should help homeowners continue to build equity.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.