Uncategorized

Argentina | Cash flow watch

admin | August 23, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

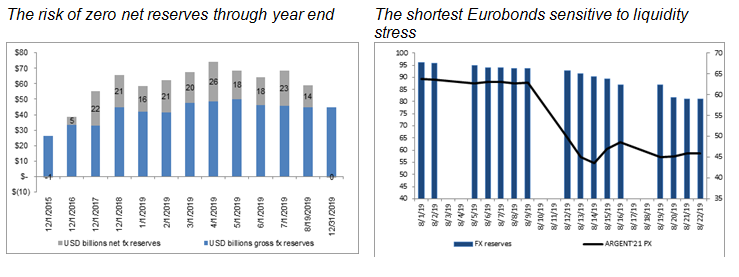

Foreign exchange reserve depletion continues in Argentina with net reserves now at $13.4 billion and ongoing uncertainty around central bank intervention and access to voluntary capital markets. The current pace of reserve loss suggests a return to the balance of payments stress of 2015 when net reserves went negative. There is not much the Macri administration can do other than damage control during the uncertainty of the election cycle. It’s a balancing act between preventing excessive foreign exchange weakness or reserve loss, for deterring and funding USD demand, and avoiding the worst case scenario of retail dollarization.

This is the constraint of a dual currency system and repetitive economic crises that reinforces USD demand. The press conferences from the economic team attempt to reassure on foreign exchange competitiveness; however, it remains cash flow watch on monitoring the daily decline in foreign exchange reserves. It’s encouraging that the foreign exchange rate has remained with a range of 55-60, but this has been at the expense of an unsustainable pace of $878-million-a-day (8/12-8/22) reserve loss.

Source: http://www.argentina.gob.ar/hacienda

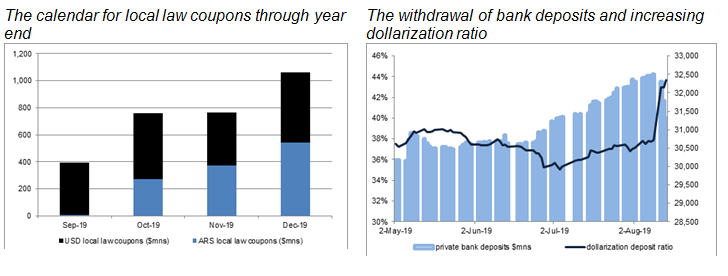

The negative shock post PASO continues with foreign exchange reserve loss of $7.9 billion through the past two weeks. This pace is clearly unsustainable against our current calculation of $13.4 billion in net foreign exchange reserves. What are the future claims against foreign exchange reserves and what are the options for the Macri administration? The market cannot rule out a potential positive shock from the Fernandez team under acute cash flow stress; however, the burden near term remains on the Macri administration to fund the outflows ahead of a worst case scenario of administrative and regulatory restrictions. The potential claims against foreign exchange reserves through 4Q19 are the USD demand on non-rollover of the private sector in treasury auctions, the local law coupon payments and further dollarization of USD bank deposits.

Source: http://www.argentina.gob.ar/hacienda

The high frequency treasury auctions are the primary concern, especially for risk of repatriation of foreign holdings in LECAP bills. The IMF (table 8 in fourth review) shows the expectations for gross financing needs for 2019 including private sector issuances of $11.3 billion from September through December. The breakdown assumes $5.6 billion for LETES and $4.8 billion for LECAP and other short term bills on a 75% rollover rate.

It’s difficult to reconcile the private sector holdings via specific maturities for the latest investor presentation (7/17/2019), though it looks like a high percentage of private sector participation between 50%-80%. On referencing the last LETES auction 8/13, the low rollover rate of 43% suggests only public sector support. The next test will be August 27 and August 30 with $2.5 billion of maturing LETES and LECAP and potential $1.6 billion claim against foreign exchange reserves assuming zero private sector rollover and USD conversion from local and foreign investors.

If this trend continues, then this could represent a potential claim of $11.3 billion through year-end against foreign exchange reserves. It seems fair to assume a similar shift from maturing ARS/USD local law coupons into cash holdings with $3 billion scheduled for payment through year end. The culmination of maturing treasury bills and local law coupon payments could push net foreign exchange reserves through zero by year end and potentially sooner if reserve loss motivates further dollarization within the banking system. The market should closely monitor deposit flight at a mature phase of dollarization at 43% (against 10% Kirchner era average). The $1.5 billion withdrawals of USD private sector bank deposits 8/12-8/15 reduces gross but not net foreign exchange reserves and hence it is more important to monitor the dollarization ratio. The eroding margin of flexibility would require either conversion of swap lines (gross foreign exchange reserves cannot decline below the $14.5 billion of private sector bank deposits) or administrative controls similar to 2015.

Source: BCRA, Bloomberg

It looks increasingly complicated for cash flow management with liquidity stress potentially triggering a cycle of USD demand. The complacency of the recent run-up on Eurobond prices over the past few days seems to ignore the latest cash flow stress. The liquidity stress could start to contaminate Eurobond performance on a higher sensitivity/correlation on foreign exchange reserve depletion that suggests a test for new lows closer to 40 historic sovereign recovery value. The shortest maturity bonds like the ARGENT’21 should have the highest sensitivity to cash flow stress as the leading indicator for when liquidity risks converge into solvency risks. Further price compression across the Eurobond curve should come if cash flow stress intensifies. The only effective solution to counter negative investor sentiment is the confirmation of an economic plan based on a fiscal anchor from the Fernandez team. It’s not sufficient to reject capital controls and debt default without first committing to the conditions necessary to avoid a broader economic crisis.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.