Uncategorized

High coupon tender candidates for total return investors

admin | August 16, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

Of the 56 investment grade issuers that brought new USD corporate deals this month since the 10-year US Treasury rate dropped below 2.00%, eight were done in conjunction with a tender offer to redeem existing debt. Those issuers included: CVS, HIG, EPR, LNC, SHW, VITR, GLCP and AIZ. This type of activity is expected to pick as long-end rates remain under pressure and appetite for yield continues to provide corporate management teams with new opportunity to manage down their liabilities and improve efficiency within the capital structure. Issuers tend to pay generous premiums on the solicitations for these less liquid tranches to get permission for early redemption.

This is by no means a new phenomenon – and quite arguably the lowest hanging fruit has previously been addressed over the course of the past several years, as issuers have had historic opportunity to access public markets and take out higher cost debt. Nevertheless, the new rate paradigm opens the door for a fresh round of tender/issue activity among both investment grade and high yield issuers. Active investors should reassess these opportunities, and seek out high probability candidates for total return opportunities – even among issues that have already had one or several tender offers executed on them.

As of Thursday’s close, aggregate yields for 30-year debt in IG credit were roughly 3.4%, and 2.8% for 10-year credit, with spreads of +130 and +143, respectively. The Corporate Aggregate IG Index yield stood at 2.92%, the lowest level since the second half of 2016. Index spread (OAS) was at +123, meaning that spread for IG corporates now makes up approximately 42% of total yield, nearly a full standard deviation above the 20-year average for the IG Index – a factor that will likely keep investors engaged even if heightened capital markets volatility persists.

Refinancing candidates in consumer/TMT

The Treasury curve continues ratcheting tighter and the 10-year Treasury hit levels not seen in over 3 years, while the 30-year yield reached a record low. In this environment corporate credit should remain active with respect to refinancing. The move in rates prompted multiple issuers to tap the market in conjunction with a tender offer. The inverted curve provides a great opportunity to extend maturities while reducing interest costs. Below are few names within the consumer, technology and media sectors that are good refinancing candidates.

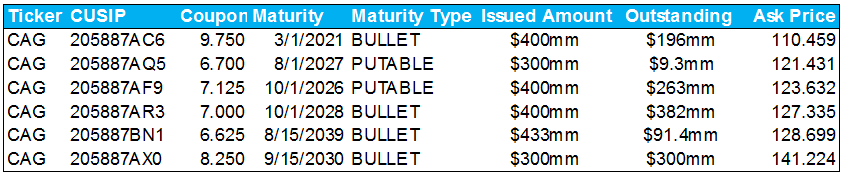

Conagra Brands Inc. (CAG: Baa3/BBB-/BBB-)

While CAG remains in debt reduction mode as it looks to reduce leverage stemming from its acquisition of Pinnacle, it makes a good refinancing candidate as the company’s weighted average coupon rate of 4.93% remains the highest among its packaged food and beverage peers. Similarly rated KHC’s weighted average coupon rate currently stands at 4.3% while its weighted average maturity of 11.25 years is nearly 2 years longer than CAG’s 9 years. Peer TAP’s weighted average coupon stands at 3.2% with an average maturity of 11.18 years. CAG’s last tender offer occurred in early 2016, in conjunction with the sale of the private label business. Subsequent to the tender offer management has utilized open market purchases to further reduce debt. However, CAG’s capital structure remains dotted with a few high coupon bonds that could be potential refinancing candidates.

Exhibit 1: CAG high coupon bonds

Source: Bloomberg, Amherst Pierpont Securities

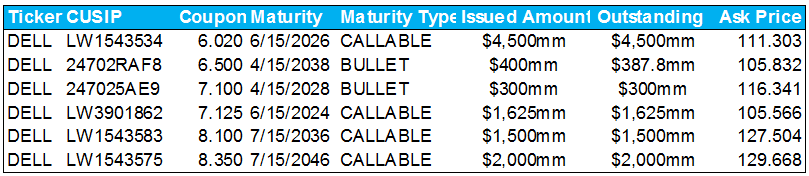

Dell Technologies Inc. (DELL: Baa3/BBB-/BBB) first lien

While the company already took the opportunity in March of this year to tap the market for $4.5 billion to fund the refinancing of some of its term loan debt, DELL still makes a good refinancing candidate. DELL has been making good on its debt reduction commitment and has repaid $15 billion of gross debt since the close of the EMC acquisition. Management noted on its most recent earnings call that it remains on track to repay $4.8 billion of debt this fiscal year after repaying $400 million in fiscal 1Q20. Management is likely to continue to target the term loans for debt reduction purposes as $10.9 billion remained outstanding as of 5/3/19. The company could look to tap the market to fully retire the term loans, target some debt that was issued at the close of the EMC transaction or even look to take out some unsecured paper. Despite the majority of the debt in its capital structure being secured (59%) and having low BBB ratings, DELL’s weighted average coupon remains at 5.19% on a weighted average maturity of 6.05 years. This compares to 4.81% and 5.95 years at Seagate (STX – Baa3/BB+/BBB-).

Exhibit 2: DELL high coupon bonds

Source: Bloomberg, Amherst Pierpont Securities

The Walt Disney Co. (DIS: A2/A/A)

After completing the Twenty-First Century Fox (21CF) acquisition earlier this year and subsequently exchanging the 21CF bonds into New Disney notes, the issuing entity going forward, DIS’ capital structure remains littered with high coupon bonds as the 21CF bonds were exchanged into New Disney bonds with the same coupon and tenors. Participation in the exchange was high at 95% or higher for each series of notes, leaving over $18 billion of debt from over 30 issues with coupons that are very high for the company’s mid-single A ratings. DIS’ weighted average coupon remains high at 4.61% on a weighted average maturity of 8.27 years. This compares with a 4.18% coupon/12.38 years at Comcast (CMCSA- A3/A-/A-) and 4.32% coupon/12.91 years at AT&T (T – Baa2/BBB/A-).

Seeking opportunities in insurance

One area of the market that has been particularly active—and could see an additional ramp up in activity—is among insurance companies, particularly for BBB issuers that are now able to bring 10 and 30-year paper at yields that have been unavailable for some time. There have been three prime examples of this activity over the past week. Hartford Financial (HIG: Baa1/BBB+) brought $1.4 billion of 10- and 30-year fixed senior debt, at launch yields of 2.80% and 4.9%, respectively. A portion of the proceeds was utilized to pay down the $694 million of 2022 and 2023 notes that had been recently tendered.

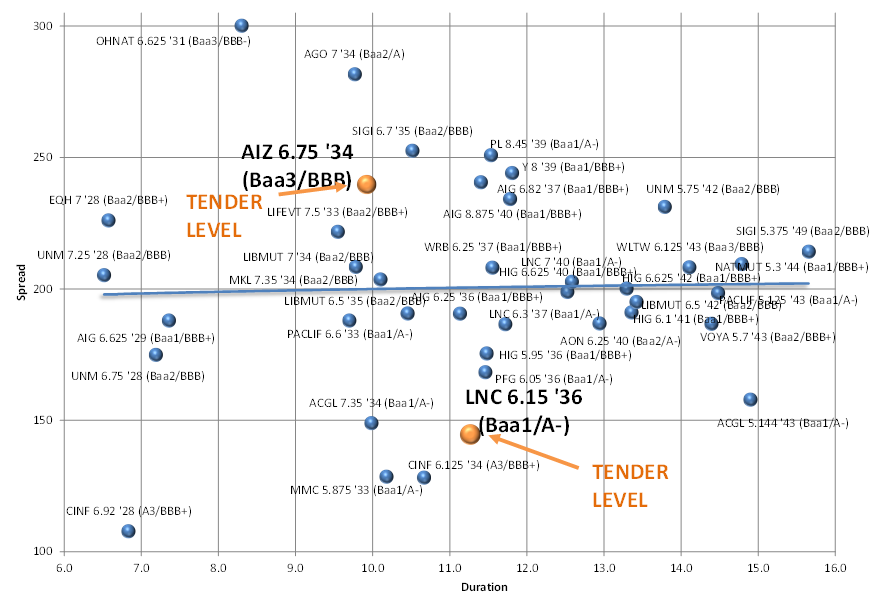

Exhibit 3: High coupon tender candidates – BBB insurance

Note: Active tender situations shown at tender level. Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

Lincoln National (LNC: Baa1/A-/A-) priced a $500 million long 10-year note at a launch yield of just 3.05%, which will be utilized to retire upwards of $50 million in front-end notes (2021), as well as up to $150 million of the $348 million remaining in the LNC 6.15% notes due 2036. LNC had previously taken out $150 million of the notes back in 2016. Worth mentioning is that only $160 million worth of notes had been tendered – meaning those that those who participated had a very high rate of acceptance and got to make the most of the premium. Longer-dated insurance paper is frequently held by insurance investors, who are less likely to participate due to both book yield and liability matching constraints, even if there is a new true 30- or 10-year deal available for purchase.

Lastly, Assurant (AIZ: Baa3/BBB) launched a $350 million long 10-year at a total yield of just 3.7%, a portion of which will go to tender for the higher coupon AIZ 6.75% of ’34, as well as redeem their callable 2021 floaters. AIZ will repurchase up to $100 million of the remaining $375 million of the AIZ ’34 bonds outstanding, meaning those left behind are likely to lose index eligibility. Bonds are being taken out at +205/30-year, which represents a premium of more than 10 points above where bonds were pricing just three months ago. Two months earlier it was highlighted here that AIZ might take out some of this specific issue, as management sought to reduce interest expenses following recent acquisition activity. The company had taken out $100 million of this issue back in late 2016, and like LNC, only $160 million were tendered, meaning those who participated got paid out on over 60% of the bonds requested.

Below is a list of more likely tender candidates within the industry. Issuers are likely to take out a mix of front-end and longer maturities, as was the case with both LNC and AIZ, but the list focuses on the long-end of the curve, as those issues present the better opportunities for total return investors. The highlighted issues have been previously addressed by corporate management teams, which could easily see a second or even third round of redemptions.

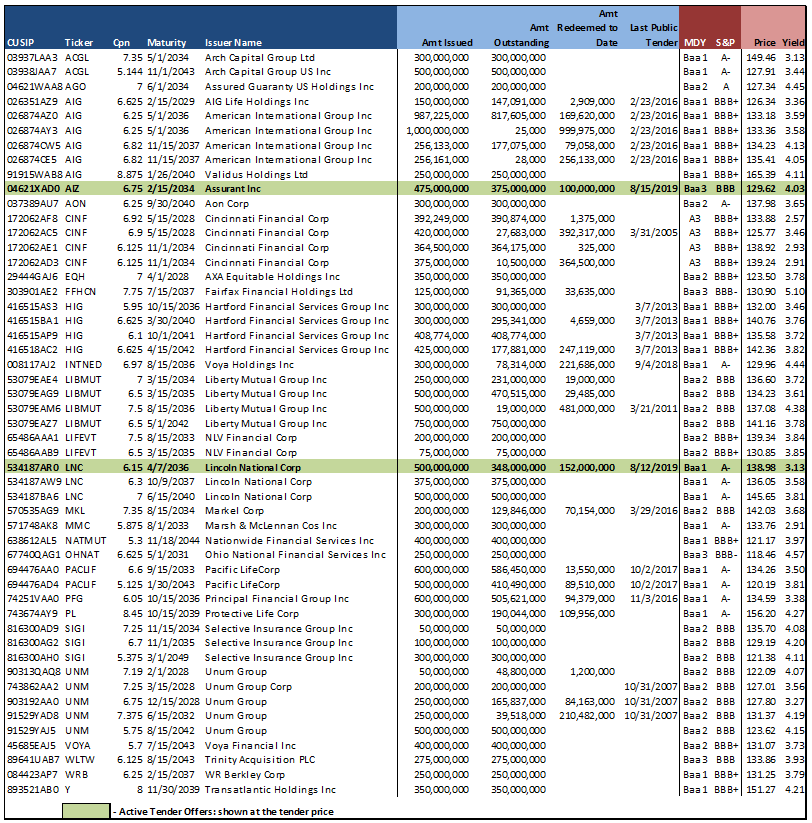

Exhibit 4: High coupon tender candidates – BBB insurance

Note: Active tender situations shown at tender level. Source: Bloomberg/TRACE indications, Amherst Pierpont Securities

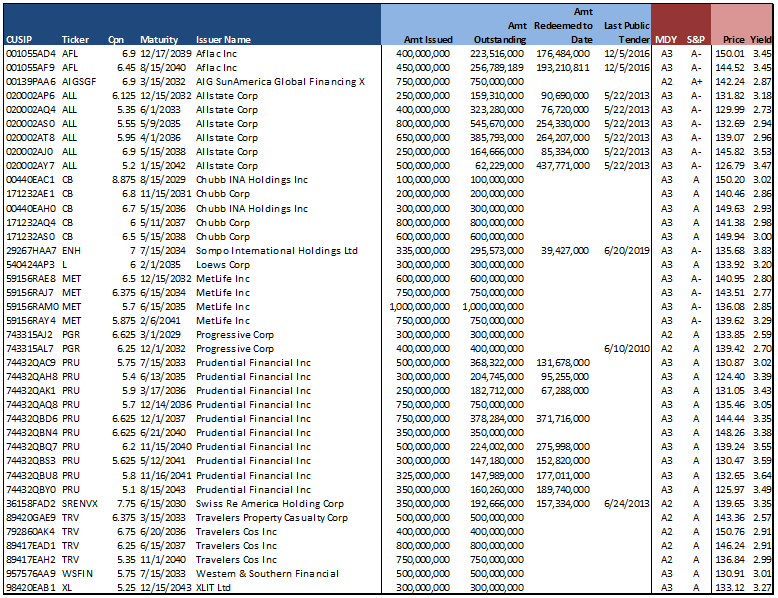

Exhibit 5: High coupon tender candidates – single-A insurance

Source: Bloomberg/TRACE indications, Amherst Pierpont Securities