Uncategorized

Argentina | Difficult choices: reform or default

admin | August 16, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

It’s understandable that Argentina Eurobonds have discounted a high probability of default. Indicators of cash flow stress and solvency have worsened under the assumption of a non-reformist government. The latest treasury auction has reaffirmed restricted access to capital while the IMF program has already front-loaded funds with no other obvious lender of last resort. The Macri administration looks likely to avoid default by drawing down scarce FX reserves, running up arrears and using other regulatory measures to contain FX stress. But the intensity of the cash flow stress likely early next year should force the Fernandez administration to quickly decide among difficult options. What are the choices for the next administration? Is default inevitable?

The challenge is regaining access to funding if the Fernandez administration chooses default over economic reform. Without access to capital, the Fernandez team would face forced austerity. The political options are difficult. The majority of population rejects economic reform, and there are ideological constraints within the coalition. It’s a tradeoff between the political constraints of economic reform versus the cash flow constraints on restricted access to capital. The default could be orderly via coordination of an IMF program, with debt sustainability being reassessed after the latest ARS weakness.

It’s possible the Fernandez team shifts towards responsible governance after understanding the economic realities once in office. However, the initial signals have all been worrisome with no apparent understanding of basic economic principles showing up in the populist campaign rhetoric and no sensitivity to the recent financial stress. There is a comfortable 15% margin of voters that allows for a shift towards more moderate rhetoric. The prospects for a more responsible approach would improve if there were an official announcement of a well-respected technocrat as economic advisor or the creation of a transition team to discuss interim policy measures. Despite the recent meeting with President Macri, candidate Fernandez lost the opportunity to name-drop a well-respected technocrat when asked about his cabinet while also discouraging any collaboration to minimize market stress. There has also been no effort to disassociate from the more radical factions of the coalition or clarify a rational economic program. The markets assume the worst based on the interventionist and isolationist strategy of the Kirchner era, and it’s difficult to expect the best without any encouragement from the Fernandez team.

Fernandez may be forced to clarify IMF relations on the risk the fund withholds the September 15 $5.4 billion payment in potential 1:1 meetings with the IMF this coming week during the assessment of the fifth program review. The longer that Fernandez waits to reassures markets, the worse the cash flow stress and the higher the probability of default from lower FX reserves and weaker FX rate. It’s worrisome that the political agenda dominates the economic agenda despite these risks. It may already be too late to avoid default after the recent ARS weakness pushes debt ratios far above 87% of GDP as of the end 2018. The next few months will be increasingly challenging on cash flow management. The risk for precarious liquidity post political transition will require huge effort for fiscal adjustment or cash flow relief on debt restructuring.

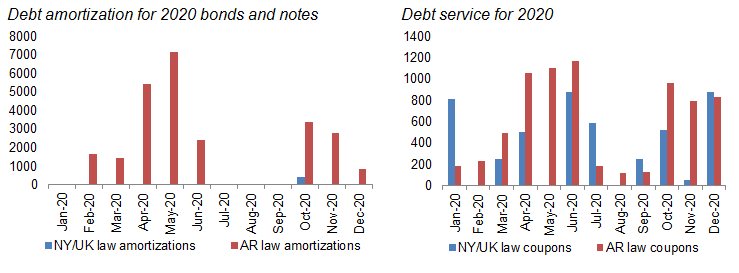

Exhibit 1: Looming debt repayments and debt service

Source: https://www.argentina.gob.ar/hacienda (includes repos and based on latest official data and ARS 3/31/2019), Amherst Pierpont Securities

There has been increasing debate about the context of default and the obvious vulnerability of the domestic debt stock. It’s a similar breakdown of local law at 27% versus 31% for NY law of the total stock of bonds and notes; however 2020 amortizations are more onerous for local law bonds (Exhibit 1). The selective or initial default on local debt could provide some efficient savings against the complications of external default. There has been a track record of distressed locally based exchanges at the first stage of rollover stress based on the perception that local investors are partners in crisis. However, voluntary distressed debt exchange and forced restructurings locally may not open access to capital markets or provide sufficient savings against the large gross financing needs. It’s not clear that external investors would provide fresh funds in light of reluctance to reform and enthusiasm to default. This is also true on negotiations to restructure external debt. The alternative of inward isolation, as in 2001, is not realistic based on low stock external assets, limited access to capital and still a cash flow deficit on the fiscal and external accounts. This could eventually reconcile the alternative of IMF sponsorship for private sector involvement (PSI) that would provide the context for a more orderly restructuring. The initial challenge will focus on managing the cash flow stress through the October 27 elections and the declining margin of flexibility on the delays to commit to a coherent economic program.

The first bounce on Eurobond prices looks more like a technical bounce after successive days of weakness with some support as bond prices converge near historic sovereign recovery value levels. The current levels on Eurobond prices would provide a clear buying opportunity if President Macri avoids default and capital controls and then the opposition delivers a positive shock with a pro-reform mandate post elections. It is too soon to say the market has reached a floor for the high correlation between ARS and solvency ratios on the 76% dollarization of the debt stock. Modeling recovery value is challenging based on the fluidity of the macroeconomic inputs, the high sensitivity to ARS projections and the lack of firm commitment from the Fernandez administration to the current economic model and IMF program. Assuming a non-reformer bias, then this would imply no further fiscal consolidation that could constrain growth prospects and demand a haircut on external debt to maximize savings necessary for debt sustainability. The debt restructuring scenario under an IMF program could allow for an orderly process while any independent restructuring would suggest worst case scenarios and recovery value below current levels.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.