Uncategorized

Banks become negative on negative convexity

admin | August 1, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

The shift towards an easier stance of monetary policy has ushered in lower rates, which inevitably leads to a pick-up in refinance activity. Anecdotally, some banks have recently started to partially mitigate the negative convexity risk by underweighting agency pass-throughs and CMOs in favor of overweighting longer duration, positively convex agency CMBS. The migration has coincided with moderately tightened spreads, particularly in the larger and well diversified Freddie Mac K deals, but the paper still looks competitive versus equivalently rated corporates and benefits from better liquidity.

The only good refi is your own

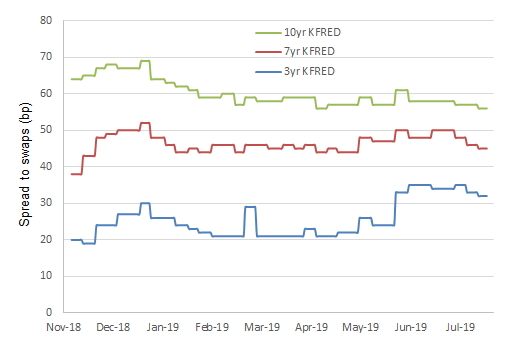

A recent uptick in bank buying of agency CMBS is likely a defensive move in response to a pick-up in refinances that has already started to emerge in agency prepay reports. Freddie K-deal fixed rate classes are commercial mortgage pass-throughs which are locked out from prepayments for most of the life of the security, so they effectively perform like fixed rate bullets and exhibit positive convexity. Since late June spreads on the fixed-rate A classes have tightened by several basis points across the maturity spectrum (Exhibit 1).

Exhibit 1: Freddie K-deal spreads have recently tightened

Source: Amherst Pierpont Securities

Competitive spreads, better liquidity than similarly rated corporates

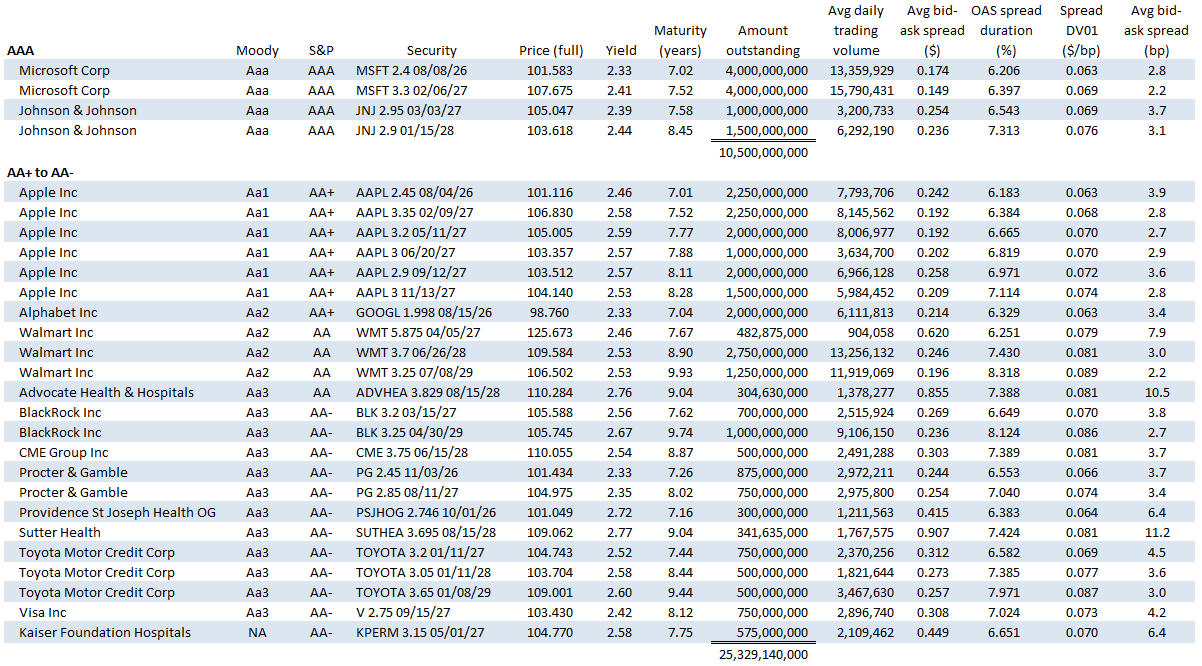

Banks, insurance companies and other investors that need AAA to AA rated bonds without the negative convexity don’t have a lot of options, particularly in the longer end of the curve (Exhibit 2). There are two AAA rated corporate issuers – Microsoft and Johnson & Johnson – with $10.5 billion of paper currently outstanding in the 7-10 year part of the curve. In the AA+ to AA- category there are 12 issuers with $25.3 billion outstanding, though several of the names have only a single bond outstanding in the sector.

Exhibit 2: Highly rated US investment grade corporates (7-10 year sector)

Note: Average daily trading volume and average bid-ask spread in dollars are estimated by Bloomberg using TRACE data and BMRK pricing and algorithms in their liquidity analysis. Prices from Bloomberg BMRK as of 7/31/2019. Includes senior unsecured AAA to AA- rated corporate issues with at least $300 million outstanding.Does not include supra sovereigns or foreign development banks. Source: Bloomberg, Amherst Pierpont Securities.

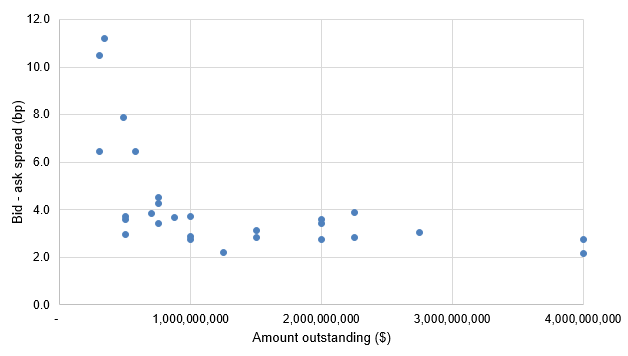

Liquidity in corporate bonds suffers both as size decreases (Exhibit 3) and the issue ages. A good example of this is seen in the WMT 5.875 4/5/27, which has below $500 million outstanding, was originally issued as a 20-year bond and has less than 7 years left to maturity. The liquidity of the bond is quite low, with an average daily trading volume below $1 million notional and a bid-ask spread of 7.9 bp. Not surprising that few investors want to part with a highly rated, high coupon, decade off-the-run bond in this environment, but it is symptomatic of the liquidity challenges in the highest grade corporate sector generally. Of the 27 issues shown, all but one of them was originally issued as a 10-year security, and only two of them were issued within the last six months.

Exhibit 3: Bid-ask spreads widens as issue size decreases

Note: Average bid-ask spread in basis points calculated from bid-ask spread in dollars, prices and OAS spread duration from Bloomberg.Source: Bloomberg, Amherst Pierpont Securities.

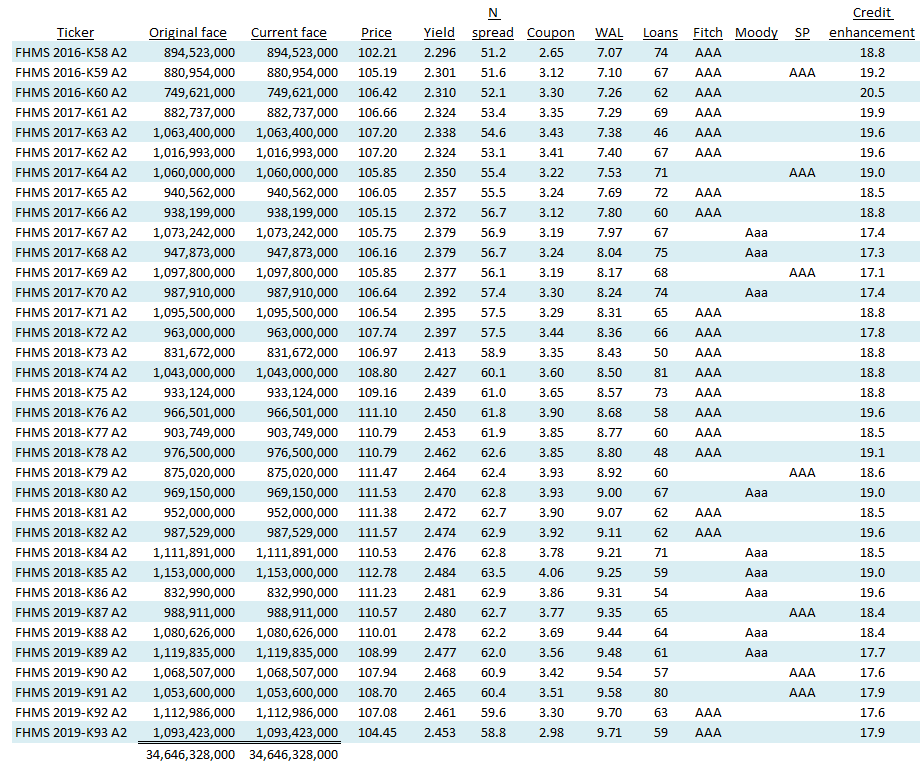

The fixed-rate, reliably AAA-rated at issuance piece of a Freddie K deal is the A2 class. A group of standard deal, multifamily pass-through A2s with weighted average life between 7- to 10-years is shown in Exhibit 4. There is $34.6 billion of this AAA-rated paper outstanding across 35 deals, with an average number of 64 multifamily loans underlying each security and 19% credit enhancement on average. Yields range from 2.30% to 2.48%, which is competitive to slightly higher than those available in investment grade corporate AAA paper in the same sector. Freddie K-deals have grown in size and frequency of issuance over the last several years, with typically at least one to two deals printing each month.

Exhibit 4: Freddie K-deal A2s outstanding, (7- to 10-year sector, list not exhaustive)

Note: All prices and spreads from Bloomberg as of 7/31/2019. Source: Bloomberg, Amherst Insight Labs, Amherst Pierpont Securities.

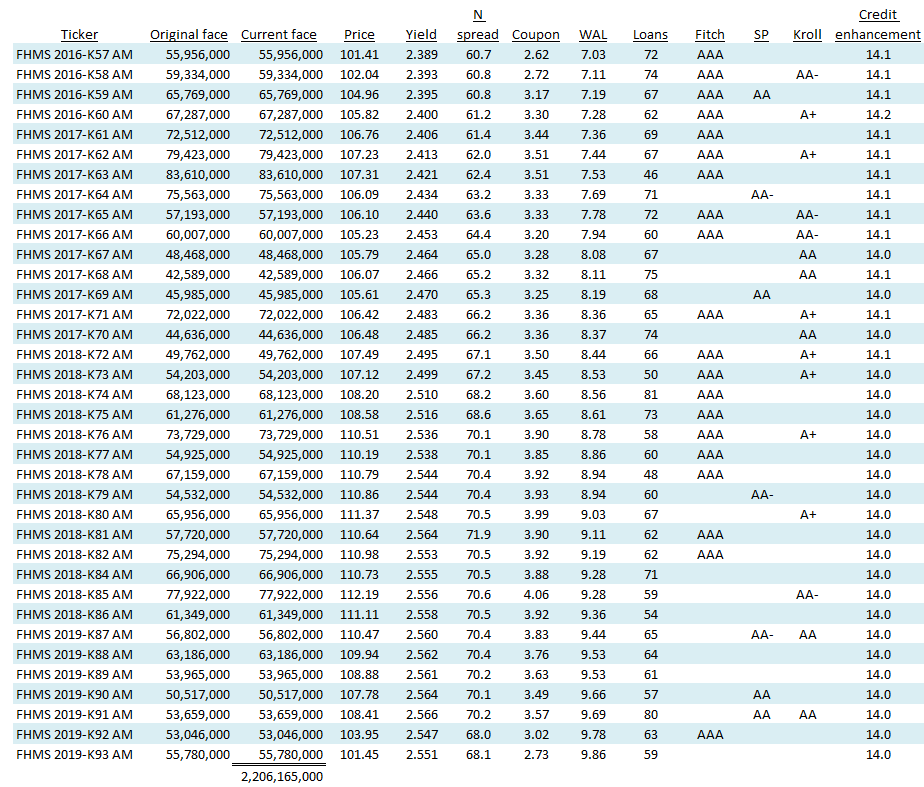

Freddie K investors can pick up yield by going down in credit to the AM class, which is typically rated Aa3/AA- to A1/A+ on the underlying collateral (Exhibit 5). Fitch and Moody’s rate these classes AAA because, like all of the A classes, they are wrapped with the Freddie Mac guarantee for timely payment of interest and ultimate payment of principal. Other ratings agencies incorporate the lower credit enhancement of the AMs compared to the A2s, as well as a variety of other metrics of the underlying collateral and structure into their ratings, before the bond is wrapped with the guarantee.

There is also a few basis points of extra yield available in the smaller Freddie K programs, such as the K-W deals which securitize workforce housing. The issuance is less frequent and the deal sizes are somewhat smaller, but the A classes are also wrapped with Freddie’s guarantee.

Exhibit 5: Freddie K-deal AMs outstanding (7- to 10-year sector, list not exhaustive)

The AMs currently yield from 2.39% to 2.56%, also competitive with the AA+ to AA- corporates in the same sector. The AM class tends to be much smaller than the A2, with only $2.2 billion total outstanding of the deals shown, and averaging $60 million face per deal.

FINRA does not provide a detailed breakdown of pricing or trading activity for structured products, though there is some aggregated data available on their website here. Trading volume in investment grade agency CMBS on 7/31/2019 was $440 million in market value across 100 trades and 44 unique securities. The breakdown by maturity sector, deal type and issuer is obviously unknown, but Freddie K deals are the deepest, most liquid market segment in agency CMBS. For comparison, the total estimated daily trading volume across all of the AAA to AA- corporate bonds shown in Exhibit 2 is $148 million.

The other benefit in agency CMBS is the greater liquidity provided by the dealer community in support of the programs. Freddie K A2 and AM paper tends trade in a 1 to 2 bp bid-ask market on spread, keeping the cost of trading paper relatively low even for the smaller sized AM deals and any seasoned paper.