Uncategorized

CFPB policy shift could lift value in high DTI loans

admin | July 26, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

The Consumer Financial Protection Bureau announced in recent days it would let special Fannie Mae and Freddie Mac provisions of the Qualified Mortgage rules expire as scheduled on January 10, 2021. Under these provisions, among other things, the GSEs can now securitize loans with debt-to-income ratios above 43%, and these high DTI loans have made up a substantial share of production in recent years. If the provisions do expire, high DTI borrowers should face higher costs for mortgage debt, and the value of MBS pools backed by existing high DTI borrowers should rise.

GSE issuance of high DTI loans has soared

Since inception the Qualified Mortgage rules have included special provisions for loans guaranteed by Fannie Mae and Freddie Mac. Certain loans that otherwise would be considered non-qualified gain qualified status when guaranteed. Perhaps the most significant exemption from the QM rules granted to the GSEs concerns loans with DTIs greater than 43%. These loans gain QM status only when they are guaranteed by the GSEs, and QM status provides lenders with additional protection from lawsuits. Therefore most lenders prefer to securitize these loans with the GSEs, and the share of GSE loans with DTI above 43% has run up rapidly (Exhibit 1).

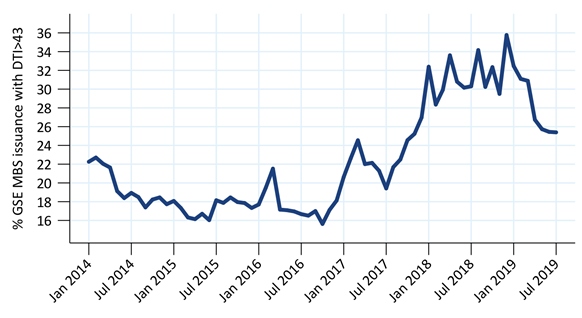

Exhibit 1: A large share of GSE loans has DTI greater than 43%

Note: TBA-deliverable 30-year pools, excluding specified pools. July issuance is month-to-date. Source: Fannie Mae, Freddie Mac, eMBS, Amherst Pierpont Securities

From 2014 through 2017, high DTI loans comprised 15% to 20% of GSE monthly issuance. In late 2017, the GSEs made changes to the underwriting requirements for these loans. The new policy reduced the documentation requirements for high DTI loans and permitted more compensating factors. GSE issuance of high DTI loans soared to 30% to 35% for most of 2018. The share of issuance has fallen in 2019, likely due to a rise in refinancing and a pick-up in new pool issuance. But high DTI loans still account for over 25% of monthly supply.

Borrowers could face higher rates when the exemption expire

If the current GSE QM exemption expires, lenders will need to price in the additional costs—liquidity, legal, underwriting and other—associated with non-QM loans. This should increase the rate a borrower receives on a new loan. The magnitude of the increase can be estimated from prime non-agency securitizations, which include loans with DTI above and below 43%.

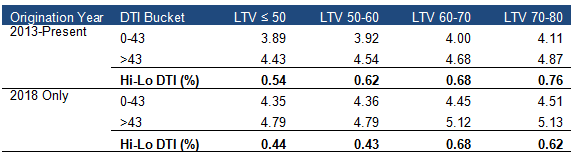

The data suggest a DTI above 43% could lift a borrower’s mortgage rate by 50 bp or more (Exhibit 2). From 2013 to the present, and, more narrowly, in 2018 only, the average securitized prime jumbo loan with DTI above 43% had a higher note rate than loans below 43%. The difference tended to rise with LTV. Last year, for example, loans with a FICO of 760 to 800, an LTV of 50 or lower and a DTI of 43% or below had an average rate of 4.35%; loans with similar FICO and LTV but a DTI above 43% had an average rate of 4.79%–a 44 bp difference. Loans with an a FICO of 760 to 800, an LTV between 70 and 80 and a DTI of 43% or lower had an average rate of 4.51%; similar FICO and LTV loans with a DTI above 43% had an average rate of 5.13%–a 62 bp difference.

Exhibit 2: Prime jumbo loans with a high DTI have higher rates than similar loans with a lower DTI

Note: All loans 760-800 FICO with balances that exceed local market GSE loan limits. This analysis does not control for other factors such as occupancy, documentation, geography and others. Source: Amherst Pierpont Securities

Assuming a 50 bp rise in rates for high DTI loans seems reasonable if the special GSE provisions expire. This should act as an elbow shift that reduces the borrower’s incentive to prepay.

Slower speeds increases the value of these loans

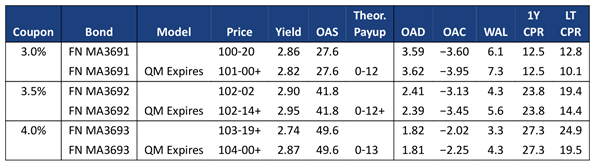

Yield Book’s prepayment model was used to estimate the theoretical pay-up on 100% high DTI pools assuming the GSE provisions expire in January 2021 and refinancing rates for these borrowers rise by 50 bp (Exhibit 2). Three benchmark pools were selected, with coupons of 3.0%, 3.5%, and 4.0%. Each pool is the June 2019 Fannie major pool. Each pool was priced at the TBA OAS using Yield Book in two scenarios—using the baseline model and using a dialed version of the model that incorporates the 50 basis point elbow shift beginning in January 2021. Speeds are identical to the undialed model prior to January 2021. The price difference between the two scenarios gives the theoretical value of slower prepayment speeds.

Exhibit 3: Theoretical payups if High DTI exemptions ends in January 2021

Source: Fannie Mae, Freddie Mac, eMBS, Amherst Pierpont Securities

The analysis assumes that DTI has no influence over current prepayment speeds since the GSEs are issuing such large numbers of high DTI loans. The pay-up is similar for all three pools, with the 3.0% increasing $0-12 and the 4.0% increasing $0-13.

Political obstacles to expiration of GSE provisions

This decision by the CFPB is likely to be strongly opposed by many in the industry. Originators, servicers, realtors, and builders would all be hurt if origination volumes decline. Consumer advocates would like oppose the reduced access to credit. It is also possible that a significant reduction in loan origination could hurt home prices. Because of potential public response, the CFPB announced it intended to seek public comment on revising the QM rules. Revision may mean that some or possibly all of the GSE special exemptions get renewed.

The January 10, 2021 expiration date also adds a wrinkle. It falls between the next presidential election and the date when the next administration gets inaugurated. Even if the next administration and Congress take a different view on this issue, there may be no replacement for the expired provisions until after the next inauguration.

Investors realistically should weight potential gains on 100% high DTI loans by the likelihood that the GSE exemptions would expire. At a small price premium to new pools, however, 100% high DTI could be an inexpensive option on a significant policy change.