Uncategorized

Outside the bank’s front door: lending as a part of portfolio strategy

admin | July 19, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Banks in the US and worldwide have long focused their debt portfolios on loans and still hold a commanding share of lending in most markets. But nonbank debt portfolios at US hedge funds and private equity funds, life insurers, broker/dealers and REITs also play important roles. They turn to lending for things not always found easily in securities and not well known to many securities investors. Higher yield, better diversification, more control and scale usually top the list.

Loans often offer higher yields than securities to compensate for lower liquidity and more operating risk, and loans commonly come with risk profiles that help diversify securities portfolios. Investors often have more direct control over loan servicing and loss mitigation, reducing potential conflicts of interest—between investors, administrators and servicers—that come with securitization. And some lending niches can absorb sizable capital.

Details of bank lending show up clearly in regulatory reports, but the details of nonbank lending are harder to pin down. Nonbank assets and forms of exposure are reported at best in large aggregates and often mixed with bank activity. Nonbank loan terms and borrowers rarely appear. Proprietary lenders often limit disclosure and rarely volunteer guidance or advice.

Debt portfolios considering loans can still piece together a view of the market beyond banks, thrifts and credit unions, beyond the boundaries of government agencies such as Fannie Mae, Freddie Mac, Ginnie Mae or the Small Business Administration, and beyond securitization vehicles. This leaves the activity of portfolios that make loans as part of a broader debt strategy. The view comes from a few angles:

- The size and type of current nonbank diversified private lending

- The investment case for lending by nonbank portfolios

- Key operating challenges

THE SIZE AND TYPE OF NONBANK DIVERSIFIED PRIVATE LENDING

Of the nearly $68 trillion in private US debt outstanding at the end of 2018, 63% came from debt securities and 37% from loans (Exhibit 1A). Securities have taken share from loans steadily since the early 1970s as securitization and corporate debt markets have grown. Using banks’ and other depositories’ share of total debt as a proxy for loans, the share of private debt originated as loans has stabilized in recent years and edged up slightly (Exhibit 1B).

Exhibit 1: Securities dominate debt funding in the US

Note: $ Billions as of 2018. Source: Z.1 Financial Accounts of the United States, June 6, 2019. Amherst Pierpont Securities

Banks and other depositories held more than 45% of the $25 trillion of loans outstanding in the US at the end of 2018, nearly 20 percentage points higher than the next largest holder (Exhibit 2). Of remaining holders with more than 1% of outstanding loans, a number are government lenders or securitization vehicles: GSE mortgage pools (24.8%), federal, state or local governments (7.3%) or issuers of asset-backed securities (4.1%). One largely represents foreign bank lending into the US: rest of the world (3.1%). That leaves a set of diversified nonbank private debt portfolios: finance companies (4.2%), households, hedge funds, private equity and nonprofits (3.5%), life insurers (3.0%), broker/dealers (1.5%) and REITs (1.1%). Diversified nonbank private portfolios have a collective share of 13.3%.

Exhibit 2: Banks dominate lending, but a handful of diversified private portfolios have key roles

Source: Z.1 Financial Accounts of the United States, June 6, 2019. Amherst Pierpont Securities

The diversified nonbank private portfolios held $3.3 trillion in loans at the end of 2018 and clearly compete with banks, securitization and government programs to lend. Federal Reserve data suggest the largest categories of nonbank diversified private lending include business loans, margin loans, mortgages and consumer credit (Exhibit 3). Finance companies, hedge funds, private equity, households and nonprofits dominate business loans while broker/dealers hold margin loans. Life insurers and REITs dominate mortgage loans. And finance companies dominate consumer credit.

Exhibit 3: Nonbanks hold large amounts of business loans, mortgages and consumer credit

Note: Other loans and advances include nonfinancial corporate business loans, syndicated loans and margin loans, among others. Mortgages include loans secured by single- and multi-family residences, commercial property and farms. Consumer credit includes credit card, auto, mobile home, education, boat, trailer and vacation loans. Source: Z.1 Financial Accounts of the United States, June 6, 2019. Amherst Pierpont Securities.

One area on the border between lending and securities is repurchase agreements, or repo. Repo involves the sale of an asset to a buyer and a simultaneous agreement to repurchase the asset at a specified price in the future. The seller holds or reinvests cash and the buyer holds the asset until the repurchase date. The difference between the sale and repurchase price in part often represents an interest rate on the cash held by the seller. Repo consequently is a form of lending secured by the particular asset.

Broker/dealers that lend to clients dominated the $4.1 trillion in pooled repo and fed funds loans reported by the Federal Reserve and outstanding at the end of 2018. Money market funds that lend to broker/dealers and others, depositories and government sponsored enterprises such as Fannie Mae and Freddie Mac also participate heavily (Exhibit 4). State and local governments, mutual funds and businesses also held repo loans, along with a string of investors that held several billion dollars each in these loans.

Exhibit 4: A wide range of portfolios hold repo loans

Source: Z.1 Financial Accounts of the United States, June 6, 2019, Table L.207. Amherst Pierpont Securities.

The vast majority of repo lending is secured by US Treasury debt or agency and private mortgage-backed securities. These securities, along with a few others, are generally eligible for special protections for the lender under US bankruptcy law.

The boundary between repo and lending gets further blurred when loans secured by assets eligible for repo get structured as repo loans. Traditional repo lending uses securities with readily available market prices, but investors can also make repo loans secured, in turn, by portfolios of loans or other assets without readily available prices. The loans get structured as repo to take advantage of protections under US bankruptcy law that allows repo lenders to liquidate collateral usually without bankruptcy court review.

THE INVESTMENT CASE

With limited or no public disclosure of lending terms, the investment case for lending has to rest on selected case studies. The outlines of lending structured as repo tend to be more available, so analysis naturally trends toward repo lending. A few examples illuminate at least that part of the market.

Repo against securities

Investing in repo collateralized by securities can generate more yield than investing in comparable securities directly. But making the comparison isn’t always easy. The maturity and risk profile of the repo and the security can differ significantly. When the comparison is close, the yield difference is clear. For instance, 30-day term repo secured by Treasury bills and agency discount notes pays a higher yield than the cash securities (Exhibit 5). The higher yield reflects the difference between the cash securities, which can be sold and settled the same or the next day, and the repo, which stays in place until maturity. A 30-day term repo secured by agency pass-throughs, CMOs or other securities trades at even higher yields reflecting the additional mark-to-market risks in the collateral, but the risk profiles of the repo and the MBS or CMO collateral are very different.

Exhibit 5: Indicative terms on repo against liquid securities

Source: Amherst Pierpont Securities indicative repo levels as of 7/19/19.

Repo against residential mortgages

A range of investors have built portfolios of residential loans that do not meet regulatory requirements for a Qualified Mortgage or QM loan. These non-QM loans often go to smaller investors, self-employed borrowers, foreign borrowers and borrowers with a trailing foreclosure or bankruptcy.

While investors in non-QM loans often use securitization to get permanent financing, they also typically need repo or warehouse financing to grow the portfolio before securitization. While the debt issued through securitization has a much longer life, it still helps benchmark the initial financing costs (Exhibit 6). A hypothetical securitization in today’s market could issue ‘AAA’ through ‘BBB’ classes for the equivalent of a 3.5-year loan with an 80-90 bp spread to the swap curve and a 90% advance rate. This compares to an unrated 1- to 2-year repo or warehouse loan with a spread of 150 bp to 200 bp and a 90% to 95% advance rate. The loan investor would draw on the warehouse line as the portfolio builds and then repay at securitization. To provide flexible liquidity to the owner of the loans and take the operational risk of building the portfolio, the lender gets a yield premium.

Exhibit 6: A comparison of non-QM securitization to warehouse lending

Source: Amherst Pierpont Securities

The market has also seen a steady flow of seasoned re-performing and non-performing loans along with REO or real estate owned after foreclosure in the wake of the 2008 financial crisis. The re-performing loans typically come from modifications of both seasoned agency and non-agency loans, and the non-performing loans and REO come from a wide range of sources. Re-performing and non-performing loan portfolios have used securitization for financing (Exhibit 7). The ‘AAA’ to ‘A’ classes of a typical re-performing securitization create the equivalent of a 5-year loan with 110-120 bp of spread to the swap curve and a 90% advance rate. This compares to a loan secured by re-preforming loans and any loans that subsequently go non-performing or REO. The loan gets structured as a 364-day maturity, to fall within the legal definition of a repo, with a mutual option to extend for another 364 days. This unrated repo loan comes with 150 bp to 200 bp of spread and a 90% advance rate.

Exhibit 7: A comparison of RPL securitization to warehouse lending

Source: Amherst Pierpont Securities

Repo against single-family rental housing

Portfolios of single-family properties available for rent have become a new niche in mortgage finance since 2012. The drop in home values and the rise in borrower delinquency and default during and after the 2008 financial crisis created a supply of available single-family properties and former homeowners that needed housing. The US homeownership rate fell from a peak of 69% before the crisis to 64% today. Institutional investors began building portfolios of rental homes. More than 20 institutional investors have operated in this market. These investors need financing to build and run their portfolios.

Repo lending and portfolio finance compete with securitization to fund portfolios of single-family rental property. Progress Residential 2018-SFR3 issued more than $1 billion in 5-year debt in October 2018 secured by single-family rental properties (Exhibit 8). The ‘AAA’ through ‘BBB’ classes combine into the equivalent of a 5-year loan with 107 bp of spread to the swap curve and a 75% advance rate. This compares to a private 3- to 5-year unrated term loan with roughly 175 bp of spread to the swap curve and approximately a 75% advance rate against the portfolio broker price opinion on the properties. In exchange for an unrated loan, less liquidity and more operating risk, the investor picks up material yield.

Exhibit 8: A comparison of SFR securitization to portfolio finance and warehouse lending

Source: Amherst Pierpont Securities

Repo against transitional commercial real estate

Owners of commercial real estate hoping to upgrade their properties and either sell or attract new tenants have helped create another niche market in lending. The real estate owner often takes out a transitional loan, stabilizes the property and then either sells or refinances into a more permanent loan. The transitional loans often have maturities too short to fit in traditional conduit commercial MBS, with often come with options to extend maturity that also make them a hard fit to conduit CMBS. Transitional commercial real estate loans also usually have floating-rate coupons instead of the fixed coupons of traditional conduit CMBS. And the possibility that the lender may need to modify other terms makes the loans difficult to securitize in a REMIC. The originators of transitional CRE loans can finance them through CRE CLOs, but investors can also finance the loans through a warehouse loan (Exhibit 9).

Exhibit 9: Indicative terms on transitional CRE warehouse lending

Source: Amherst Pierpont Securities

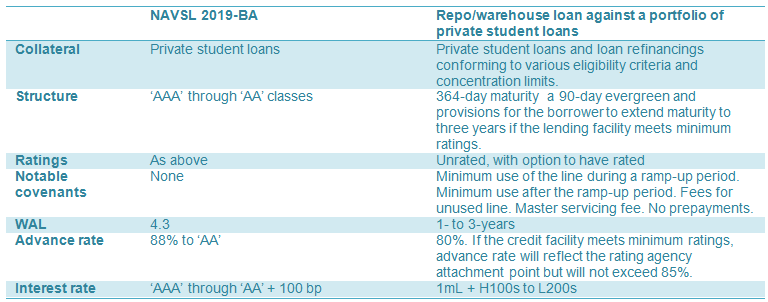

Repo against consumer loan portfolios

Nonbank lenders periodically have opportunity to provide repo or portfolio finance for consumer loans. These loans can include a detailed list of provisions protecting against deterioration of portfolio credit quality. Since the originator may need a time to build up a portfolio large enough for securitization, the portfolio finance loans also can ensure that the lenders gets a least a minimum draw on the financing line or a minimum fee. Loans also can include provisions for having the lending arrangement rated, which usually improves terms for the borrower. And like loans against other types of assets, the loans can get split into senior and mezzanine classes with different yields and weighted average lives (Exhibits 10 and 11).

Exhibit 10: Indicative terms on warehouse financing a portfolio of private student loans

Source: Amherst Pierpont Securities

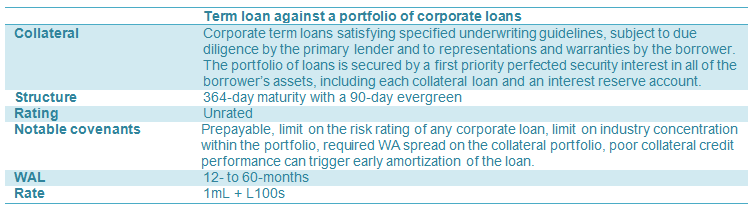

Repo against portfolios of corporate term loans

The growth of the leveraged loan market from $500 billion in late 2010 to more than $1.2 trillion in 2018 has created demand for financing portfolios of corporate loans while managers of collateralized loan obligations, or CLOs, build portfolios. Middle market lending has also expanded, with annual new loan volume from 2010 through 2018 ranging between $50 billion to $110 billion. Loans to finance these portfolios of corporate debt can involve a claim against the loan portfolio and other assets of the borrower. The funding terms can also involve a wide range of covenants governing prepayment, allowable risk in the corporate loans and triggers to amortize or call the loan if collateral quality deteriorates (Exhibit 11).

Exhibit 11: Indicative terms on repo against a portfolio of corporate term loans

Source: Amherst Pierpont Securities

OPERATING CHALLENGES

Lenders often choose to make repo or term loans against financial assets they already hold or may hold in portfolio. Investors in RPL or NPL securitizations, for example, may choose to lend against similar loans. Investors in private student loan ABS may similarly choose to lend against private student loan portfolios. Investors in single-family rental securitizations may choose to lend against portfolios of rental properties. This helps if the lender is ever forced to seize the loan collateral. A lender familiar with the collateral not only knows more about its risk, value and liquidity, but the lender also is more likely to know service providers—servicers, administrators, collectors, brokers, data providers and so on—to help manage or liquidate the asset. Lending extends the portfolio manager’s expertise.

A lender’s exposure to the loan originator and servicer in the case of direct lending or to the loan owner in the case of a loan secured by a loan portfolio creates a distinct layer of operational risk and control. Asset quality either in lending or securitization can depend on the counterparties’ financial and operating stability. Counterparties running into trouble can reduce the time, effort and other resources used to monitor and manage the assets, leading portfolio quality to decline. Lenders and investors in securitization both need to monitor counterparty performance. But lenders often have an easier time of actively managing counterparty risk. Lenders can pursue their own interests instead of coordinating with administrators, servicers and other investors in a securitization.

Portfolio lenders and direct lenders also often need an administrator to help monitor both collateral and counterparty quality, especially if covenants in the loan agreement could trigger new terms. The administrator needs to set up a system to provide regular data and updates.

COMPETITION

Banks continue to dominate most categories of lending through relationships, broad awareness among potential borrowers and through diverse, flexible and often inexpensive sources of funds. Flexible bank funding is particularly worth noting. In many warehouse lending arrangements, for instance, the borrower’s demand for funds can vary significantly as loan origination rises and falls. Banks, with their diversified lending books and years of experience in asset-liability management, can often match funding to the borrower’s demand. However, banks also have to abide by capital and liquidity regulations that can hamper efficient lending in some segments, and by stress testing regimes that can add capital requirements for different types of loans.

Larger banks with a national footprint also tend to need significant scale to justify lending into a particular market segment, limiting their efforts in some otherwise profitable niches. The underwriting, marketing, information processing, accounting, legal and compliance costs drive the need for scale. This opens the door for nonbank lending to smaller segments.

Smaller banks, on the other hand, often lend only within a limited geographic footprint. That footprint might not justify development of lending programs that look small within any particular area but much larger across a number of regions. That also opens a door for nonbank lenders.

In general, banks have migrated away from mortgage lending in the last 10 years and toward commercial and industrial and other types of lending (Exhibit 12). The shift could reflect change in demand for these types of loans as easily as it could change in bank willingness to lend. If the change is in demand, all lenders have lost an opportunity. If the change is in bank appetite, it opens the door to other lenders.

Exhibit 12: Banks have migrated away from mortgage lending and toward other types

Source: SNL for the 38 US commercial banks with more than $30 billion in total assets as of 1Q2019. Amherst Pierpont Securities.

Life insurers have encountered low yield for years and, with long liabilities, can hold assets on their balance sheet that lack readily available market liquidity. Life insurers also have asset-liability management expertise that can help them match funding to borrowers’ demand.

More traditional managers of mutual funds or separate accounts also have come under pressure from passive investing and exchange traded funds or ETFs. If asset managers can find pools of capital willing and able to take on lending exposures and the accompanying liquidity and operating risk, then this kind of investing helps form a bulwark against some of the pressure from passive management and ETFs. Passive management and ETFs reflect the increasing influence of scale on asset management. Any investment strategy that can be scaled is highly likely to show up in an ETF with relatively low fees. This goes not just for strategies that track market indices but for some that systematically select different types of securities, such as strategies that fall under the umbrella of smart beta. Asset managers, whether on a platform best known for managing mutual or hedge funds or at insurance or pension funds, will likely have their performance and fees compared to similar passive funds or ETFs. Since lending is less subject to scale economies, passive vehicles should have more trouble competing against portfolios able to offer lending exposure.

Traditional asset managers do run into challenges matching funds to borrowers with demand that varies significantly over time. Traditional managers usually avoid contingent funding. This puts managers at a disadvantage to banks and insurers with more flexible sources of funds. Managers can still make loans that fund a borrower’s minimum level of demand, and could make additional loans in the future based on prevailing market conditions.

Institutional investors increasingly can source systematic market exposure or beta inexpensively through passive vehicles and spend the bulk of their fee budget on more valuable alpha, which will often come in the form of investment exposures or strategies that the investors cannot reproduce on their own. Lending is arguably one way to offer alpha exposure.

* * *

Nonbank lending will likely always be a niche market operating just outside the bounds of bank and government programs and securitization, but it is a niche that can play a valuable portfolio role. Additional yield, different risk profiles and control makes various forms of lending attractive if the investor can take the illiquidity of lending and manage the complexity and operational risk. Banks still face tight regulatory controls put in place after the 2008 financial crisis—controls that almost certainly make the financial system more stable but also may limit credit to some creditworthy borrowers. This is where nonbank lenders stand to make their best investments. And in a market for asset management where any scalable investment quickly comes under margin pressure, lending also is a market where distinct expertise and operating capacity can get rewarded.