Uncategorized

Watching inflation expectations

admin | June 14, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

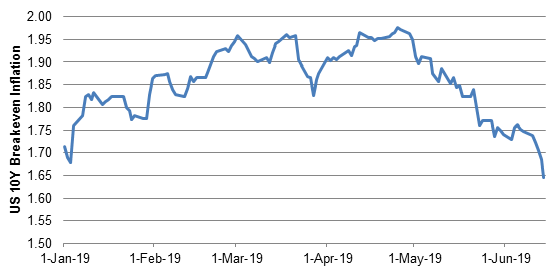

Of the nearly 40 bp drop in US 10-year rates since early May, 30 bp has come from lower expected inflation and the rest from lower expected real rates. Inflation implied by the spread between 10-year notes and TIPS now stands below 165 bp, the lowest level since late 2016. Low realized inflation worldwide hasn’t helped. Concern about inflation expectations may be the bigger reason the Fed might cut.

Implied 10-year inflation has dropped from 195 bp at the start of May to 165 bp lately (Exhibit 1). Core PCE has steadily dropped since December, so recent readings seem an unlikely immediate cause. New US tariffs on China announced May 9 arguably should have an inflationary effect, so it is hard to see cause there either.

Exhibit 1: A sharp drop in 10-year inflation expectations since early May

Source: Bloomberg

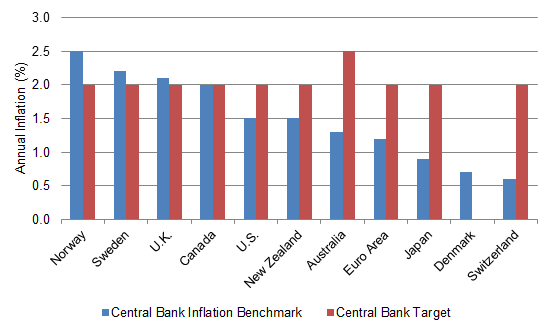

The world generally is awash in low inflation. Among the largest developed economies, only Norway, Sweden and the UK have inflation above the central bank target (Exhibit 2). Canada is at target. And the US, euro area and Japan, among others are below target.

Exhibit 2: Inflation in most developed economies is running below target

Source: Bloomberg

The Fed and other central banks clearly are struggling to understand post-2008 inflation. It has generally failed to respond to central bank efforts that seemed effective pre-2008. Reports from the early June Fed conference in Chicago, which drew a historic crowd of FOMC members, Fed staff, academics, Fed watchers and the press, also suggest a consensus that models of inflation are too uncertain.

Much of the orthodoxy of thinking at the Fed and worldwide has revolved around the importance of maintaining inflation expectations. Explicit inflation targets and forward guidance have become much more effective tools than market operations for managing price stability. Central banks have had to augment these tools with QE, but the combination still is likely powerful.

The Fed conference in Chicago also sent signals that the central bank would be willing to risk seeing inflation run above target partly because of perceived benefits to keeping labor markets tight. If market-implied expectations and survey expectations of inflation show further signs of weakening, a preemptive cut by the Fed could go a long way.

* * *

The view in rates

US 10-year yields continue to show some of the highest realized volatility of the year but have effectively moved sideways. With the Fed on June 19 and the G20 on June 28-29, volatility should continue into each meeting with some temporary respite after each. Fundamental fair value for 10-year rates remains around 2.50%, but uncertainty around tariffs and their impact should keep rates from getting there.

The market remains confident that the Fed will ease at the end of July. The implied probability of a cut is around 86%. The Fed should offer some guidance on June 19, but that guidance will likely be contingent on results from G20. If no credible resolution to US-China trade tension comes there—the mostly likely result—the market will likely assume that trade and tariffs are key part of the base case.

The view in spreads

Spreads in credit should continue to widen as trade frictions stay in play. It’s an appropriate repricing as prospective global growth comes under pressure. Agency MBS should outperform credit. Since the US announced new tariffs on China on May 9, MBS has performed much better than credit, and correlations suggest flows from credit into MBS. That should continue.

The view in credit

Corporate credit on the margin looks like it is improving from its state last year. Various measures of leverage paint a mixed picture, but many are improving. Companies have started to divert cash flow toward paying down debt, have started to sell non-core assets and have curtailed stock buybacks. Management has heard the concerns of debt investors. Households continue to look strong with low unemployment, rising home prices, and generally good performance in investment portfolios.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.