Uncategorized

A few lenders get a quick start at new refinancings

admin | June 14, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

A mortgage origination market with thin margins can easily turn originators into either the quick or the dead, but the drop in interest rates this year has given new opportunity for the quick. Prepayment speeds at some originators over the last few months have jumped 30% faster than peers’ while other originators have slowed against peers. It’s an early look at how originators and servicers are responding to the latest episode of low rates.

APS measures servicers’ prepayment speeds each month against their peers’ controlling for collateral attributes such as loan size, borrower credit score, geography and other influences on prepayments. The measure captures trailing 3-, 6- and 12-month performance. For each servicer and horizon, APS calculates the percentage faster or slower that servicer’s loans prepaid compared to the aggregate speed of collateral with similar attributes. The measure highlights the unique impact of the servicer.

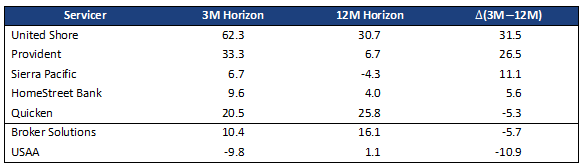

A few GSE servicers’ speeds picked up significantly over the last three months (Exhibit 1). The exhibit includes any Top 40 servicer, ranked by principal serviced, whose relative speeds changed by more than 5% either faster or slower. Two servicers prepaid much faster as rates fell—United Shore and Provident both jumped by roughly 30%. For example, United Shore pools prepaid 30.7% faster over 12 months but were much faster—62.3%—over the most recent three months.

Some servicers show better performance over the last three months. The most notable is Quicken, with relative performance that improved by roughly 5% as rates declined. USAA also bears mentioning as the most improved servicer of the group, suggesting these pools have flatter S-curves.

Exhibit 1: GSE servicer comparison (% above or below benchmark CPR)

Source: Fannie Mae, Freddie Mac, eMBS, Amherst Pierpont Securities

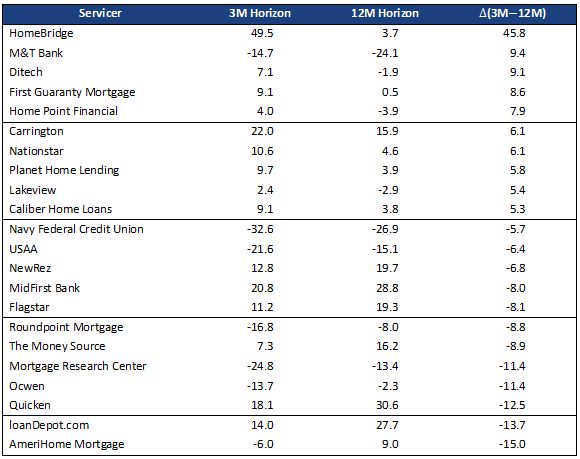

Change came in Ginnie Mae servicers, too (Exhibit 2). The largest change was by HomeBridge, which sold a significant amount of its servicing to NewRez (called New Penn at that time) in late 2018. At the same time, NewRez’s performance improved substantially, suggesting that loans with slower than typical prepayments were sold to NewRez, and that HomeBridge’s remaining loans prepay much worse than other servicers’ loans.

Quicken’s performance also improved substantially in Ginnie Mae pools, even more than the improvement in their GSE pools. loanDepot.com also improved, likely due to efforts to control prepayment speeds in order to be readmitted to Ginnie Mae’s multi lender pool program. Ginnie Mae removed loanDepot.com from the program in February due to poor historical prepayment speeds.

Exhibit 2: Ginnie Mae servicer comparison (% above or below benchmark CPR)

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

A loan servicer can have a large influence over whether a borrower will prepay. A servicer that also originates loans does not want a borrower to refinance with another lender, and individual loan officers and brokers have incentive to increase business through contact with former clients. Business practices vary by lender, and therefore so do speeds, so investors need to stay on top recent servicer behavior, especially as rates fall and open the door to new refinancing.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.