Uncategorized

So far, so good in the transition to UMBS

admin | May 31, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

One of the biggest changes in the history agency MBS, the blending of separate Fannie Mae and Freddie Mac TBA markets to a single one for uniform MBS or UMBS, has run with only a few minor hitches so far. TBA trading in UMBS started on March 12 for settlement starting June 3, exchange of Freddie Mac PCs for UMBS began May 7, and compensation for the exchange has run smoothly. Despite a few software bugs, a wrinkle in exchanging May’s pools and a slight premium for Fannie Mae TBA pools, the market seems ready for the transition to UMBS to go fully live on June 3.

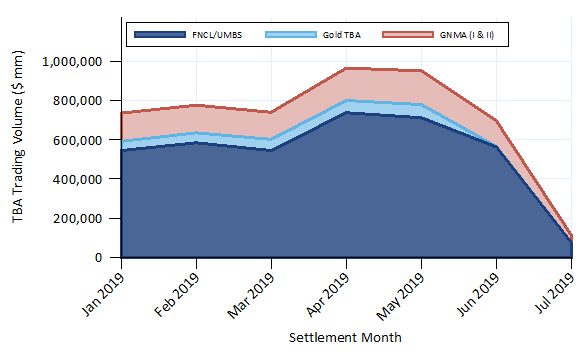

Fannie TBA trading volume carries on in UMBS, while Gold TBA virtually stops

Conventional TBA trading hasn’t slowed with the advent of UMBS (Exhibit 1). Gold TBA trading typically was 10% of total conventional volume in 2019 but has fallen to virtually nothing in the months with UMBS TBA trading, since those pools can be exchanged and delivered into the UMBS contract.

Exhibit 1: TBA 30-year trading volumes (net of dollar rolls) by settlement month

Source: FINRA TRACE, Amherst Pierpont Securities

UMBS does not appear to have hurt conventional TBA trading. UMBS TBA trading for June settle has already reached levels comparable with combined Fannie and Gold TBA trading from January through March.

Another way to show that UMBS hasn’t hurt conventional TBA trading is to compare conventional to Ginnie Mae volumes. For example, Ginnie Mae TBA trading averaged 18.7% of total TBA trading in 2019, and is 18.7% of TBA volume in June.

Exchange volume has been strong

On June 3 Freddie Mac will no longer issue new 45-day delay Gold pools—with the exception of Giants— taking the final step towards creating a security that is fungible with those issued by Fannie Mae. All new Freddie Mac fixed rate pools will carry a 55-day delay, while ARM pools will continue to use a 75-day delay.

However a major step was already taken on May 7, when the process to exchange legacy Gold pools for 55-day delay pools went live. Since pool exchanges could settle in May market participants had to be ready operationally, and 55-day delay pools are already circulating in the market. The pool an investor receives is known as a “mirror security” and is backed by the exact same loans as the original 45-day delay pool.

Roughly $71 billion of pools have been exchanged so far, which is roughly 5% of the outstanding balance of Gold pools. A portion of those pools are locked up in CMOs and cannot be exchanged, which means that roughly 6% of the available float has already been exchanged. The first exchanges settled on May 17 and there have been seven settlement days in all, so on average nearly 1% of the float has been exchanged each day. The next available settlement date is currently June 10—there is a blackout period from June 3 to June 7, when factors are released.

Importantly, there were no surprises regarding float compensation

A major concern of investors was that the compensation received for lost float when exchanging pools would be correct, and by all accounts it has been. Freddie Mac was very careful to create a transparent process for valuing the lost float and communicating the amount to the market directly and through Bloomberg. Yet until the exchange process was available there was the risk that an operational problem could affect the payment—the amount received timing, and so on.. So far those fears have proven unfounded.

Bloomberg’s trading system cannot yet process exchanged pools

On May 3 Bloomberg changed its ticker syntax for Freddie Mac 55-day delay pools and created a problem with Bloomberg’s trading system. The company had planned to use an “FN” prefix for any TBA-deliverable (UMBS) pool, and the “FR” prefix for all other 55-day delay Freddie Mac MBS. Now Bloomberg intends to use “FR” for all Freddie Mac 55-day pools regardless of TBA eligibility.

However, the change caused an issue with Bloomberg’s TOMS trading system, which became unable to process mirror pools. Trades of these pools must be manually booked and manually reported to TRACE. Bloomberg intends to release a fix on June 6. So while this is an operational burden it did not threaten to delay the single security go-live date.

One software platform did not immediately support exchanged pools

Another issue came up while testing the back office platform IMPACT, preventing it from processing changes for the first 7 days. The problem was resolved in a fix on May 14. This platform is very widely used and many customers chose to wait for the fix before exchanging pools. This contributed to very low volumes during the first week the exchange was open.

Some May Gold pools couldn’t be exchanged immediately

May is the only month during which Freddie Mac issued new Gold PCs while investors had access to the exchange process. This created some operational issues with exchanging May issue pools. The largest effect was on the multi-lender pools, which don’t settle until close to the end of the month, and therefore couldn’t be exchanged before May 30. Single-issuer pools settling from May 13 through May 28 were eligible for exchange four days after settlement, pools settling on May 29 and 30 were exchange eligible one day after settlement, and pools settling on May 31 are not eligible for exchange until the 5th business day (June 7).

A similar issue arose when creating supers, which were not permitted to settle until the fifth business day of June.

The Gold/Fannie swap no longer trades

Since the exchange process allows any TBA-eligible Gold pool to be exchange for its equivalent UMBS pool there is no longer any point in trading the Gold/Fannie swap. Investors can exchange the pool as needed or when they feel the float compensation is rich. Therefore the swap is no longer trading.

Some Fannie UMBS is trading at a payup

Some investors remain concerned that Freddie UMBS will prepay worse than Fannie UMBS. For example, the servicer mix in Freddie multi-lender pools is perceived as being worse than in Fannie pools, so the latter pools are currently trading at a slight payup.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.