Uncategorized

The basis and balance sheet normalization

admin | March 15, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

The Fed’s eventual unfurling of more detailed guidance on its balance sheet normalization, possibly as soon as March 20th, will likely include plans to hold its portfolio balance steady in part by reinvesting MBS principal back into Treasury debt. Although bad on the margin for portfolios overweight MBS against rates, the Fed is not the only net supplier of Treasury debt these days. The federal government is likely to issue $1 trillion or more in net new debt this year and in 2020 and 2021 and for years after that. All else equal, the flood of Treasury debt should bias all spreads tighter.

Primary dealers estimated in January that privately held net Treasury debt would rise by $1.345 trillion this year with only $286 billion coming from the Fed’s portfolio. If the Fed announces it will begin reinvesting both maturing Treasury principal and amortizing and prepaid MBS principal back into Treasury debt, the reinvestment will reduce net private supply. The absolute impact will depend on timing and the pace of MBS prepayments. Fed Treasury balances have been falling by an average of $24 billion a month and MBS by more than $16 billion. The later the Fed starts, the less impact it has.

There is a large global audience of buyers for Treasury debt, and that audience grows in proportion to US trade deficits, which the Congressional Budget Office projects at $1 trillion annually through 2021. Some of the dollars spent to import goods and services will stay outside the US and get reinvested in Treasuries. But that demand still may not be enough to absorb net private supply.

Net new supply of MBS has been running lately at an annual rate of $240 billion and, based on spreads, has been readily absorbed. A flat yield curve and low realized and implied volatility has helped build a strong bid for carry this year. MBS along with other spread products has seen good demand. The Fannie Mae 30-year par coupon yield started the year 90 bp wide of the 7.5-year Treasury curve and is now only 83 bp wide.

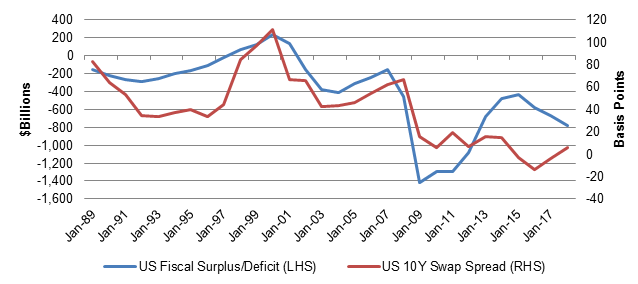

US deficit spending and the occasional surplus have long had an influence on fixed income spreads. When the US last reported fiscal surplus in the late 1990s and early 2000s, the resulting shortage of Treasury debt left many spreads at historic wides. Spreads on 10-year interest rate swaps, for instance, reached more than 120 bp (Exhibit 1). When recession hit in 2001 and deficit spending returned, the rising supply of Treasury debt led to tighter spreads. And since deficit spending soared to record levels in the years after the 2008 financial crisis, spreads tightened to historic levels, too. With deficits projected to exceed $1 trillion annually through 2021 and for years afterwards, spreads should steadily tighten. The Fed’s balance normalization is unlikely to stand in the way.

Exhibit 1: As US deficit spending goes, so go US fixed income spreads

Source: Federal Reserve, Bloomberg

* * *

The view in rates

The 2.58% rate on 10-year Treasury notes looks clearly rich to fundamental fair value, but it has been tracking a steady decline in rates globally. The ECB’s recent announcement of a third TLTRO, its extended guidance and its revision of inflation expectations through 2021 suggest significant weakness in Europe. Recent Fed remarks also have highlighted downside risk to growth. The 2.44% rate on 2-year notes has also started to build in slightly better odds of a Fed cut in the next two years, another signal of growth concerns. And breakeven 10-year inflation continues to hover less than 10 bp below the Fed’s 2.0% target, suggesting that most of the drop in rates has come from revised growth expectations.

The view in spreads

With the yield curve flat, rates steady, and those conditions likely to persist, carry has caught a bid. MBS could widen a little this year if new bank liquidity rules reduce bank demand for MBS. Healthy MBS net supply could also weigh on spreads. But low volatility argues for MBS, as does heavy Treasury supply. MBS should still outperform corporate credit especially as slowing growth raises concern about leveraged corporate balance sheets. Portfolios buying corporate debt should focus on names that show organic growth or use free cash flow or asset sales to pay down debt.

The view in credit fundamentals

Household balance sheets look strong, and corporate balance sheets look vulnerable. The ratio of household debt service to disposable income is at a record low, corporate leverage at a relative high. Of course, this all can continue for a long time if growth persists. The Fed has signaled that it stands ready to buffer any material softening in growth. Still, corporations may need to trim equity buybacks and reduce debt.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.