Uncategorized

New leadership, new direction at the FHFA

admin | January 31, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

With Joseph Otting now in place as acting director of the Federal Housing Finance Agency and with Mark Calabria nominated and likely to get the nod as director, the thoughts of the housing finance community have turned to the ways the new chief regulator might change the direction of Fannie Mae and Freddie Mac. Many are concerned that the GSEs will veer off on a dramatically different path with predictions ranging from full restoration of their pre-2008 status to shrinkage to a mere fraction of their current selves. While the angst is understandable, neither extreme is likely. Some shrinkage, however, looks very likely. The more interesting question is ‘how?’

The players

Mel Watt finished his 5-year term on January 6, and President Trump moved quickly. He tapped Joseph Otting, the Comptroller of the Currency as the acting head, and Mark Calabria, Vice President Michael Pence’s Chief Economist, as the permanent head. Otting assumed the office when Watt departed and will hold both the OCC and FHFA job until Congress approves the nomination of Mark Calabria. Holding both the top OCC and FHFA jobs is easier than most two-job combinations as they are in the same building in DC.

Otting, in particular, is unlikely to veer dramatically off the current course. For one, he is dedicated to continuity in the most important policy issue on the near horizon, the Single Security, which is to be launched on June 3, 2019. In order to launch on time, TBA trading needs to begin in March or April. Before TBA trading can begin, the Securities Industry Financial Markets Association, or SIFMA, must approve trading in the so-called Uniform Mortgage-Backed Security. SIFMA has made it clear that they are concerned about changes in policies at Fannie and Freddie that could produce different prepayment speeds and need to see the FHFA specify the remedies that it will take to assure alignment of GSE policies before they can consider approval. By inviting Bob Ryan, the FHFA senior executive who has been the most involved with the launch of the Single Security, to stay as Special Advisor, Otting has made it clear the Single Security is a priority. A conference on the topic hosted by Fannie Mae and Freddie Mae is scheduled for March 4 in New York, another signal that Otting wants things to move ahead on schedule.

Calabria is likely to take over as the confirmed director in the spring or summer this year. As the former senior aide on the Senate Banking Committee and a generally collegial guy, it is hard to imagine that he would fall short of the 51 votes needed for Senate confirmation as it would mean that four Republicans had abandoned him.

As a libertarian, Calabria has long maintained that the government should drastically reduce its role in the housing finance system. And while as a regulator he will likely moderate his position, the change is likely to be one of degree not of direction. So we should expect him to take steps to shrink their footprint.

Shrinking the GSE footprint

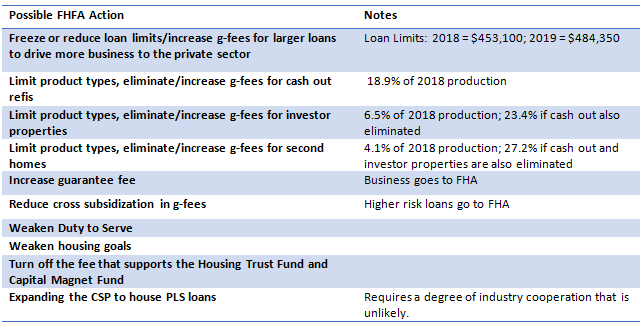

Calabria can choose from a menu of options to shrink the footprint of the GSEs. The possibilities range from changing loan limits, raising guarantee fees and trimming the list of loans covered to changing policy mandates, cutting the affordable housing commitment and opening GSE infrastructure to private securitization (Exhibit 1). Some are more plausible than others.

Exhibit 1: FHFA can choose from a menu of options to shrink the GSE footprint

Source: Author synthesis from various articles and press reports; author calculations from eMBS data.

Restricting loan balances

Given the role of the FHFA as conservator under the Housing and Economic Recovery Act of 2008, or HERA, Calabria can change the loan limits, now $484,350 in most of the nation and up to 50% higher in high cost areas. He was a senior aide on the Senate Banking Committee from 2006 to 2008, and drafting HERA was one of his crowning achievements. An alternative would be to simply raise guarantee fees on all loans over some limit, and let the private market capture these loans. This preserves the government backstop in case the private market cannot step up fast enough and allows for experimentation as to what the “right” g-fee is to accomplish this. It thus seems the more sensible of the two approaches.

Tightening loan eligibility

The second set of actions would be to reduce the range of products covered by the GSEs. For example, Calabria could eliminate or raise guarantee fees on cash-out refinancings. This is a very large category, covering 18% of 2018 production. He could also make investor properties ineligible or increase the g-fees on these loans. It is important to note that investor properties already face high LLPAs, and many of these loans are already going into non-agency securitizations. Investor properties were 6.5% of 2018 production. Some of investor properties were also cash out refinances, however, so eliminating these categories completely would eliminate 23.4% of 2018 production. Finally, Calabria could make second homes ineligible or price to drive more of these loans to the private market. These loans constituted 4.1% of 2018 production. If the new director eliminated cash-out refinances, investor properties and second homes, it would have cut 27.2% of 2018 production. Chances are good these categories will be curtailed through higher g-fees but not completely eliminated. And remember, eliminating cash-out refis would send many of these loans to FHA, with its full faith and credit guarantee.

Restructuring g-fees

What about raising the overall level of g-fees and eliminating the cross subsidization within the GSE space? That is, the FHFA believes that very pristine borrowers pay more than their risk would indicate, while more risky borrowers pay less. The latest FHFA Report to Congress makes this clear. While one could quibble with the math in this analysis—it does not consider g-fees paid (risky borrowers pay more), and it does not consider the fact that more pristine collateral has higher prepayment costs, as these loans are more negatively convex—let’s assume the FHFA is convinced that there is a large amount of cross-subsidization. The issue is that if FHFA tries to eliminate the cross subsidization, by raising g-fees to riskier borrowers, they drive most of the risky business to the FHA. It is hard to think that a libertarian would be proud of having driven the GSE share down, while simultaneously increasing the FHA share.

Loosening affordable housing mandates

Other actions the Calabria led FHFA could take include reducing the duty to serve mandate, starving the Housing Trust Fund and the Capital Magnet Fund, and being less aggressive about housing goals. Duty to Serve Mandate directs the GSEs to provide mortgage financing by developing new products and through more flexible underwriting to three specific underserved markets: manufactured housing, affordable housing preservation and rural markets. The GSEs are required to set aside 4.2 bp of the dollar amount of new business, as long as it would not interfere with the financial stability of the enterprises or hinder a capital restoration plan, to be divided 65% to the Housing Trust Fund, an affordable housing production program that attempts to increase and preserve housing supply for very low income, and extremely low income families, and 35% to the Capital Magnet Fund, a fund that provides grants to community development financial institutions and other non-profits, through a competition, to financial affordable housing, economic development activities and community service facilities. The FHFA is also required to set annual housing goals for Fannie Mae and Freddie Mac.

It is hard to predict what would happen to these tools. While required by statute, the FHFA has some flexibility with each of these mandates. When he was director, Ed DeMarco suspended payments to the funds and delayed the implementation of the duty to serve, and it would be easy for Calabria to change the metrics by which either the duty to serve or the goals are judged, reducing their impact. While philosophically Calabria has expressed skepticism for the efficacy of these tools, reducing them significantly would be very controversial with the advocate community. Expect any action on these to be slow and incremental.

Broadening the Coverage of the CSP

There has also been discussion among industry participants that the Common Securitization Platform could be extended to private-label securities. To realize significant advantages, this extension would require the private market to adapt standard documentation and practices. Despite the best efforts of the Structure Finance Industry Group, which has attempted to standardize the documentation and best practices through the RMBS 3.0 Green Papers, there is little industry standardization. It is hard to see the level of industry cooperation that would make this happen.

Other Thoughts

Don’t expect a large expansion of the non-QM market in 2019 as a result of Calabria’s confirmation; the timing does not allow for it. If things go smoothly, he will be is confirmed in the April to June timeframe. Let’s assume the items mentioned above were the top of his list. He would begin to study the issue, and it is unlikely he would issue any sort of directive to increase g-fees or cut products before August or September. FHFA usually gives the market 3 month notice on changes, so it would be November or December before changes are enacted.

Do expect the GSEs to continue to lay off the bulk of their risk through credit risk transfer. These hugely successful programs have allowed the GSEs to transfer most of the credit risk on new mortgage origination from the taxpayer to private capital. These programs are likely to grow further.

Finally, be wary of claims that he will bring the GSEs out of conservatorship. Calabria, as one of the designers of HERA, gave the FHFA the power to put the GSEs into receivership, and has since suggested that this would be his preferred way out. But he would be unlikely to do this without the design of a viable housing finance system in place; particularly given the challenges to maintaining government support after receivership. The Urban Institute has reported on these issues extensively. Moreover, Calabria is deeply skeptical of actions that privatize the gains and socialize the losses, which would be precisely what such a path would amount to if the GSEs were to emerge from conservatorship then receivership with a government guarantee. Look for a lot of noise but no real action on this front.

Laurie Goodman is a consultant to Amherst Pierpont Securities. She is also a co-Director of the Housing Finance Policy Center at the Urban Institute in Washington DC; all views expressed in this article are her own.