Uncategorized

LIBOR transition divides legacy and new securitizations

admin | January 11, 2019

This material is a Marketing Communication and does not constitute Independent Investment Research.

Loan, bond and securitization contracts issued before problems with LIBOR escalated in 2013 often did not anticipate a scenario where the benchmark rate ceased to exist or provide for a smooth transition to a new floating-rate index. If LIBOR is unavailable on a reset date, the legacy contracts typically fix LIBOR at the previous setting based on the unstated presumption that the disruption in LIBOR is temporary. This could effectively recast legacy LIBOR floating-rate loans and securities into fixed-rate ones, introducing significant risks. ARRC has drafted more robust fallback language for new contracts, which includes provisions for transition to a new benchmark, but due to the many uncertainties surrounding the eventual structure of the SOFR curve and its comparability to LIBOR, it’s possible that the new fallback language will not be completely market-neutral either.

Problematic LIBOR fallback language in legacy securitizations

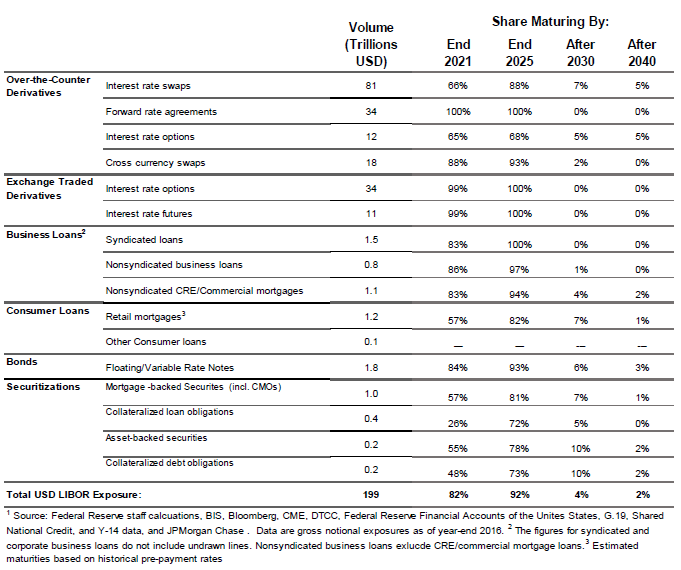

The boilerplate language in a lot of bond, loan, and securitization contracts never envisioned an outright cessation of LIBOR or a transfer to a new benchmark interest rate. The fallback provisions in the contracts were often written to accommodate a temporary market disruption where LIBOR was unavailable for a short period of time. The amount of LIBOR exposure across asset classes that will still be outstanding after 2021 is shown in Exhibit 1, the table is borrowed from an ARRC presentation:

Exhibit 1: Estimated USD LIBOR market footprint by asset class

An example of this kind of language comes from a prospectus for student loan asset-backed notes which were securitized in 2008 as part of the SLC Student Loan Trust 2008-1. The securities are composed of five tranches of floating rate notes indexed to 3-month LIBOR plus various spreads. Two of the tranches have final maturity dates in 2032 and 2038 respectively, 10 and 16 years after LIBOR will likely cease publication. There is additional basis risk in the securitization as the underlying assets are student loans with rates that float off of 3-month Treasury bills or 3-month commercial paper rates, not LIBOR.

If LIBOR is not reported or is unavailable on an interest rate determination date, the securitization uses the following rules (page S-34 of the prospectus, formatting and emphasis added):

Determination of LIBOR

LIBOR, for any accrual period, will be the London interbank offered rate for deposits in U.S. Dollars having the specified maturity commencing on the first day of the accrual period, as that rate appears on the Reuters LIBOR01 Page, or another page of this or any other financial reporting service in general use in the financial services industry, as of 11:00 a.m., London time, on the related LIBOR Determination Date.

If no rate is so reported on the related LIBOR Determination Date, the rate for that day will be determined on the basis of the rates at which deposits in U.S. Dollars, having the specified maturity and in a principal amount of not less than $1,000,000, are offered at approximately 11:00 a.m., London time, on that LIBOR Determination Date, to prime banks in the London interbank market by the Reference Banks. The administrator will request the principal London office of each Reference Bank to provide a quotation of its rate. If the Reference Banks provide at least two quotations, the rate for that day will be the arithmetic mean of the quotations. If the Reference Banks provide fewer than two quotations, the rate for that day will be the arithmetic mean of the rates quoted by major banks in New York City, selected by the administrator, at approximately 11:00 a.m., New York time, on that LIBOR Determination Date, for loans in U.S. Dollars to leading European banks having the specified maturity and in a principal amount of not less than $1,000,000.

If the banks selected as described above are not providing quotations, LIBOR in effect for the applicable accrual period will be LIBOR for the specified maturity in effect for the previous accrual period.

Based on the above language, in the event that LIBOR ceases to be reported, the still outstanding floating rate securities will effectively become fixed rate securities, with the interest rate fixed on the last “live” LIBOR determination date for the remaining maturity of the bond. In such a scenario the LIBOR levels prevailing over the latter half of 2021 will “freeze” the interest rates for the life of the securities.

Whether freezing the interest rate generates a gain or loss obviously depends on both the particular securities and the yield curve. If the security has only six months to maturity, for instance, and the yield curve slopes upward, then the security might take a small mark-to-market loss. If the security has 10 years to maturity, however, and the yield curve slopes upward, the mark-to-market loss could be substantial. If the yield curve is inverted, in contrast, the securities could take mark-to-market gains.

There is basis risk in securitizations, too. In the student loan securitization example, the underlying assets are not tied to LIBOR but float off of Treasury and commercial paper indices. Securitization of option ARMs before 2008 also often involved issuing LIBOR-indexed securities backed by loans floating off of a constant maturity Treasury index. The securitizations typically make payment of the security coupon subject to funds available from the loans. If LIBOR became fixed and the Treasury-index fell, the trust may not have enough funds to pay the security coupon. The basis risk is therefore borne by the securitization trust and potentially the investor. In other securitized products, the loans are tied to LIBOR as well. Depending on the fallback language in the contract and the prevailing interest rates at the time of LIBOR cessation, one party may have a contractual right to a gain, while the other absorbs a loss. Of course, many securitizations also include provisions to amend the documents with the consent of investors, although terms of consent can vary widely.

The larger investment, legal and management consultant community has noticed the issue. The following is excerpted from Changing the World’s Most Important Number – LIBOR Transition by management consultant firm Oliver Wyman:

LIBOR may become unavailable even though products referencing it remain in force. These contracts typically include “fall-back provisions” which specify contract terms in case LIBOR is unavailable. If the period of unavailability is brief, as envisaged when the contracts were drafted, the resulting losses and gains are manageable. But if fall-back terms are used for the remaining life of the contract, the economic impact is likely to be significant, with one side a winner and the other a loser.

Renegotiating a large volume of contracts would be difficult, especially when one party has a contractual right to a windfall gain. If contracts are left to convert to fall-back provisions if LIBOR becomes unavailable, a vast number of price changes would occur in a short period. The associated financial, customer and operational impacts would be difficult to manage.

The Oliver Wyman language implies that the economic impact of LIBOR cessation is a zero-sum game, although reality is likely to be much more subtle. As 2021 approaches, the mix of fallback language, security characteristics and prevailing interest rates could stir up a whirl of repositioning activity.

LIBOR transition plans and fallback language for new securitizations

New securitizations issued over the next three years – prior to the transition from LIBOR to SOFR currently planned for year-end 2021 – should benefit from specific and uniform contract language that will govern the fallback from one reference rate to another. The Alternative Reference Rates Committee (ARRC) and the Structured Finance Industry Group (SFIG) released consultations for the fallback contract language for new LIBOR securitizations in December 2018. The proposals seek comments and feedback no later than February 5, 2019. ARRC is expected to issue final contract language for market participant’s voluntary use in future LIBOR contracts sometime after the 60-day comment period closes.

The draft LIBOR fallback language for new securitizations contains the following provisions:

- A list of trigger events that will result in a transition from LIBOR to the new replacement rate, presumably SOFR;

- A replacement benchmark waterfall, specifying what the replacement rate will be, whether it is overnight SOFR, term SOFR, a futures-based SOFR (neither of which exist yet but hopefully will by the time the transition takes place) or a compounded SOFR set “in arrears” or “in advance” still to be determined; and,

- A replacement benchmark spread waterfall, specifying how the benchmark rate should be adjusted to account for the term and bank credit risk in LIBOR compared to the risk-free, secured, overnight SOFR rate. The spread adjustment has yet to be defined but presumably will be by ARRC by the time the proposed contract language is finalized.

Perhaps the most consequential proposal in the consultation is that there is a proposed trigger that if more than 50% of the assets by principal balance underlying a securitization move to a new reference rate, this would trigger the securities to move to the new reference rate as well. This potentially addresses the asset-liability mismatch if LIBOR-based loans and securities don’t convert to the new reference rate at the same time. This would potentially eliminate some of the basis risk in new securitizations due to the transition. Legacy contracts could be amended to include the language, but existing investors or borrowers who potentially faced a profit if their floating rate loans convert to fixed, would be unlikely to agree to the amendment unless they were fairly compensated.

Background on transition plans

There have been several recent updates and developments regarding proposed transition plans from LIBOR to SOFR, specifically regarding how the transition should be effected for new issuances of LIBOR-based securitizations.

ARRC Consultation on Fallback Contract Language for New Issuances of LIBOR Securitizations was released on December 7, 2018.

LIBOR Task Force Green Paper, with recommended best practices for LIBOR benchmark transition of new-issue securitizations was published by the Structured Finance Industry Group (SFIG) on December 14, 2018.

The SFIG is involved in the Alternative Reference Rates Committee (ARRC) and is co-chair of ARRC’s Securitizations Working Group, which published its own consultation on December 7, 2018. SFIG’s LIBOR Task Force published the green paper to specifically reflect the views of their membership. The LIBOR Task Force seeks to establish industry consensus and provide recommendations around one or multiple accepted approaches.

The consultations by ARRC, the Securitizations Working Group of ARRC, and the SFIG LIBOR Task Force appear to be fundamentally the same. To the extent that there are any material discrepancies or strong preferences for different methods among the various groups, these will be pointed out as they emerge. So far the proposals are virtually identical, so we recap the proposed fallback language for new securitizations from ARRCs consultation.

Notes from ARRC consultation

The following notes are taken nearly verbatim from the slides prepared by ARRC. Editors remarks are noted as such.

Libor Fallback Language for New Securitizations

- Triggers: What events would result in a transition from LIBOR to the new replacement rate?

- Replacement Benchmark Waterfall: What should the new replacement rate be? SOFR is the preferred rate but there isn’t a term structure for it yet.

- Replacement Benchmark Spread Waterfall: How should the rates be adjusted to account for the differences between LIBOR and SOFR? LIBOR has both a term and bank credit risk component while SOFR is a secured, risk-free overnight rate. What should the additional spread be to compensate for these differences?

Triggers

Consultation proposes six triggers that would signal conversion from LIBOR to a new reference rate.

The first two triggers match ISDA’s triggers for derivatives.

- A public statement or information on behalf of the administrator of the Benchmark announcing that the administrator has ceased or will cease to provide the Benchmark permanently or indefinitely, provided that there is no successor administrator that will continue to provide the Benchmark.

- A public statement or information by the regulatory supervisor for the administrator of the Benchmark, the central bank for the currency of the Benchmark, an insolvency official with jurisdiction over the administrator for the Benchmark, … which states that the administrator of the Benchmark has ceased or will cease to provide the Benchmark permanently or indefinitely, provided that there is no successor administrator that will continue to provide the Benchmark.

Critical note: ISDA triggers assume a permanent cessation of LIBOR and will require the market to move to the new replacement rate once LIBOR has ceased.

Editor’s note: Trigger 2 seems to allow the Federal Reserve, as the central bank for US dollar currency, and the Bank of England and FCA as the regulatory supervisors of ICE as the benchmark administrator, to require that ICE cease publication of LIBOR. While the FCA likely has the legal authority to do so, it is unclear that the Federal Reserve could or would execute such authority unilaterally. Such actions could potentially require resolution by the courts.

The remaining four triggers contemplate a transition to a new reference rate in the absence of permanent cessation of LIBOR and are referred to as “pre-cessation” triggers.

Trigger Signals the Unannounced Stop to LIBOR. A Benchmark rate is not published by the administrator for five consecutive business days and such failure is not the result of a temporary moratorium, embargo or disruption.

4. Trigger Signals a Change in the Quality of LIBOR. A public statement or publication of information by the administrator of such Benchmark that it has invoked or will invoke, permanently or indefinitely, its insufficient submissions policy.

5. Trigger Reflects Regulator View that LIBOR is No Longer Representative. A public statement by the regulatory supervisor for the administrator of the Benchmark (or another regulator or Government Authority with jurisdiction over the Designated Transaction Representative) announcing that such Benchmark is no longer representative or may no longer be used.

6. The Asset Replacement Percentage is greater than 50%, as reported in the most recent servicer report.

Trigger 6 addresses the mismatch that could occur if LIBOR-based assets and liabilities do not convert to the same replacement rate at the same time.

Editor’s notes: The pre-cessation triggers clearly provide a path for regulators to advance the date of the transition to SOFR. Trigger 5 ostensibly allows the FCA, as the regulator of ICE, to declare that LIBOR is not representative and force the transition. Again this could introduce jurisdictional and regulatory issues between UK and US law, and it seems unlikely that such an action would be taken, but clearly the threat of action might provide encouragement enough for counterparties to the financial contracts to adopt fallback language and execute the transition to SOFR.

The Asset Replacement Percentage measures, by principal balance, the percentage of underlying assets that have moved to the new replacement rate. Therefore if the ARP is greater than 50% (meaning that more than 50% of the underlying assets are now using the new reference rate) this would trigger the securities to move to the new reference rate.

Securitizations Replacement Benchmark Waterfall

- Term SOFR – assuming term SOFR is published at the time of the transition

- Compounded SOFR – overnight SOFR compounded over the term of the contract

- Replacement rate recommended by the Relevant Governmental Body (the ARRC) – assumes SOFR is not available at all, the default to different rate recommended by ARRC

- Replacement rate in then-current ISDA definitions – if ARRC is unavailable use rate recommended by ISDA

- Replacement rate proposed by the Designated Transaction Representative – if the financial world has descended into chaos, put on a helmet (editor’s commentary).

Securitizations Replacement Benchmark Spread Waterfall

- Spread recommended by Relevant Governmental Body (ARRC)

- Spread in fallbacks for derivatives in ISDA Definitions

Editors note: The spread waterfall is perhaps the most problematic, as it could immediately introduce a market value discrepancy that would require compensation.

ICE studies zombie LIBOR

On December 4, 2018 ICE Benchmark Administration announced a survey to seek support from globally active banks for publishing LIBOR after year-end 2021 for users with outstanding LIBOR-linked contracts that are impossible or impractical to modify. An excerpt from the announcement (emphasis added):

The purpose of the survey is to identify the LIBOR settings that are most widely used. IBA will use the results of the survey to inform its work in seeking the support of globally active banks for the publication of certain LIBOR settings after year-end 2021. The primary goal of this work would be to provide those LIBOR settings to users with outstanding LIBOR-linked contracts that are impossible or impractical to modify. Any such settings would need to be compliant with relevant regulations and in particular those regarding representativeness.

It will be interesting to see if ICE can persuade the FCA and global banks to allow them to continue to publish LIBOR after year-end 2021 and for the FCA not to invoke the trigger event by declaring it unrepresentative or insufficient. The outcome may depend on investor comfort with SOFR over time and the success encountered building out a SOFR term structure and futures market.