Uncategorized

Business as usual as markets underprice the Fed

admin | December 14, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

Financial markets historically have underestimated the pace at which the Federal Reserve would ultimately raise rates. This is important again now that markets have been pricing out Fed moves beyond the December meeting. Currently, fed funds futures indicate that the Fed will only tighten once after December 19, at which point the current rate cycle will be over. In contrast, the FOMC’s September median dot projections call for three rate hikes next year and one more in 2020. While the dots may come down a little on Wednesday, there will almost certainly remain a substantial gap between policymakers and market expectations. This is nothing new. In recent history, markets have almost always underestimated how much interest rates would rise.

Measuring market expectations for monetary policy

Eurodollar futures signal market expectations for the path of the Fed’s policy rate at various points in time. Fed funds futures would be a better measure, but there is very little trading in distant forward fed funds futures today and there was virtually none decades ago. The more liquid Eurodollar contracts offer a more reliable, though less clean, gauge.

Since Eurodollar futures correspond to 3-month LIBOR rates, I am going to look at the rolling 9th Eurodollar contract implied yield and compare it to the rolling current contract implied yield to get a measure of how much the Fed was expected to move over the next two years just before the initial rate hike in each of the last three rate cycles. Up until the current rate cycle, two years was generally considered enough to capture an entire hiking campaign – I will look further ahead when considering the current episode. Since these are three-month contracts, I will look at a date exactly three months before the first Fed move to assess market expectations before the onset of tightening. If anything, the spread that I am examining probably slightly overstates the expectations of rate hikes since the Eurodollar futures curve includes a modest amount of term premium as you move out the curve.

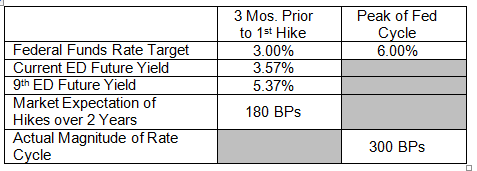

Hiking from 1994-1995

The Federal Reserve took the fed funds rate all the way down to 3% in 1992, a shockingly low rate at the time in the wake of the high-inflation 1970s and 1980s. Moreover, policy remained on hold at that level for well over a year, at the time one of the longest spells of inactivity from the Fed in its history. The first rate increase occurred on February 4, 1994. Market expectations were that the FOMC would push rates up by between 150 bp and 200 bp over the next two years (see Exhibit 1). However, the Federal Reserve ultimately jacked up rates by 300 bp in 12 months, pushing the funds rate to 6%.

Exhibit 1: 1994 rate expectations

Source: Bloomberg

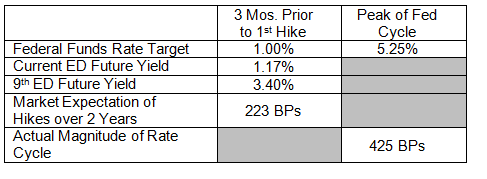

Rate cycle from 2004-2006

In the next easing cycle, in the wake of the 9/11 attacks and a sluggish recovery, the FOMC lowered the funds rate target to 1.00% in 2003 and held it there for a year. Finally, in June 2004, with growth surging and core inflation having accelerated after briefly dipping below the Fed’s implied “comfort zone” in 2003, the FOMC began to raise rates. Just before the rate hikes began, the Eurodollar futures curve suggested that the markets expected the Fed to raise rates by a little more than 200 bp over the next two years. In the end, the FOMC executed 25 bp rate increases at 17 consecutive meetings over exactly two years (see Exhibit 2).

Exhibit 2: 2004 Rate expectations

Source: Bloomberg

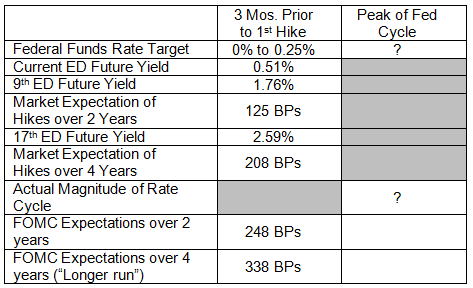

Rate cycle starting in 2015

The Federal Reserve hit the zero bound in 2008 and stayed there for years after the Crisis. In fact, further easing was added via QE from 2010 through 2014. The FOMC finally lifted off from the zero bound in December 2015 after delaying several times (first in tapering QE in 2013 and then in raising rates in 2015). It was commonly understood at that time that the rate hike cycle was likely to last more than two years, so referencing the 9th Eurodollar future is probably insufficient. For this cycle, I would also introduce the rolling 17th Eurodollar future, which can be used as a rough proxy of where markets expected the policy rate to be in four years. The other innovation for the latest rate cycle is that the FOMC’s dot projections are available, so we can compare market expectations with those of policymakers. As Exhibit 3 shows, Eurodollar futures implied about 125 bp of tightening over the two years from the first rate move, about half of what the FOMC itself expected to carry out.

Exhibit 3: 2015 Rate expectations

Source: Bloomberg, Federal Reserve

Of course, we do not know where the funds rate target will peak in this cycle, but we do have some indicators of how market expectations compare to the actual outcome. In this instance, dovish market pricing turned out to be more right than the Fed’s own thinking. Three-month LIBOR ended 2017 at 1.60%, just a few basis points below the market’s projection from late 2015. Moreover, the December 2019 Eurodollar future currently yields 2.93%, only 34 bp higher than the 4-year ahead Eurodollar futures contract projected in late 2015.

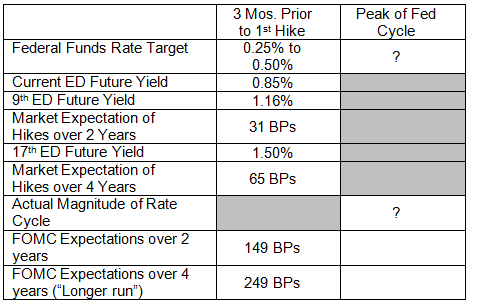

Detour in 2016

Of course, the current rate hike cycle was nearly derailed just after it got off the ground. Financial market volatility in early 2016 short-circuited the FOMC’s intentions (at the end of 2015, the dot projections indicated that the Fed expected to raise rates by 100 bp in 2016). The Committee was firmly on hold for much of the year and finally resumed its rate hike campaign in December 2016. The contrast between market expectations and the actual results when treating the December 2016 rate increase as the start of the cycle (since it, rather than the first one in 2015, turned out to be the beginning of a regular series of moves) looks much more like the two prior episodes. Conditioned on the FOMC’s ultra-dovish behavior in 2016, market expectations proved to have a far-too-dovish outlook (see Exhibit 4).

Exhibit 4: 2016 Rate expectations

Source: Bloomberg, Federal Reserve

As it turns out, both the markets and the Fed were too conservative in late 2016, as, assuming the FOMC hikes on Wednesday, the funds rate target will have risen by 200 bp over the period from September 2016 through the end of 2018. Moreover, the policy rate has already moved well above 1.50%, where Eurodollars futures in late 2016 were priced for the end of 2020. The December 2020 Eurodollar futures contract currently yields 2.84%, nearly double where it was roughly two years ago.

Looking ahead

Thus, the wide gap that currently exists between market pricing of future Fed policy and the FOMC’s own expectations is far from extraordinary. I am not surprised that markets are substantially more dovish than the FOMC (or my own forecasts). Beyond the history laid out above, there are two reasons in my view why market participants have been especially dovish in the current rate cycle (market pricing has trailed the FOMC dots throughout the rate cycle, usually by a wide margin).

First, the Federal Reserve lost a lot of credibility with its behavior earlier this decade. There are several instances where the FOMC appeared to be signaling a move toward normalization and then pulled back due to worries about financial market volatility and/or downside economic risks. Chairman Bernanke spent several months signaling that tapering of QE would be announced in September 2013, but when the markets responded with the Taper Tantrum, the Fed held off (ultimately making the taper announcement three months later in December). Then, in both the summer of 2015 and early 2016, the FOMC delayed rate hikes by at least six months in response to episodes of market volatility. The lesson that market participants learned from these episodes is that the Fed could not be trusted to follow through with tightening moves that they were projecting. The stark downward move in Eurodollar futures from late 2015 (Exhibit 3) to late 2016 (Exhibit 4) shows how substantially market participants adjusted their shifts to the FOMC’s dovishness. It took quarterly rate hikes for basically two years straight for market participants to finally begin to believe that the Fed would do what it said it would, as the gap between the dots and market expectations finally began to close this year. However, to many, the recent upheaval in equity and risk markets smells an awful lot like the Taper Tantrum, the summer of 2015, and the beginning of 2016, so there are renewed concerns that the FOMC will alter its course, as it did several times earlier in the decade. In my view, what market participants may be missing is that the economy is in a very different place today than it was back then, with growth momentum much stronger and labor and product markets much tighter.

This is a good lead-in to the second reason that I believe market participants have been so much more dovish than Fed officials (and most economists) in recent years: market participants, perhaps scarred by the Financial Crisis, have been quite pessimistic regarding the economy throughout this expansion. As noted above, while that skepticism largely served traders and investors well in the early years of the decade, it may be misplaced going forward, as economic growth has been much stronger over the past two years than it was before. I also suspect that global economic concerns may be exaggerated in the minds of many market participants because the transmission from foreign turmoil in financial markets to U.S. asset prices has been far more potent than the transmission of global economic weakness to the U.S. economy, which is far more domestically-oriented than that of our major trading partners. Market participants have also taken a dim view of the inflation outlook. After accounting for liquidity premia, etc., TIPS breakevens have run well below policymakers’, economists’, consumers’, and businesses’ inflation expectations for several years. In sum, market participants are dovish regarding the Fed outlook in part because they see a recession as a realistic possibility for 2019, whereas the FOMC and most economists expect a deceleration in activity next year but to still well-above-trend real GDP growth.