Uncategorized

The demise of the auto sector has been greatly exaggerated

admin | December 7, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

Financial market participants have become increasingly concerned that the U.S. economy is quickly losing steam and that the Fed will soon have to wrap up its current rate hike cycle. One key element of this narrative has been that the interest rate sensitive sectors of the economy – autos and housing – are weakening. That statement is only half right. Without doubt, housing demand has softened after several years of unsustainably rapid home price increases and recently rising mortgage rates. In contrast, demand for motor vehicles has been strong in recent months and appears unaffected by Fed rate hikes.

Broad View

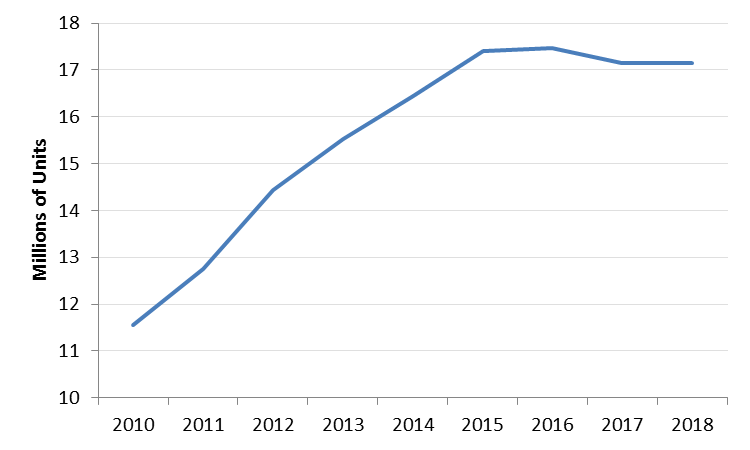

Unit auto sales made a steady recovery from the steep downturn during the 2008-09 recession. In fact, motor vehicle sales may have peaked for the cycle a few years ago, reaching 17.4 million units in 2015 and almost 17.5 million in 2016 (Exhibit 1). Sales slipped modestly in 2017, likely a result of the reining in of what had come to be arguably profligate auto lending to subprime borrowers, though the annual figure of just over 17 million remained quite robust. Despite all of the discussion of weakening in the auto sector, the sales pace in the first 11 months of 2018 is virtually the same as the 2017 performance. Thus, from a broad view, auto sales look quite steady in recent years.

Exhibit 1: Annual unit auto sales

Source: BEA

Focusing on Recent Months

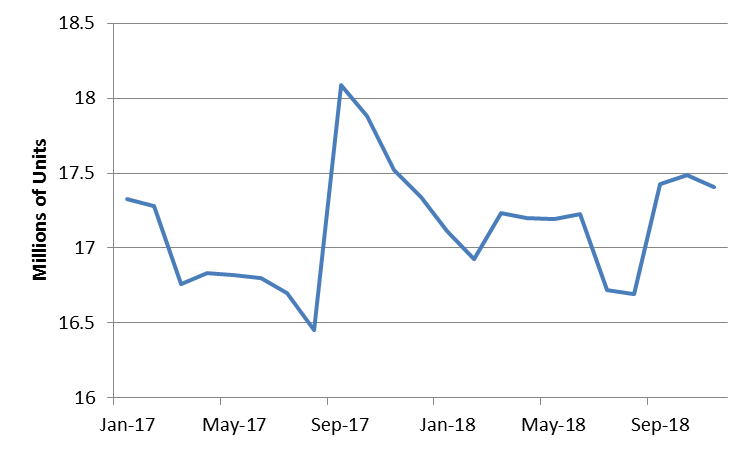

The case for a downturn in auto sales as a key piece of a softening in the overall U.S. economy is even weaker when we focus more closely on the performance of sales in recent months. Unit sales have registered an annualized pace of 17.4 million or 17.5 million in each of the past three months (September, October, and November), the three best monthly sales figures of the year. In fact, aside from the spike in sales in September, October, and November of last year, reflecting heavy replacement of vehicles ruined by Hurricane Harvey, the last three monthly readings for unit auto sales were the top three in nearly two years (Exhibit 2).

Exhibit 2: Monthly unit auto sales

Source: BEA

Thus, the popular narrative that the interest-sensitive auto sector is faltering fails to match reality. In fact, the reverse appears to be true. Motor vehicle sales have picked up steam in recent months, consistent with the overall performance of the consumer: real consumer spending rose at better than a 3½% annualized clip in each of the past two quarters and is on track to advance at close to that pace again Q4.

Postscript: GM Plant Closings

Over the past few weeks, a key piece of the “auto sector is weakening” narrative has been the announcement in late November by GM that it would be closing several assembly and parts plants. This development has been interpreted by most as evidence of a souring outlook for the motor vehicle industry. However, the GM announcement reflects two key longer-term factors that have little to do with the current health of the overall motor vehicle sector. First, U.S. households increasingly prefer trucks and SUVs to sedans. This trend has been intensifying in recent years, helped along not only by shifting customer preferences but also by more moderate gasoline prices. Truck demand wavered over the last 10-15 years whenever gasoline prices surged toward $4/gallon, but prices at the pump have not even hit $3/gallon in over three years. GM is not necessarily going to be producing substantially fewer vehicles overall in the wake of these plant closures, since all of the plants being shuttered are focused on car models that are being discontinued. Expectations are that GM will produce fewer cars — and presumably more light trucks and SUVs. Second, this decision was probably long overdue based on market realities, and the timing was driven in part from regulatory changes. Very stringent fuel efficiency standards during the Obama Administration essentially forced domestic automakers to produce large numbers of fuel-efficient cars so that the average mileage figures for their overall fleet would meet government standards. These were cars that not very many consumers wanted – ending up in rental car fleets instead of end users’ driveways, while others would have to be sold at deep discounts – and cars that the automakers had difficulty producing profitably. When the Trump Administration made its official announcement relaxing future fuel efficiency standards in August, automakers began to shift production toward larger vehicles that customers more highly value. In fact, the “Big Three” automakers, GM, Ford, and Chrysler, appear to be largely surrendering the car market to foreign nameplates, led by the Honda Accord and Toyota Camry. Aside from niche models, US automakers are focusing increasingly on trucks and SUVs, where they believe they have a comparative advantage and can be more profitable per unit produced. Thus, while the GM announcement is certainly an important development in the industry, it does not necessarily have meaningful implications for the broad economic outlook, and it certainly does not prove that Fed rate hikes are gravely harming demand for motor vehicles.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.