Uncategorized

Volatility returns but the long end stays range-bound

admin | November 30, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

A transition away from forward guidance and back to data-driven monetary policy will re-establish the economy and investor risk appetite as primary driving forces in rates. The outlook for rates depends on how soon this transition occurs, and whether wider credit spreads do some of the Fed’s work for them. The overwhelming consensus is for a flat to inverted Treasury curve at a somewhat higher level. Should the Fed pause its hiking early there is a bias for steepening. Liquidity in SOFR futures should improve, particularly if helped along by increased GSE and Treasury issuance of SOFR-linked notes and FHLB advances to banks.

***

The broad consensus is for higher rates, a flatter curve

The overwhelming consensus view in rates among strategists and economists is for modestly higher rates and a flatter to potentially inverted Treasury curve in 2019. The view is predicated on a stable economy – supported by almost $1 trillion in new Treasury supply to fund the estimated federal deficit – and rising inflation allowing the Fed to continue hiking rates until they find neutral. The Fed itself has diagrammed the scenario with the median FOMC dots projecting the target rate at 3.125% for year-end 2019. Fundamentally that outlook appears sound: the Congressional Budget Office expects dissipating fiscal stimulus and growth in private investment will lift GDP to 2.4% in 2019 before slowing markedly in following years. The probability of a recession in the near-term appears low, and attempts to make a case that runaway inflation would spur the Fed to raise rates above 3.50% in 2019 seem downright far-fetched.

An outlier case for fewer hikes, a steeper curve

There is a growing possibility that there may be a pause in hikes in 2019, not because the FOMC acquiesces to cajoling from the Administration, but because a widening in spread products may do some of the Fed’s work for them. The re-pricing of risk – including a calving off of some of the weaker BBB credits into high yield territory – appears likely in continue in 2019. Wider spreads and steeper credit curves tighten financial conditions, pulling neutral closer without raising rates.

As the Fed transitions away from forward guidance and the path of rates again becomes data driven, intra-day volatility in the rates market should pick up, as traders and investors return to sweating out every non-farm payroll print. The consequences of a return to normalcy with the target rate at 2.75% could be a bull steepening of the Treasury curve as the front end re-prices. Volatility would increase on short tenors, but undershooting the dots and possibly the inflation target would likely result in a drop in volatility on longer tenors as the long-end of the curve remained range-bound. In this case expect the 10yT to navigate in the 2.75% – 3.30% range, with no sustained breakout on either side.

Probabilities for the Fed funds target rate: 20% chance the Fed “matches the dots”, and raises the target rate to 3.25% or above by year-end; 60% chance the Fed hikes only once or twice in 2019, increasing the rate to 2.75% or 3.00%; 20% chance the Fed pauses at 2.50% in December and does not tighten in 2019.

The trades: Stay invested in repo and the front end of the rates curve. Extend in duration and enter 2s10s steepeners if growth and inflation remain subdued. Long gamma, short vega.

***

The mandate to build liquidity in SOFR

The official transition from LIBOR to the secured overnight financing rate (SOFR) is scheduled for year-end 2021. At that time the 16 LIBOR panel banks will no longer be required by regulators to submit rates at which they can obtain wholesale funding. Given the substantial civil and criminal penalties imposed on banks, traders and managers across the spectrum of panel banks as a result of the LIBOR-rigging scandal, it is considered highly unlikely that any back will voluntarily remain on the panel beyond that time.

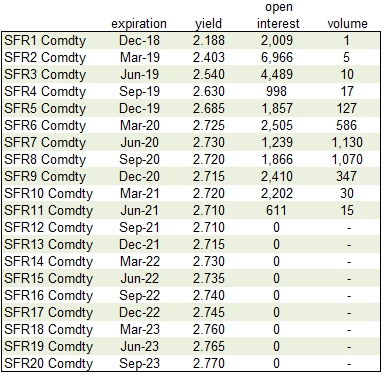

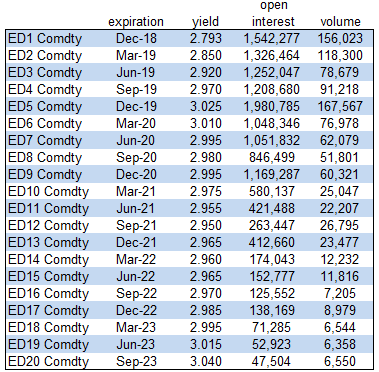

Regulators, investors and issuers have three years to build out the overnight SOFR rate into a deeply liquid term and futures market capable of supplanting LIBOR, Eurodollar futures and swaps. The crucial scaffolding of a SOFR futures market is in place (Exhibit 1), but trading volume remains anemic compared to Eurodollar futures (Exhibit 2). What propels heavy trading in Eurodollar futures is the widespread exposure investors have on both the asset and liability side to LIBOR floating rates and LIBOR-based swaps and other derivatives.

Exhibit 1: SOFR futures (3 month)

Source: Bloomberg

Exhibit 2: Eurodollar futures (3 month)

Source: Bloomberg

The keys to SOFR liquidity: issuance and exposure

The imperative to build a liquid futures market – which will in turn allow the construction of a SOFR term structure and SOFR-based swaps market – is largely dependent on two things:

- How quickly issuers, lenders and structurers transition to SOFR as the underlying floating rate in securities such as floating rate notes, securitized products and interest rate derivatives; and

- How confident investors who hold SOFR-based securities or derivatives feel in their ability to hedge those exposures via the SOFR futures or swaps market.

The challenge for 2019 will be to build broad-based adoption of SOFR as an underlying floating rate by lenders and investors. The Federal Reserve and other regulators can accelerate the adoption process to some extent by encouraging the GSEs – in particular the Federal Home Loan Banks (FHLBs) – to begin denominating new assets and liabilities tied to SOFR instead of LIBOR. The FHLBs are significant issuers of LIBOR-based floating rate notes, which banks and other investors hold as assets; and also extensively lend money to banks via the advance programs, which are often tied to LIBOR and swap rates. Bank and investor exposure to SOFR on both the asset and liability side would encourage interest rate hedging via SOFR futures.

The Treasury Borrowing Advisory Committee (TBAC) has recommended that the Treasury consider issuing SOFR-based floating rate notes. This would also encourage adoption and create additional demand for SOFR futures among those wishing to hedge their risk. Although Treasury has not announced a SOFR-based floating rate note program yet, it is possible that they will do so and that the first Treasury SOFR floaters could be issued in the second half of 2019.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.