Uncategorized

Spreads, dollar rolls and a new sheriff in town

admin | November 30, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

Risk and opportunity in MBS next year is almost certain to turn on a few major influences including the tug-of-war between supply and demand, the potential transition of more than $1 trillion in Freddie Mac PCs into universal MBS and the appointment of a new Federal Housing Finance Agency Director with broad power over things that matter in the markets. Spreads look likely to widen 5 bp to 10 bp to Treasury rates, and wider to swaps. Liquidity in Freddie Mac PCs is likely to come under pressure in the universal MBS transition. And a new FHFA director is likely to look for ways to shrink the enterprise footprint

* * *

Toward wider MBS spreads

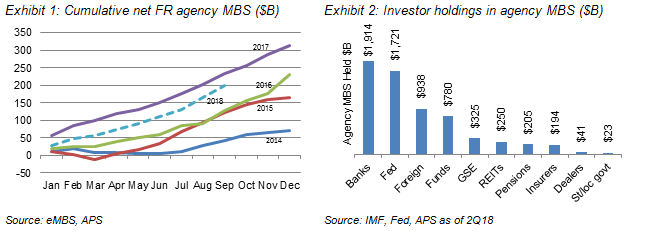

Investors in agency MBS will likely have to navigate conflicting currents next year, but the result should be wider benchmark 30-year spreads by 5 bp to 10 bp. Absent more than $1 trillion in projected net Treasury issuance next year, spreads would go even wider. Growth in outstanding fixed-rate MBS should slow from an estimated $270 billion this year to $215 billion next thanks to a slowing housing market (Exhibit 1), and that should ease some spread pressure. But demand should be uneven (Exhibit 2). Banks, the largest agency MBS investors, should tread water or even allow MBS balances to fall as Fed liquidity rules likely loosen next year (here) and continued economic growth feeds loan demand. The Fed, the second largest investor, almost certainly will let its MBS run off according to script (here). And foreign investors, the third largest group, have shown little MBS appetite in recent years. That leaves the 2019 market in the hands of a few likely strong bidders – total return funds, possibly insurers and almost definitely mortgage REITs. Total return funds have become the strongest marginal bid for MBS this year as an alternative to the rising fundamental risk in investment grade corporate debt. Corporate leverage and slowing economic growth should continue to widen corporate spreads and draw total return capital into MBS. Insurers also started reallocating away from corporate credit this year but have plowed most of the capital into loans. Loan growth should remain insurers’ preferred alternative, but a modest tilt toward MBS could help spreads. Finally, wider spreads to the swap curve should pave the way for a robust bid from mortgage REITs. REITs this year have shown ability to manage rising rates, addressing concerns left over from the 2013 taper tantrum, and equity should be attracted to the REIT yields fueled by a wider basis and manageable leverage. Spread pressure from supply and flat-to-falling MBS balances at banks and the Fed should outweigh the strong bid from total return, insurance and REITs.

Probabilities of widening the par 30-year MBS yield spread to the 7.5-year Treasury: 50% chance of 10 bp or more, 30% chance of 0-10 bp, 20% chance of 0 bp or less.

The trades: Long MBS, short investment grade credit. Long higher coupons in MBS, short lower coupons. Long IO MBS, short pass-throughs.

Agency MBS net supply should fall from 2018, but likely demand looks uneven

* * *

Risks to Freddie Mac dollar roll markets

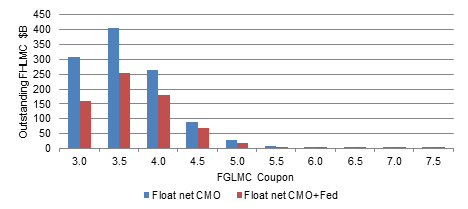

A new universal MBS that blends the Fannie Mae and Freddie Mac TBA markets is scheduled to start trading in June next year, and the stars will have to line up to ensure that it goes off without a hitch for liquidity in Freddie Mac PCs and for the team in the back office. Freddie Mac has done a thorough job of planning and preparing for conversion to UMBS, but trading in Gold PCs could shrink dramatically or grind to a halt over trader concerns about getting caught in a short squeeze. That could happen if investors asked for offerings in securities where market makers suspected a significant flow of intraday conversion and a resulting drop in floating supply. The float in 30-year Gold 4.5% PCs already is low enough to raise that concern (Exhibit 3). The dollar roll market could quickly become impaired, distorting the economics in that market and potentially forcing some investors to take delivery of pools. TBA PC investors would almost be forced to convert to UMBS to regain liquidity. Freddie Mac has said publically that it has significant holdings of Gold PCs in its portfolio, and that the portfolio is there to ensure market liquidity and generate returns for the enterprise. That could be a signal that Freddie Mac would use its holdings to help market makers cover short positions in a squeeze. Just the potential for Freddie Mac to help cover short squeezes could go a long way to allaying market makers’ concerns, but the enterprise has not committed to anything yet. Conversion to UMBS also raises risk for the operational team in the back office. The challenge of clearing and settling mortgage securities already is high, and a tide of conversion clearly ups the ante for getting prices, cash flows, factors and other details right.

Probability that the dollar roll market in Gold PCs shrinks in the months before conversion: 80% to 95%. Probability of a Freddie Mac portfolio intervention: 10% to 20%. Probability of back office complications that delay 10% of conversions by three days or more: 50%.

The trade: Overweight Gold specified pools, underweight Fannie Mae specified pools

Exhibit 3: The tradeable float in some FGLMC coupons is low

Source: eMBS

* * *

A new sheriff in town

When Federal Housing Finance Agency Director Mel Watt’s term ends in January, someone new will step into a position with power large and small over MBS. The issues on the table range from guarantee fees, underwriting guidelines, credit risk transfers, the Single Security initiative that has led to UMBS and ongoing efforts to end the 10-year-old Fannie Mae and Freddie Mac conservatorship. Any material change, however, will run into deeply entrenched and well-funded constituencies that rely on the current system including lenders, servicers, realtors, homebuilders, housing advocates and investors. A number of names have circulated as possible replacements for Watt (here), with Mark Calabria, chief economist to Vice President Mike Pence, recently reportedly in the lead. The likely bias of any new director will be to reign in the footprint of the enterprises. That could come in small ways such as revising affordable housing goals. It could also come in big ways for MBS investors such as reducing the allowable debt-to-income ratio on new loans; loans with DTI greater than 43% constituted [XX%] of 30-year MBS this year. A new director could also revise guarantee fees or loan level price adjustments, making some loans more likely to end up in bank portfolios or private securitizations. Any active efforts to liquidate or privatize parts of the enterprises could shake confidence in the implicit government guarantee. Agency MBS next year arguably will have more regulatory risk than any time since December 2013 when Watt was confirmed. Although the risk is hard to quantify, it looks broadly biased to reduce marginal MBS supply. Although that should help MBS spreads, policy change would likely be idiosyncratic with impact on parts of the market rather than all.

Probability of policy that reduces MBS supply in the first half of 2019: 10%. In the second half of 2019: 25%. Probability that it comes through tighter underwriting guidelines: 25%. Probability that it comes through higher guarantee fees: 10%.

The trade: Overweight pools with concentrations of high DTI loans since any tightening in allowable DTI would reduce refinancing risk.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.