Uncategorized

Proposed Fed liquidity rules mean bad news for Ginnie Mae

admin | November 9, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

The recently proposed Fed easing in liquidity requirements for some of the largest US super-regional banks, coupled with elimination for smaller institutions, likely spells bad news for Ginnie Mae securities. The looser rules will likely trim demand for Treasuries and Ginnie Mae. But where strict liquidity requirements go away entirely, banks in the extreme could revert back to levels of Treasuries and Ginnie Mae securities prevailing before strict liquidity rules applied, reducing holdings of Ginnie Mae MBS and CMOs over time by as much as 80%. But because of attractive carry in Ginnie Mae MBS, the best timing for going underweight the sector may be a few months away.

Eliminating LCR for $50- to $250-billion banks

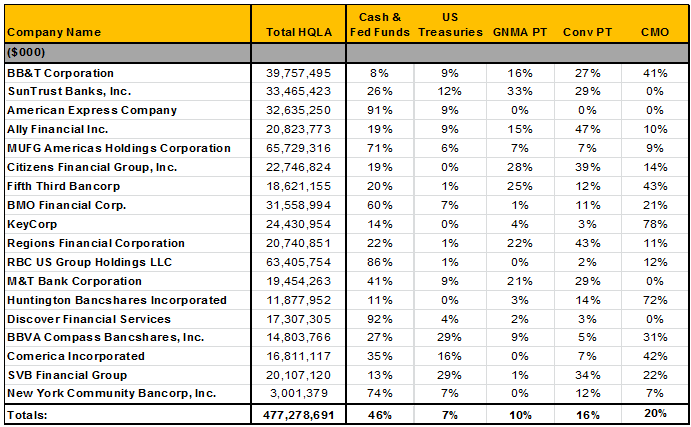

While the market focused primarily on changes to the liquidity coverage ratio (summarized here) for five large super regional banks, the potentially more significant change is the elimination of LCR requirements for banks between $50 billion and $250 billion in total assets. The 18 institutions likely affected if strict LCR requirements disappear hold $477 billion in High Quality Liquid Assets or HQLA (Exhibit 1). That includes cash, excess reserves, Treasuries and MBS pass-throughs and CMOs. These institutions look unlikely to rotate out of those assets en masse if the proposed changes go into effect, but they would no longer have strict regulatory incentives to hold Treasuries or Ginnie Mae MBS. Additionally, the nominal reduction in LCR needs for larger banks would skew their existing stock of liquid assets, creating an overweight of the safest Level I liquid assets.

Under the existing rules, banks can satisfy LCR with two tiers of liquid assets. Level I assets must make up a minimum of 60% of a bank’s liquidity bucket and include cash, excess reserves, and instruments backed by the full faith and credit of the US such as Treasuries and Ginnie Mae MBS. Level II assets fall into Level IIA assets, including conventional MBS and CMOs and GSE debt, and Level IIB assets, including common stock and non-financial corporates. Collectively, Level II HQLA can make up 40% of a bank’s liquidity store with Level IIB assets capped at 15% of that contribution. If the Fed proposal goes through, this shift to a Level I overweight may prove to be significant.

Exhibit 1: Banks with $50B to $250B in total assets; $475B of HQLA needs may disappear

Source: SNL Financial, as of 6/30/2018

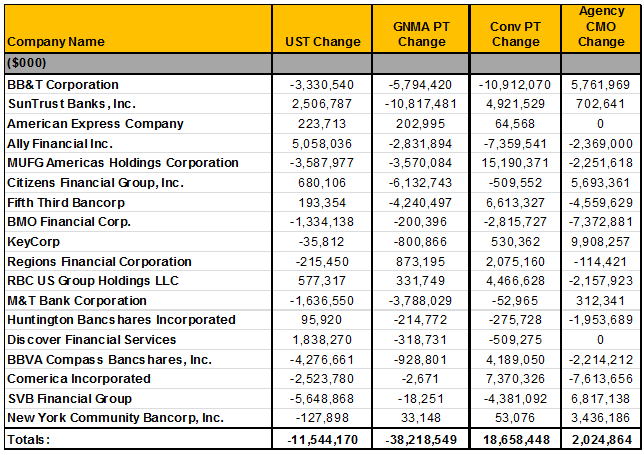

If past is prologue holdings of Ginnie Mae MBS may fall by as much as 80% for banks between $50 and $250 billion in total assets – translating to a reduction in holdings of approximately $40 billion. Holdings of Treasuries may fall by a third, yielding a relatively small $11billion reduction. The elimination of LCR at these banks may yield an increase in demand for conventional MBS, which could rise as much as 20%.

These potential changes follow from holdings of each asset class at the affected banks as of the fourth quarter of 2010, before current LCR requirements started forming. The Basel III rules and the concept of liquidity coverage first came out of the Basel Committee in December 2010. Bank holdings of HQLA as share of total assets at this point offer a useful guide to where holdings may shake out in the rule’s absence. In general, HQLA share was much lower. Conventional MBS are the likely beneficiary of reductions in Ginnie Mae and Treasury holdings. A reversion to a late 2010 asset mix would lift conventional pass-through holdings by $18.7 billion, reduce Ginnie Mae MBS by $38.2 billion and Treasuries by $11.5 billion (Exhibit 2). Additionally, we would expect the mix in CMO demand to swing back towards conventional issuance. While Ginnie Mae will still maintain the benefit of being a zero percent risk-weighted asset, the banking system is flush with both risk-based and common capital as a whole, potentially giving little benefit to the lower risk weighting on Ginnie Mae MBS and CMOs.

A few obstacles likely stand in the way of immediate asset allocation, however. These securities on average now trade below book value, leaving banks reluctant to sell and realize losses through income. Of course, banks could harvest gains against offsetting losses. Healthy shares of MBS also now sit in held-to-maturity portfolios, which prevent banks from selling except for rare circumstances. And banks with $100 billion to $250 billion in assets will still have to conduct quarterly liquidity stress tests, possibly leading bank examiners, management or shareholders to hold more liquid assets than they might in late 2010. Still, demand, especially for relatively less liquid and lower-yielding Ginnie Mae MBS, will likely fall.

Exhibit 2: GNMA Pass-through holdings may fall as much as 80%

Note: numbers reflect the change from current holdings if the securities’ share of total bank assets reverted to December 2010 levels. Source: SNL Financial, as of 6/30/2018. APS calculations.

Easier LCR rules for $250- to $700-billion banks

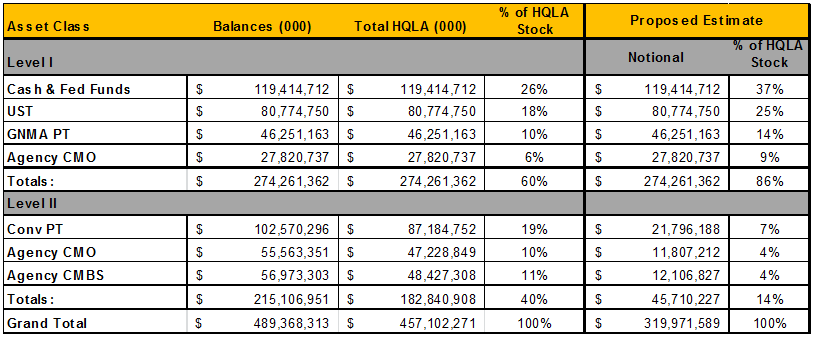

The reduction in overall HQLA needs for banks between $250 billion and $700 billion in total assets could materially reduce needs for full faith and credit instruments for the foreseeable future. If the five affected banks are currently at the regulatory cap on Level II assets the potential 30% reduction in overall HQLA needs would increase their Level I allocation to 86% of their HQLA stock. We derive this by taking the balances of Level I assets across the five affected institutions making an assumption that one-third of agency CMO holdings are Ginnie Mae, broadly consistent with overall issuance, totaling $275 billion of Level I HQLA. We then size the banks’ existing conventional pass through, CMO and agency CMBS exposures to 40% of the HQLA stock or just over $450 billion in total HQLA. We then reduce the overall HQLA amount by 30% to $320 billion and carry the existing Level I stock of $275 billion over – making it 86% of the overall stock giving these banks a potentially huge cushion of Level I assets that would have to be drawn down before they hit their minimum allocation and invest another marginal dollar in an equivalent Level I asset. This cushion may prove to be integral as the Fed steadily drains excess reserves from the system through the systematic reduction in the size of their securities portfolio. While there have been concerns that reduction in reserve balances will put pressure on short term funding markets given banks’ reliance on reserve balances to satisfy their LCR requirements, this proposal, if passed would certainly remove some of that pressure.

Exhibit 3: Level 1 HQLA may grow to as much as 86% of total HQLA at certain banks

Source: Amherst Pierpont, SNL Financial as of 6/30/2018

Weighing the trade: Long FNCL, short G2SF

While the proposed revisions to bank liquidity rules clearly create incentives for banks to reallocate from Ginnie Mae to conventional MBS, waiting for Ginnie Mae MBS to widen to Fannie Mae for now involves negative carry (Exhibit 4). At current dollar roll financing, going short G2SF 4.0% and long FNCL 4.0%s at a 1×1 hedge ratio involves 4.56/32s of annualized negative. Matching duration by going short 1.12 units of G2SF 4.0% for every 1.00 unit of FNCL 4.0%s involves 10.14/32s of annualized negative carry.

Exhibit 4: Negative carry in shorting Ginnie Mae/Fannie Mae 4.0% swap

Source: Bloomberg as of 11/9/18

Investors may have a better entry point for selling the Ginnie/Fannie 4.0% swap in the first half of next year. By that time, the comment period on the Fed proposal will be closed and prospects and timing for new liquidity rules should be clearer. The market also should be through the seasonal low point for prepayments, reducing the current interest in the relatively faster prepayments in discount Ginnie Mae MBS. The transition of Fannie Mae and Freddie Mac MBS into the new UMBS also should be clearer. Investors may miss some of the widening of Ginnie Mae to conventional MBS, but a good time to put the trade on should come.