Uncategorized

LIBOR transition issues come up in the ARM market

admin | November 6, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

The challenges of one day leaving LIBOR behind and finding a better index to set borrowing rates has finally started to pick up in the market for mortgage loans. Originators and investors in Fannie Mae and Freddie Mac ARMs have started to wrestle with possibly resetting the index on the loans and securities and ending issuance of new LIBOR instruments. The Federal Housing Finance Agency reportedly will mandate the enterprises move quickly in 2019 on this and other aspects of LIBOR transition. LIBOR ARMs could become a legacy market, with a Treasury index a strong contender to replace it.

Several investors within the last week have indicated that Fannie Mae or Freddie Mac had reached out to discuss the challenges of changing the index on LIBOR ARMs. Fannie Mae currently has $64.5 billion of LIBOR-indexed ARMs outstanding with average monthly issuance this year of $603 million. Freddie Mac has $46.5 billion outstanding with an average month issuance this year of $323 million.

Unlike the enterprises’ LIBOR exposure in its interest rate derivatives, debt and MBS, it’s ARM loans involve consumers rather than institutions. According to several investors, the enterprises are considering leaving LIBOR in place on all current loans and consequently keeping the index for ARM MBS. The rationale seems to be that this would avoid the complexities of changing the index on millions of loans and explaining the change to consumers. The Intercontinental Exchange or ICE, the official publisher of LIBOR, intends to keep publishing LIBOR rates after 2021 using either bank submissions or other methods. This would allow the enterprises to keep LIBOR in place on ARMs and related MBS even if other markets moved away.

Some investors and originators have also reported that the enterprises may stop buying and securitizing ARMs indexed to LIBOR to minimize outstanding balances if traditional LIBOR settings went away in 2021, as US and UK regulators have indicated. Instead, the enterprises reportedly are considering requiring new ARMs to use a constant maturity Treasury or CMT index since those rates already are available and transparent, and both enterprises already securitize CMT ARMs. The Ginnie Mae ARM market uses CMT exclusively.

The Mortgage Bankers Association has had a working group focused for more than a year on LIBOR transition.

The activity in the mortgage loan market comes as work to transition away from LIBOR by 2021 continues to accelerate. The transition from LIBOR to SOFR is now three years and a holiday season away. The Treasury Borrowing Advisory Committee (TBAC) discussed the status and summarized progress of the transition for the Treasury Department at their meeting ahead of the November quarterly refunding. SOFR is backed by a deep, liquid market that averages $700 billion in daily transactions, compared to overnight Eurodollars which now average roughly one-tenth of that. Significant challenges remain ahead of the transition: the development of a robust SOFR term structure and futures market are in their infancy, and SOFR-linked issuance is building but so far modest.

The highlights

- The Financial Conduct Authority announced in July 2017 that it will no longer sustain LIBOR through the current panel bank submission process beyond the end of 2021.

- The secured overnight financing rate (SOFR) is scheduled to officially supplant US dollar LIBOR as the benchmark short-term financing rate.

- USD LIBOR is referenced in roughly $200 trillion notional worth of financial contracts, covering financial derivatives such as interest rate swaps, swaptions and Eurodollar futures, and cash products.

- Approximately $36 trillion notional of financial contracts which utilize LIBOR as a benchmark rate will still be outstanding in 2022. The vast majority is comprised of financial derivatives, but the total also includes $920 billion in securitizations, $554 billion in business loans, $516 billion in consumer loans and $288 billion of floating rate notes.

- SOFR is a secured overnight financing rate based on borrowing collateralized by Treasury securities, which averages over $700 billion in daily transaction volume across a large number of market participants.

- LIBOR is an unsecured financing rate which spans tenors from overnight to one year. Borrowing rates are submitted by a panel of global banks based on actual transactions when available, or otherwise imputed from similar money market rates. Estimates are that three-month LIBOR is currently priced off $500 million or less of daily transactions.

- Efforts to develop a term structure of SOFR rates and a functioning futures and options market are still in their infancy, but regulators are hoping the markets mature prior to the transition.

- There will be term and credit spread adjustments required to migrate from an unsecured, term LIBOR rate to a secured, potentially overnight only SOFR rate in existing contracts. There are many proposed calculation methods, none of which are likely to be market value / tax / accounting neutral across all products and counterparties. This could create litigation and liquidity risk if SOFR market is not sufficiently developed at the time of LIBOR cessation.

- Some financial contracts do not contain fallback language to an alternative benchmark rate, which also increases litigation risk.

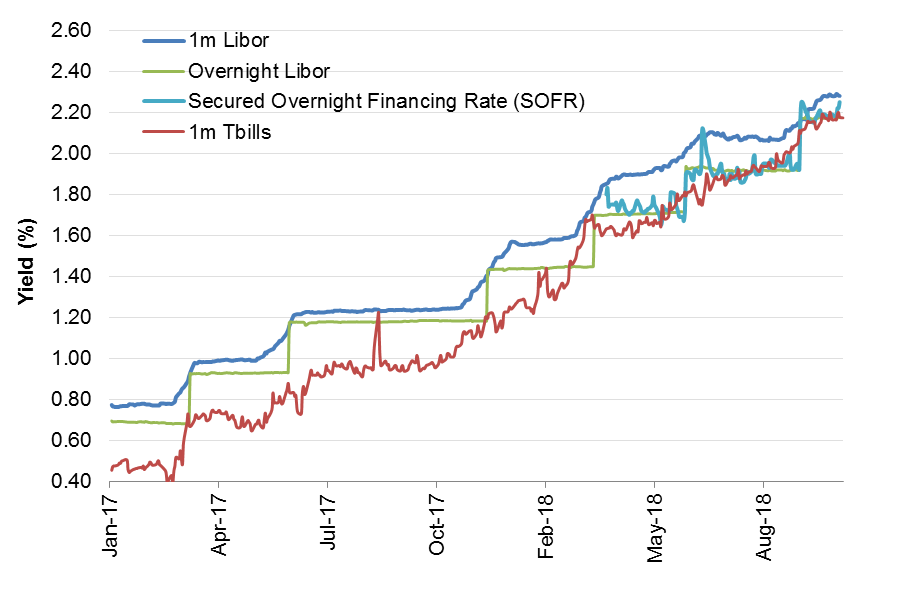

Migrating to a deeper, more indicative market

The Fed began publishing overnight SOFR in April 2018, though a longer indicative history of the three repo rates (TGCR, BCRG and SOFR) is available along with daily transactions volumes. A comparison of overnight and one-month rates is shown in Exhibit 1. The SOFR and Treasury bill rates are based on very deep and liquid markets. Average daily trading volume in SOFR is nearly $800 billion per day, and Treasury bills (all maturities) currently average roughly $100 billion in trading per day.

Exhibit 1: Select short-term financing rates

Source: Bloomberg, APS

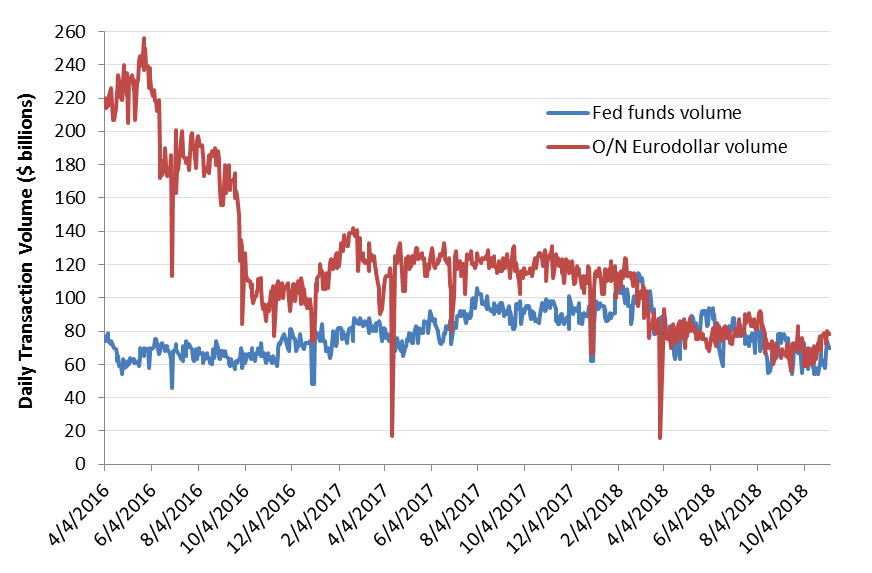

Both overnight and term Eurodollar financing has been decreasing steadily post-crisis as new bank and money market regulations contributed to a preference for shorter-term funding, and quantitative easing created a massive buildup of onshore bank reserves. Tax reform and corporate repatriation of offshore funds further reduced overnight Eurodollar financing down to the level of fed funds (as shown in Exhibit 2), both of which average approximately $70 – $80 billion in daily transaction volume.

Exhibit 2: Overnight fed funds and Eurodollar borrowing

Source: New York Federal Reserve Bank; data from FR 2420 report.

It’s not that the need for the additional $35 billion of funding has disappeared since the beginning of 2018, but that it has moved onshore and is not currently being captured by the Fed’s report. The Fed submitted a request to modify data collection of the FR2420 report (emphasis added):

The Board proposes adding a new section, Part D, to the FR 2420, intended to capture short-term wholesale unsecured deposits that are economically equivalent to federal funds purchased in Part A or Eurodollars in Part B. The primary target for this collection would be reporting institutions that, in recent years, shifted deposits from branches in the Caribbean Islands [2] to the U.S., which has caused this borrowing to fall outside the scope of the current FR 2420. The proposed Part D would also collect data from institutions that have historically booked all or a portion of such deposits in their U.S. offices.

Since June 2016, some Eurodollar activity from Cayman and Nassau branches of foreign banks has shifted to U.S. branches of those banks, causing Eurodollar volume reported on the FR 2420 to decline significantly, obscuring vision into the wholesale funding market and reducing the robustness of the data used in calculating the OBFR. Federal Reserve staff are aware of at least roughly $35 billion in overnight Eurodollar transactions that have moved from the Cayman Islands to New York. The motivation has been described as the simplification of corporate structure for the drafting of living wills. Accordingly, the Board proposes to add Part D to the FR 2420 to capture these short-term, wholesale, domestic deposits.

Corporate cash on deposit at domestic banks will be re-incorporated into the overnight bank funding rate and volume data.

Term Eurodollar – that is LIBOR markets – are more difficult to monitor. The data can only be collected by the Fed if one of the counterparties falls under Fed supervision by having an onshore branch or banking facility. The Fed does not make such data public, but they do release reports that incorporate it on a macro basis from time to time. The TBAC report mentions that three-month LIBOR rates are based on a mere $500 million of average daily transaction volume.

Transitioning from an unsecured to secured financing benchmark

The Federal Reserve’s Alternative Reference Rate Committee (ARRC) chose to transition from LIBOR to SOFR. LIBOR is an unsecured, originally interbank financing rate which post-crisis was more broadly defined to reflect a financial market financing rate for US dollars borrowed offshore. SOFR is a secured, overnight financing rate collateralized by US Treasury securities (or repo, complete definition in the Appendix). Although term repo does exist, so far there is no SOFR term structure of spot rates in the same way there are LIBOR rates from overnight to 1 year.

Reference rate committees in the ECB, Japan and the UK so far have chosen to replace their “IBOR” with a newly constructed unsecured financing rate. The US and Swiss central bankers have both designated a secured financing rate as an alternative reference rate. All are overnight rates.

Differences between overnight SOFR and 3-month LIBOR are expanded upon in the TBAC presentation (from slide 7):

- 3M LIBOR and o/n SOFR differ in two aspects:

– SOFR is secured and LIBOR is unsecured. LIBOR is inherently bank-credit sensitive, pro-cyclical asset whereas SOFR is collateralized and largely cleared, hence a counter-cyclical asset

– 3M LIBOR is a term rate vs SOFR is an overnight rate. We find this difference to be more salient, as noted by volatility in 3M LIBOR / 3M FF OIS basis

- 3M LIBOR/OIS tend to widen on funding “stress” scenarios. This is not the case for SOFR

The lack of a cyclical credit component in SOFR as compared to LIBOR means that the reference benchmark will no longer reflect funding stress, widening on weakness in the financial sector. This may also inhibit the ability for SOFR based instruments to hedge general bank funding risk. The TBAC presentation expands upon the differences between LIBOR and SOFR from a bank perspective (slide 12):

- Banks generally responded to increased regulation and improved liquidity risk management with the extension of maturity profiles of unsecured borrowings.

- Post-crisis shifts towards deposit funding (commercial/demand deposits) increased the relative size of certain short-to medium-duration liabilities.

Overall the exposure to funding spread resets of liabilities arguably has been reduced.

- However banks still have to manage funding spread risks due to spread duration gaps between assets with longer re-pricing cycles and shorter-dated liabilities –exposing banks to a sudden widening of sector credit spreads.

There is still a need for ALM instruments whose performance is linked to unsecured bank credit spread such as Libor.

- On the other hand unsecured inter-bank lending volumes have collapsed since the crisis resulting in Libor being less representative of actual bank funding costs.

Will the banking industry require new hedging instruments based on unsecured benchmarks?

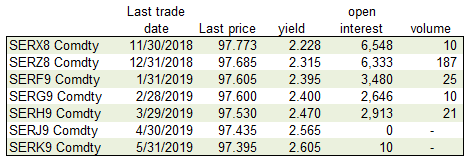

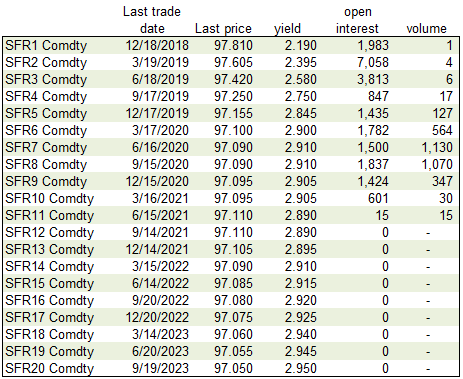

Slow start in SOFR futures

The development of a SOFR term structure and derivatives market is paramount, if SOFR swaps are ever going to credibly supplant LIBOR swaps and Eurodollar futures. Three-month and one-month SOFR futures began trading on the Chicago Mercantile Exchange in May 7, 2018. Six months into trading, SOFR futures volume is somewhat anemic (Exhibit 3 and 4):

Exhibit 3: SOFR futures – 1 month

Source: Bloomberg, CME; trading volumes as of 10:30am 11/6/2018.

Eurodollar and Treasury futures are among the most liquid contracts in the world, with trading volume in the front contracts normally exceeding 100k per day, and open interest in the millions.

Exhibit 4: SOFR futures – 3 month

Source: Bloomberg, CME; trading volume as of 10:30am 11/6/2018.

Term and spread / credit adjustments

ARRC has proposed a variety of methodologies for calculating an appropriate spread to account for differences in the term and credit components between overnight SOFR and a term LIBOR rate in existing products. Ultimately much of this will depend on how quickly the SOFR term and futures markets develop. Details on these approaches can be found in the TBAC presentation and in ARRC publications.

Issuance of SOFR floaters

The first SOFR-based floating rate note was issued by Fannie Mae in July 2018, a $6 billion, three tranche deal of 6 months, 1 year and 1 ½ year maturities. Since then 10 other issuers have come to market with SOFR floaters totaling $17 billion notional. It’s encouraging, but broader adoption of SOFR-linked debt by both issuers and investors is required to build momentum. TBAC recommended that Treasury evaluate issuing floating rate notes off SOFR. The GSEs and the financials are among the issuers more preferred by investors, based on a September 2018 survey.

Appendix: Definitions

From a BIS speech by Simon Potter of the New York Fed, Money markets after liftoff – assessment to date and the road ahead, definitions in an appendix:

Eurodollars are unsecured U.S. dollar deposits held at a bank or bank branch outside of the United States or domestically through an international banking facility (IBF), whereas federal funds are domestic borrowings by U.S. banks and U.S. branches and agencies of foreign banking organizations (FBOs). Although the Federal Reserve can impose reserve requirements on net Eurodollar deposits of U.S.-based banks, it has imposed a zero reserve requirement since 1990, making the treatment of Eurodollar deposits effectively the same as

federal funds borrowings.

Shortcuts:

TGCR + GCF + Bilateral Repo = SOFR

TGCR + GCF = BGCR

OBFR = O/N Fed funds + O/N Eurodollars

The following definitions are taken from the Treasury repo reference rates information on the New York Fed website.

The Tri-Party General Collateral Rate (TGCR) is a measure of rates on overnight, specific-counterparty tri-party general collateral repo transactions secured by Treasury securities. Specific-counterparty transactions refer to those in which the counterparties involved know each other’s identity at the time of the trade. General collateral transactions are those for which the specific securities provided as collateral are not identified until after other terms of the trade are agreed. The rate excludes GCF Repo transactions and transactions to which the Federal Reserve is a counterparty. It is based on transaction-level tri-party data collected from the Bank of New York Mellon (BNYM) only.

The Broad General Collateral Rate (BGCR) is a measure of rates on overnight Treasury general collateral repurchase agreement (repo) transactions. General collateral repo transactions are those for which the specific securities provided as collateral are not identified until after other terms of the trade are agreed. The BGCR includes all trades in the Tri-Party General Collateral Rate plus GCF Repo transactions.

The Secured Overnight Financing Rate (SOFR) is a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities. The SOFR includes all trades in the Broad General Collateral Rate plus bilateral Treasury repurchase agreement (repo) transactions cleared through the Delivery-versus-Payment (DVP) service offered by the Fixed Income Clearing Corporation (FICC), which is filtered to remove a portion of transactions considered “specials”.

The SOFR, the BGCR, and the TGCR are each calculated as a volume-weighted median, which is the rate associated with transactions at the 50th percentile of transaction volume. Specifically, the volume-weighted median rate is calculated by ordering the transactions from lowest to highest rate, taking the cumulative sum of volumes of these transactions, and identifying the rate associated with the trades at the 50th percentile of dollar volume. At publication, the volume-weighted median is rounded to the nearest basis point.

The Overnight Bank Funding Rate (OBFR) is calculated using federal funds transactions and certain Eurodollar transactions. The federal funds market consists of domestic unsecured borrowings in U.S. dollars by depository institutions from other depository institutions and certain other entities, primarily government-sponsored enterprises, while the Eurodollar market consists of unsecured U.S. dollar deposits held at banks or bank branches outside of the United States. U.S.-based banks can also take Eurodollar deposits domestically through international banking facilities (IBFs).

The overnight bank funding rate (OBFR) is calculated as a volume-weighted median of overnight federal funds transactions and Eurodollar transactions reported in the FR 2420 Report of Selected Money Market Rates. The New York Fed publishes the OBFR for the prior business day on the New York Fed website at approximately 9:00am.