Uncategorized

The Fed’s wishful thinking

admin | September 28, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

The FOMC’s economic and policy projections released September 26 represent an unrealistically optimistic scenario. If things turn out the way the FOMC expects, it will be the most benign soft landing in history. I hope Chairman Powell and the FOMC are right, but it is hard to imagine that we will be so lucky. Examining some of the key elements of the projections provide some sense of the vulnerabilities of the FOMC’s outlook and how reality could diverge from the Happily Ever After story told in the Fed’s projections released this week.

Setting the context

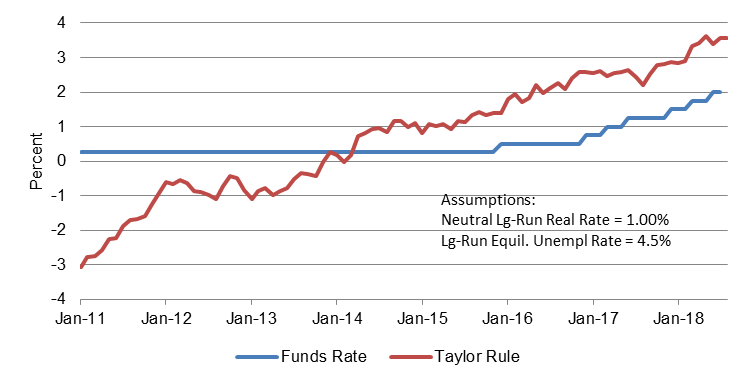

Before exploring the outlook for the next few years, it is helpful to set the stage. Monetary policy in this cycle has been tremendously easy for years. Relative to the FOMC’s own estimates of longer-run neutral monetary policy and the equilibrium unemployment rate, a standard Taylor Rule calculation shows that monetary policy has been easier than unemployment and core inflation would normally dictate by a substantial margin for nearly five years running (Exhibit 1).

Exhibit 1: Fed policy compared to the Taylor rule

Source: Bloomberg.

In fact, since the middle of 2014, the Taylor Rule recommendation for monetary policy has averaged 130 bp above the actual fed funds rate – and that is before accounting for the extra stimulus provided through the balance sheet and QE. Moreover, despite Fed rate hikes so far, the August reading showed that actual policy was more than 150 bp easier than the Taylor Rule suggested,a wider gap than the month before the FOMC lifted off from the zero bound.

With that as context, the FOMC outlook as indicated by the economic and policy projections lay out a scenario where the Fed can painlessly transition to a perfect economic environment, one where economic growth is in line with the long-term trend, inflation is exactly at the 2% target, and the unemployment rate will creep up toward its longer-run equilibrium. Here are, as I see it, some of the biggest vulnerabilities to the FOMC’s sunny outlook.

- Strong growth in 2018 is not a sugar high.

FOMC estimates of 2018 real GDP growth have been revised up for five straight quarters beginning with September 2017, taking the expectation from 2.1% to 3.0%. There has also been some bleedover into 2019 estimates, which have also been raised over the past five quarters by a cumulative 0.5 percentage points to 2.5%. Much of this boost to growth has been attributed to the passage of tax reform last December. Fed officials and especially Fed Board staff have long been known for overwhelmingly focusing on the demand side of the economy, so it is perhaps not surprising that FOMC participants have implicitly ruled out any persistent supply side boost from pro-growth changes in tax and regulatory policy over the last two years, even as business investment has surged and productivity growth has shown tentative signs of accelerating noticeably. How do we know that the Fed sees no persistent boost to growth? The 2020 and longer-run growth estimates have not budged by even a single tenth since December 2017.

Relative to the Fed’s apparent view, there are two alternative explanations of growth that would have important implications for the path of monetary policy. First, it could be that the boost to economic growth includes a significant element of persistent supply-side boost, as lower tax rates, more favorable tax treatment of investment, and growth-friendlier regulatory and tax policy. In such a scenario, longer-run growth is likely higher than the FOMC’s 1.8% projection, which probably means that the neutral level of the fed funds rate is higher than the Fed currently estimates and thus current policy remains easier than the FOMC believes.

Alternatively, the substantially higher-than-trend economic growth in 2018 could be mostly a function of the chronically easy monetary policy referenced in the chart above, in which case it is dubious that growth would slow as quickly as the FOMC currently projects given that, by the Fed’s own reckoning, policy will remain easy for at least the better part of another year.

2. Unemployment rate below 4% for four straight years.

With the addition of 2021 projections, we can now see that the Fed expects the unemployment rate to remain below 4% for at least four years straight. This would be an extraordinary run. In the last nearly 50 years, the unemployment rate has been below 4% combined total of only six months, all in 2000. The last time that the unemployment rate held below 4% for an extended period of time was the late 1960s, which directly led to the accelerating pace of inflation in the 1970s. Anecdotal and survey evidence suggest that the labor market is under increasing stress, which may finally be leading to a meaningful pickup in wage gains. Can we expect the unemployment rate to remain so low for at least three more years without creating the sort of significant imbalances that have in the past led to problems in the economy?

3. Phillips Curve is dead.

The FOMC projections suggest that the Fed believes that there is no relationship at all between growth and unemployment versus inflation. With growth sharply above trend in 2018 and 2019 and the unemployment rate far below the FOMC’s estimate of equilibrium, the inflation estimates are in the 2.0% to 2.1% range through 2021. Most economists would certainly agree that the Phillips Curve is far flatter today than it was in the past, but the FOMC projections suggest that the Phillips Curve is outright dead. Of course, as I have noted in the past, a central bank simply can’t project inflation very far above its target and maintain its credibility. I am not criticizing the Fed’s inflation forecasts, which I think are meaningfully too low, but instead suggesting that they should not be taken as face value. It is important to keep in mind that market participants should not take much comfort in the Fed’s assertion that it will hit its target as far as the eye can see.

4. Relationship between growth and unemployment.

Standard economic theory suggests that when economic growth is above trend, the unemployment rate falls, and when growth is below trend or negative, the unemployment rate rises. In contrast, the latest FOMC projections have the unemployment rate leveling out in 2019 and 2020, when growth is still noticeably above trend, and actually rising in 2021, when growth settles to exactly their estimate of the longer-run trend.

There are two worrisome aspects to the unemployment rate forecasts. First, standard economic theory suggests that the unemployment rate should probably fall significantly further than the Fed is projecting, creating an even more severe overshoot and higher odds of serious imbalances developing in the economy. Second, the higher unemployment rate projection for 2021 suggests that FOMC participants are taking an extreme position that the economy has a strong tendency to revert to its long-run equilibrium state. While that may in fact occur, past experience suggests that the economy has a lot of inertia. Once animal spirits become high, tailwinds pick up speed, or whatever other analogy you prefer, the economy typically remains strong until something dramatic happens, either a shock of some sort or a sharp swing in monetary or fiscal policy.

5. Relationship between monetary policy and the economy.

Similarly, standard economic theory and historical experience indicate that once the economy generates the sort of above-trend momentum that we currently see, it takes more than the Fed simply reaching a neutral policy stance to tamp down growth. Perhaps this time will be different, and moving the funds rate one or two notches above the FOMC’s estimate of longer-run neutrality will produce a growth slowdown to below 2%. However, this scenario, the ephemeral soft landing that has rarely been sighted outside of Fed research, represents a best-case possibility and not an especially plausible one at that. In most prior economic cycles, when the economy has overshot as far as it already has, the Fed has had to take monetary policy well into restrictive territory to cool things off, usually by enough that the economy ultimately rolled over. Of course, the FOMC is never going to include a recession in their projections, but, again, market participants should not take much comfort from the benign scenario laid out in the Fed projections.

6. Financial conditions as a kicker.

Chairman Powell and others at the Fed have emphasized the increasingly important role of financial conditions in the performance of the economy. Powell noted earlier this year that the last two economic cycles have ended with financial market upheaval rather than the old-school 20th century inflation-driven overshoot. Given that, the following chart should be considered worrisome.

Exhibit 2: Chicago Fed financial conditions index

Source: Chicago Federal Reserve

By this gauge, financial conditions, after eight rate hikes, are easier than they have been at any point in the last 25 years (including during the late 1990s equity bubble and the 2000s housing and liquidity bubble). The FOMC projections lay out a story where the central bank has done most of the hard work to return policy to neutral and only needs a handful of additional moves to get the economy on a sustainable perfectly-Goldilocks track. This would be awesome, but there is clearly a risk that a more forceful effort by the Fed will prove necessary to not only bring the economy back into alignment but also to cool off financial conditions.