Uncategorized

Oasis of Prosperity

admin | September 14, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

As developments overseas once again threaten to intrude on a rosy domestic economic outlook, Fed officials would be well advised to keep their focus on growth, employment, and inflation conditions here. Contrary to Chairman Greenspan’s contention that the US might be caught up in the international events of 1998, the U.S. today is uniquely positioned to be an “oasis of prosperity” even when some of our trading partners struggle. Domestic demand and deep financial markets create the buffer.

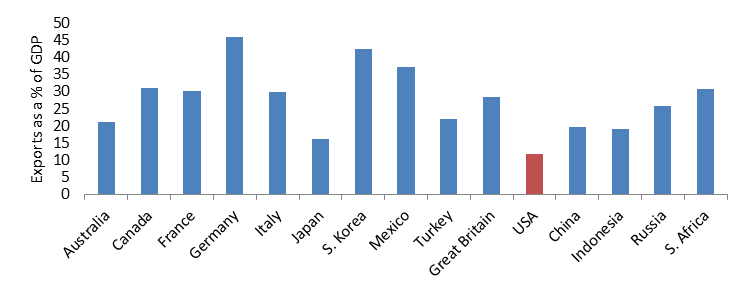

The U.S. economy, while more open today than it has been historically, remains more “closed” than other major economies. By “closed,” economists mean that activity is primarily driven by domestic demand rather than trade. Exports make up far less of the U.S. economy than any other G-20 country (Exhibit 1).

Exhibit 1: Exports as a percentage of GDP

Source: OECD.

U.S. financial markets also are by far the deepest and most liquid in the world. Certainly, the transmission from global financial markets to U.S. markets is more important today than it was decades ago, but it is still far less than the other way around. Indeed, one would be hard pressed to find a credible example where developments in overseas financial markets impacted U.S. financial markets by enough or for long enough to make a discernible difference for the U.S. economy.

In September 1998, Fed Chairman Alan Greenspan declared that “it is just not credible that the United States can remain an oasis of prosperity unaffected by a world that is experiencing greatly increased stress.” Over the next three months, the Federal Reserve eased three times despite booming growth and a 4.5% unemployment rate, partly in response to domestic ripple effects of the collapse of Long-Term Capital but also due to significant concerns about the global economy. Though an easing is not in the offing currently, there are many similarities between 1998 and 2018, as many market participants believe that the U.S. economy, despite being robust at the moment, cannot possibly sustain its strength given the difficulties elsewhere in the global economy. This view has not borne out historically. In fact, in past episodes, when the Federal Reserve has altered its policy course due to international considerations, it has arguably been a mistake every time.

Fed policy in 1997-1998

The late 1990s episode is the first time that the FOMC explicitly altered policy largely due to international considerations. There had been prior instances where global factors played in policymakers’ thinking, of course, but only to the extent that they altered the domestic outlook. In 1997, after hiking in March, the Fed refrained from further rate increases in the spring and summer, as currency devaluations in Thailand, Indonesia and South Korea, among others, led to concerns that a stronger dollar would drag down U.S. growth. The Fed also may have felt that it needed to refrain from rate increases to make it easier for Asian central banks to support their currencies.

Then in the summer of 1998, a sense of instability developed. Russia defaulted on its sovereign debt in August, shocking market participants, and Long-Term Capital Management, a huge hedge fund with eye-popping leverage, went bust in September, requiring a substantial Wall Street-orchestrated bailout. Days after arranging the LTCM bailout, the FOMC lowered rates on September 29. The ensuing FOMC statement noted:

“The action was taken to cushion the effects on prospective economic growth in the United States of increasing weakness in foreign economies and of less accommodative financial conditions domestically. The recent changes in the global economy and adjustments in U.S. financial markets mean that a slightly lower federal funds rate should now be consistent with keeping inflation low and sustaining economic growth going forward.”

Additional easing moves followed in October and November, mainly in an attempt to shore up shaky financial markets. The Fed’s easing in 1998 arguably worked, as financial markets calmed down and had returned to normal by early 1999. However, contrary to Fed fears, neither the global problems nor the financial market gyrations had a discernible impact on the domestic economy.

Real GDP growth averaged 6% in the second half of 1998 and the unemployment rate slid into the low 4%s in early 1999. The FOMC waited too long to reverse the pre-emptive insurance policy that it had adopted, holding policy steady until the second half of 1999, by which time the economy and the stock market were in the process of overheating. As a result, the FOMC ultimately was forced to clamp down hard, raising the fed funds rate target all the way to 6.50% by mid-2000, after the proverbial cattle had left the barn.

Fed policy in 2011-2012

A few years after the 2008 financial crisis, the economy and financial markets had stabilized but the recovery was frustratingly slow. The FOMC had completed QE2 in mid-2011, but the Greek sovereign debt crisis and prospects of a meltdown in Europe spooked the Fed. There were also concerns related to the U.S. nearly defaulting on its debt in August, spurring a downgrade by S&P. In response, the FOMC ratcheted up its forward guidance, extending the projected period over which rates would remain near zero, and initiated Operation Twist in an effort to further depress long-term rates and provide stimulus to the U.S. economy.

It is difficult to argue that the Fed’s moves in 2011-12 were a blatant mistake, but the Fed’s fears related to a sharp downturn in Europe failed to materialize. While U.S. economic growth was sluggish, the unemployment rate steadily declined in 2011 and 2012, and the Fed’s aggressively pessimistic stance likely spooked consumers and businesses, at least one factor that helped to keep animal spirits low during that period. In retrospect, the Fed probably would have been fine to maintain a steady policy and simply keep a close eye on the European situation, which never rose to the level of significantly impacting the U.S. economy.

Fed policy in 2015-2016

The FOMC dots in December 2014 indicated that the median expectation on the Committee for 2015 was not only that the Fed would finally escape its near-zero rate setting but that it would hike rates three to four times. It was not meant to be. Harsh winter weather depressed economic activity early in the year, and policymakers wanted to wait and make sure that growth rebounded in the spring (it did). Then, just as the Committee appeared to be revving up for a September 2015 liftoff, a swoon in the Chinese stock market and currency spilled over into U.S. financial market volatility and spooked an eternally-skittish FOMC. The Committee stood down, noting in its September 17, 2015 statement:

“Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term… The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring developments abroad.”

Ironically, the U.S. stock market had retraced about half of its August swoon by the time of the September FOMC meeting but slid back almost all the way to its late-August lows after the Fed’s vote of no-confidence in the domestic economy. Stock prices did fully recover in October, and the FOMC finally lifted off in December 2015.

Unfortunately, the Chinese stock market swooned again in the first days of 2016, once again derailing expectations of multiple Fed rate hikes for the year. As it had in 2015, the Yellen-led FOMC put its normalization campaign on hold, noting in the January 27, 2016 statement that “the Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.” Once again, in the weeks immediately after the Fed’s dovish statement, the stock market fell further, as market participants were worried that the Fed itself was so worried. In the meantime, the U.S. economy was never much affected by all of the gyrations in China.

As we sit in 2018 with an employment rate below 4%, real GDP growth more than a percentage point faster than the Fed’s estimate of the long-run potential, and increasing signs of overheating in the economy and in financial markets, the 21 months in 2015 and 2016 that the Fed sat idly by, raising rates only once, now looks like a lost opportunity. At the end of 2014, the median FOMC dot projection for the end of 2016 was 2.50%. In actuality, the FOMC finally raised rates for the second time in December 2016, to 0.625%. Virtually every FOMC participant today is saying that the policy rate needs to be about 100 BPs higher than it is. If only the Fed had put less weight on global developments in 2015 and 2016, policy today might be in better alignment with the U.S. economy.

As an aside, there is a common theme in the 1997-98 and 2015-16 episodes. While the wisdom of the Fed’s initial reaction to overseas trouble can be debated, the most obvious mistake made by officials is that, having deviated from the policy path dictated solely by domestic economic conditions, the FOMC has repeatedly in the past failed to play catch up. The 1998 eases and the 2015/16 delays would not have been a lasting problem if the Committee had made up for lost time by hiking rates more aggressively to get back on track once the fleeting global and/or financial market issues cleared up.

Oasis of prosperity

Certainly, Fed officials are not supposed to ignore altogether what is happening beyond our shores. However, history suggests that the FOMC has tended to place far too much weight on global developments than it should in setting domestic monetary policy. Let’s hope that pattern is not repeated in the coming months.