Uncategorized

Come fly with me

admin | September 7, 2018

This material is a Marketing Communication and does not constitute Independent Investment Research.

Recent production delays at Boeing illustrate the bottlenecks that are spreading, especially in the manufacturing sector, as the economy grows at a well-above-trend pace while the unemployment rate slides further below estimates of the natural rate. Economists and policymakers continue to debate the proper stance of monetary policy when wage and price inflation fail to accelerate decisively, despite the fact that the economy is operating well beyond potential. The economy is so hot that it has arguably moved into territory not seen for decades, which could challenge the current confidence of many that inflation will never move much above the Fed’s 2% target.

Bottlenecks in the economy

The economy is currently running quite high. The first area to show serious supply constraints was the labor market. Complaints by firms about the inability to find qualified workers have been plentiful for several years and continue to spread. This year, both the number of initial unemployment claims and the headline unemployment rate have dropped to their lowest levels since 1969.

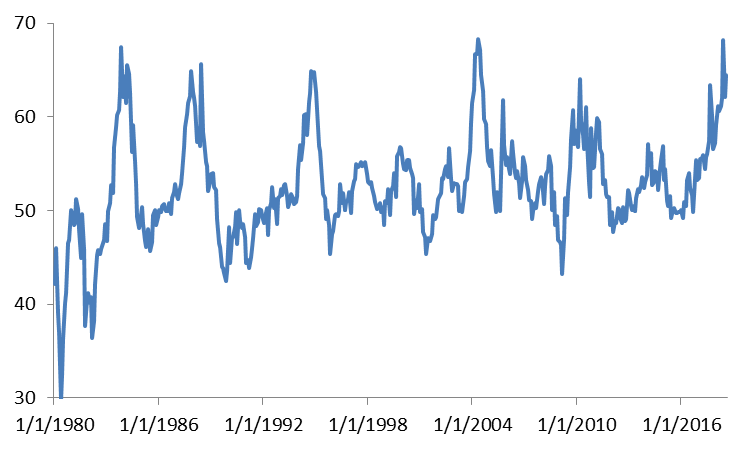

More recently, the signs of constraints in product markets have begun to pile up. The supplier deliveries index in the monthly ISM manufacturing survey has run far above the break-even mark of 50 for almost two years straight, signaling that vendors are taking longer to deliver supplies to factories. In fact, the June and August readings were the two highest since 2004 and, aside from a handful of readings in 2004, the strongest in 30 years (see Exhibit 1).

Exhibit 1: ISM Manufacturing Survey Supplier Devices Index

Source: ISM

The interpretation of a high reading for this measure varies widely depending on the stage of the business cycle. As Exhibit 1 shows, the index tends to spike early in recoveries, as supplier deliveries lengthen back to normal after shrinking dramatically during recessions. Brief surges in supplier deliveries occurred in 1983-84, 1994-95, 2003-04, and 2010, as supply chains and order books normalized after recessions.

Nine years into an expansion, a surge in supplier deliveries means something quite different. A late-cycle deterioration in vendor performance suggests that supply chains are under stress and that bottlenecks may be developing. The last time that the ISM manufacturing survey’s supplier deliveries index exceeded 60 late in a business cycle was the 1987-88 period. At that time, like today, the unemployment rate was also running below estimates of the natural rate.

As the economy strained to meet torrid demand, core inflation accelerated significantly. After declining through much of the 1980s, the year-over-year advance in the core PCE deflator rose from around 3% in early 1987 to a peak of 4.7% in February 1989. In response, the Fed hiked rates by over 300 bp in a year, reaching a cycle peak of 9.875% in February 1989.

This is not to suggest that core inflation is about to accelerate by 200 bp in a year or that the Fed will need to raise rates by 300 bp in 2019. The world is very different today than it was in the 1980s. Most importantly, inflation expectations are well-anchored, which should help to prevent such a dramatic inflation outbreak. Though it would be overly complacent to trust that inflation cannot accelerate simply because it has been well-behaved over the last 20 years.

Boeing as an example of bottlenecks

The recent travails at Boeing offer a concrete example of the sort of strains that are becoming more common in the economy and especially in the manufacturing sector. A September 3rd article in the Wall Street Journal details the difficulties at the airplane maker. Assemblies are being delayed by two key suppliers: an engine maker and a fuselage manufacturer. The engine maker has had trouble smoothing the production process on a new engine, suffering from parts shortages from its own suppliers; the fuselage firm had trouble adding enough workers to keep up with the step-up in the pace of assemblies at Boeing.

Boeing’s deliveries suffered in July, sinking to 29 for the month, down from a norm of over 50. This was a large enough problem that it affected several key macroeconomic indicators for the month, contributing to a drop in durable goods shipments and merchandise exports. Meanwhile, Boeing is running out of room to park the mostly-finished planes that are waiting for engines. It has contracted with the local small airport near its factory to park planes on idle runways, between buildings, and wherever else the airport can make space. The flipside of the drop in shipments and exports in July was a massive rise in inventories of “work in process” aircraft. These swings in the data are likely to be largely offsetting in terms of GDP – lower business investment in aircraft and exports offset by a rise in inventories – but it is rare to see one company’s problems rise to the level of creating distortions in the broad economic data.

Boeing’s order book is so large that a new order placed today will not be filled for years. In an effort to chop through some of the backlog, the firm is trying to ramp up production over the next few years. The difficulties seen in recent months show what happens when labor and product markets get so hot that it becomes tough to grow one’s business.

There is very little in the experience of the last 25 years that can tell us how the economy will respond to these difficulties. Inflation may remain anchored at or near 2%, in which case, firms will probably throw up their hands and stop trying to add workers and expand production in an environment where it is impossible to do so while maintaining an appropriate cost structure. Alternatively, firms are likely to at least try to test the waters to recover some of the cost increases they are experiencing. We will see whether businesses and consumers will accept the grasp at pricing power or not.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.