The Big Idea

Sticky home prices help investors

Steven Abrahams | September 30, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

In the five years before Fed Chair Paul Volcker started a fight against inflation that would put him in the history books, home prices in California ran up by 140%. And when Volcker then pushed fed funds to 20% three times between 1980 and 1981 and sent 30-year mortgage rates above 18% and helped trigger two recessions, home prices in California did a strange thing: they kept rising. Between 1980 and the end of 1982, home prices in California went up another 17%. And that says something important about the way home prices—and markets influenced by home prices—are likely to play out over the next few years.

Recent work by Stephen Stanley and a recent review by Brian Landy of Moody’s home price forecasts both point to flat prices for the next few years. But part of the price story in housing is the tendency for prices to be sticky to the downside, falling much more slowly than they rise. The stickiness of home prices stands to affect a few markets:

- Protecting most exposures in residential credit

- Supporting more cash-out refinancing of agency MBS, and

- Helping investment grade homebuilder credit

Looking not for a clearing price but for a target price

Homes do not trade in a market that continually finds a clearing price largely because owners can stay in a property and continue getting value out of it. If homes did trade in a clearing market, inventory would move continually with the price on every home falling until it sold. Instead, homes usually trade in a market that finds a target price set by the seller. If the seller does not get the target price, the seller can keep living in the house until a buyer comes along and hits the target. Or the buyer can take the house off the market or rent it or only bring the price down in gradual steps.

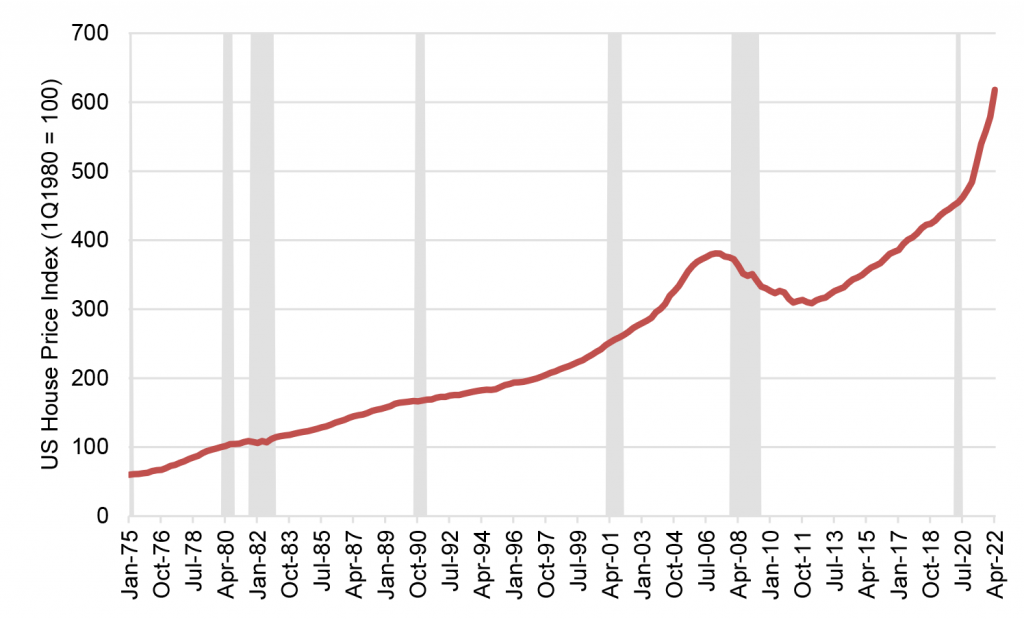

US home price history points to sticky prices on the downside in part because prices rose in five out of the last six recessions, markets presumably when aggregate housing demand fell (Exhibit 1). Only the Great Financial Crisis triggered falling home prices, and that likely was because many homeowners did not have the option or wherewithal to continuing to live in their properties. Many homeowners in the late 2000s could not afford the property—or properties—they bought, and defaults and foreclosures put a steady supply in the hands of banks and securitization trusts that actually did go looking for a clearing price. By early 2008, for example, a fifth of existing home sales came from foreclosures and most of those sold at auction.

Exhibit 1: Home prices rose through five of the last six US recessions

Source: Federal Housing Finance Agency, NBER, Amherst Pierpont Securities

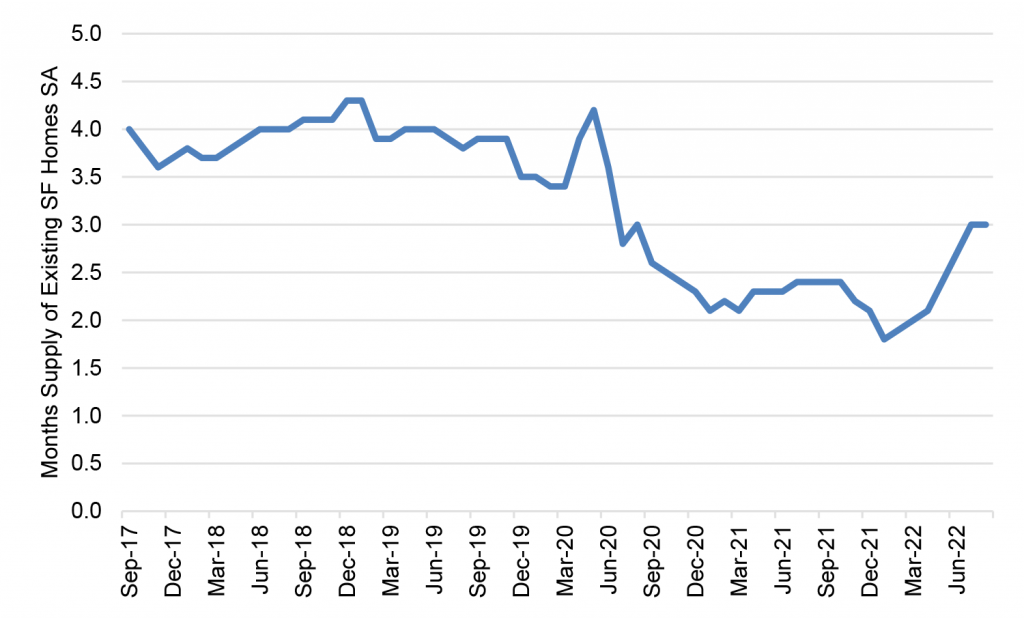

Another sign of a sticky market is the rise in housing inventory when demand falls and sellers keep listing their house at their target price. That has happened in past housing market slowdowns and has started happening again this year with months of housing supply rising from two to three this year (Exhibit 2).

Exhibit 2: House supply has started to rise

Source: Bloomberg, Amherst Pierpont Securities

One more thing especially relevant in today’s market is that stickiness is even more pronounced when mortgage rates move well above the coupon on outstanding loans, according to work done by Karl Case, of Case-Shiller fame, and John Quigley. In that situation, owners have even more incentive to stay in their property and wait for their target price. Case and Shiller describe the counterexample of homes in Vancouver, British Columbia, Canada, that also saw rates rise sharply in the early 1980s. But because most homeowners there had floating-rate mortgages, which imposed a rising cost for staying in the home, more homes came onto the market and prices fell by around 60%.

None of this means that home prices can never go down, of course, especially in local markets seeing the failure of major employers, natural disasters or major population outflows. But on a national basis, home prices have declined historically when owners face circumstances that force them out. And with nearly $4.5 trillion of excess liquid assets stockpiled since the onset of pandemic, according to Amherst Pierpont estimates, it should take a lot to force consumers out of their homes.

The market implications of sticky home prices

Sticky home prices essentially mean the available supply at a true clearing price becomes very limited, inflating the price where home sales eventually do take place. The nominal price of housing ends up looking better than it would in a clearing market.

The market in residential credit is one obvious place where sticky home prices help, mainly by slowing or stopping the erosion of borrower equity that would happen in a clearing market. Even though housing is clearly slowing based on existing and new homes sales, on new homes contracted and delivered by homebuilders and even on recent small drops in home prices, borrowers are likely to sustain a healthy amount of home equity. This should keep defaults and losses well below levels suggested by models trained on the aftermath of the Global Financial Crisis.

The agency MBS market is also likely to get some help from sticky home prices through cash-out refinancing. Most borrowers should continue to see good equity in their homes, perhaps with the exception of borrowers that bought very recently in weak local markets. Cash-out refinancing has become a noticeable component of prepayment speeds this year in agency MBS. And with big parts of the agency MBS market trading between $80 and $90, small increases in prepayments can make a big different in yield, value and return.

Homebuilders also look likely to get some help from sticky home prices, at least to the extent they hold inventory on balance sheet. According to my colleague, Dan Bruzzo, investment grade homebuilders have strong enough balance sheets to let them wait for their target price. Sticky mark-to-market on their inventory should let them continue waiting.

The Fed probably wishes that housing traded in a clearing market instead of a targeting market. That would allow housing to reprice down quickly, tightening financial conditions faster and taking more heat off the rental market. Not the case. That is bad news for the Fed and its inflation fight. It is good news for most investors with housing exposure.

* * *

The view in rates

OIS forward rates now imply fed funds will peak around 4.50% early next year and drift lower in the second half. That is roughly consistent with the September FOMC dots. But persistent shelter and medical care inflation along with tight labor look likely to keep the Fed at a plateau in rates for most of next year. Fade the idea of falling fed funds in the second half.

Fed RRP balances closed Friday at $2.42 trillion, a new record. Yields on Treasury bills into mid-December continue to trade below the current 3.05% rate on RRP cash. Money market funds have little alternative but to put proceeds into RRP.

Settings on 3-month LIBOR have closed Friday at 374 bp, higher by 12 bp on the week. Setting on 3-month term SOFR closed Friday at 359bp, higher by 9 bp.

Further out the curve, the 2-year note closed Friday at 4.28%, roughly fair value based on Fed dots through 2024. The 10-year note closed well above fundamental fair value at 3.83%, so the higher yield has to get chalked up to a market seeing or expecting supply to overwhelm demand. So far, the source of selling is unclear.

The Treasury yield curve has finished its most recent session with 2s10s at -45 bp, steeper by 7 bp on the week. The 5s30s finished the most recent session at -31 bp, steeper by 6 bp on the week. The 2s10s curve looks likely to invert by around 70 bp shortly before Fed tightening comes to an end.

Breakeven 10-year inflation finished the week at 215 bp, down 22 bp from a week before. The 10-year real rate finished the week at 168 bp, higher by 62 bp.

The view in spreads

Volatility should continue while the Fed’s path stays in flux. Both MBS and credit have widened steadily since mid-August. Nominal par 30-year MBS spreads to the blend of 5- and 10-year Treasury yields finished the most recent session at 172 bp, wider by 7 bp on the week. Par 30-year MBS OAS finished the week at 62 bp, wider by 6 bp on the week. Investment grade cash credit spreads have finished the week at 187 bp over the SOFR curve, wider by 17 bp.

The view in credit

Credit fundamentals have started to soften with the weakest credits showing slower revenue growth so far in 2022, declining free operating cash flow and less cash on the balance sheet. Ahead lays weaker demand, margin pressure, a soft housing market and various risks from Covid and supply interruptions. Inflation will land differently across different balance sheets. A recent New York Fed study argues inflation generally helps companies lift gross margins, although airlines and leisure may have an easier time passing through costs than healthcare, retail and restaurants. In leveraged loans, a higher real cost of funds would start to eat away at highly leveraged balance sheets with weak or volatile revenues. Consumer balance sheets look strong with rising income, substantial savings and big gains in real estate and investment portfolios. Homeowner equity jumped by $3.5 trillion in 2021, and mortgage delinquencies have dropped to a record low. But inflation and recession could take a toll and add credit risk to consumer balance sheets.