Uncategorized

Latin America | Choose wisely

admin | November 20, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Excess global liquidity and tight emerging markets spreads once again have biased investors toward high carry returns heading into 2021. But investors should choose wisely among the high yielders. Post-Covid fundamentals are much weaker, with rating downgrades and higher debt ratios. The market has already seen sovereign debt restructurings in Argentina and Ecuador with bondholders mostly providing liquidity rather than solvency relief. The overhang of default risk should persist into next year for countries that have just restructured their debt, such as Argentina and Ecuador, and for others, such as Costa Rica and El Salvador, that suffer from liquidity and solvency stress.

Similar to last year, 2021 starts with assessing default risk. It will require difficult political commitment to austerity with only a slow economic recovery ahead. The negotiation for formal International Monetary Fund programs could provide a relief rally on prospects of near-term liquidity. However, the high execution risk that comes with overly ambitious IMF programs may encourage selling into strength. This does not set the stage for passive carry returns in the ‘B’ credits but rather for an active strategy reflecting the fluid process needed to avoid default. Uruguay is the outlier for passive carry returns with Global local UI bonds offering potential diversification of external risks and persistent high inflation. Amherst Pierpont’s top picks for 2021 are El Salvador Eurobonds, positioning for the positive event of an IMF program, and Uruguay inflation linkers, for high carry returns. We remain most cautious on Costa Rica for domestic rollover risk.

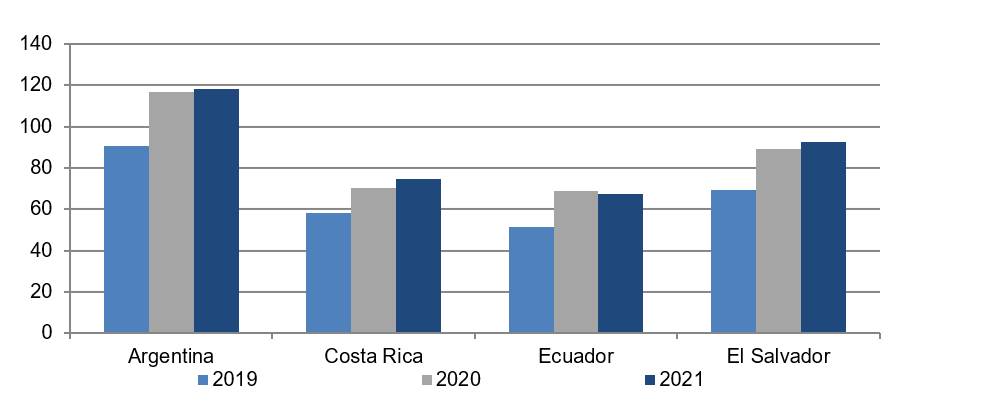

Exhibit 1: Gross public debt as a percent of GDP

Source: Bloomberg, official sources, Moody’s net (+) one notch upgrade and (-) one notch downgrade

The restructured credits struggle with solvency

Argentina

The Eurobond prices in Argentina at $30 to $40 do not show much if any relief after debt restructuring. There is a high implied risk of a future default. Argentina is unique for a credit that refuses to commit to policy orthodoxy and struggles with suboptimal growth, high inflation and a full-blown balance-of-payments crisis. The crux of the problem is the political coalition with Kirchnerismo and an ideology that favors a public consumption growth model with excessive spending and deficit monetization. There are no near-term debt payments. The challenge is whether Argentina can accumulate sufficient foreign exchange reserves over the next three years to honor future debt repayments. The zero coupons offer zero carry with Eurobonds representing a long-term option on whether the country avoids default through heavy amortizations in 2024-2028. There is low conviction of success on muddling through with piecemeal pragmatism.

Next year should determine whether the balance of payments deficit shifts to surplus. This will determine whether or not current low bond prices offer upside optionality and whether trapped long investors buy or sell into the strength. Argentina has not been immune to the risk-on rally with favorable externals allowing a bounce off the price lows as the cheapest credit in the region. We remain skeptical on the ideological constraints that discourage capital inflows, encourage capital outflows, thwart FX reserve accumulation and reaffirm low growth. This perpetuates the illiquidity risks and high debt ratios that threaten future debt repayment. The Fernandez administration faces ideological, election and cyclical constraints for slow economic recovery ahead of elections next year. The game changer would be a policy reversal towards orthodoxy and a breakaway from the Kirchnerismo coalition as President Fernandez suffers from declining popularity and a political setback after midterm election defeat.

Ecuador

Ecuador Eurobond yields have mostly normalized at 10% following restructuring, thanks to the anchor of an exceptional IMF access program with front-loaded funds. The access to external credit along with debt relief from bondholders provides breathing room on liquidity. But Ecuador still has a debt problem. The country has high debt ratios and a high structural fiscal deficit. The IMF program targets an ambitious fiscal adjustment of 5% of GDP. The crux of the adjustment is a proposed VAT hike that would only kick in at a mature phase of cyclical economic recovery. The policy management after upcoming elections is critical. That should determine whether there is commitment for the IMF program. It is binary event risk between the center right CREO candidate and the Correista candidate. The path towards debt sustainability requires both smooth political transition and broad political commitment to controversial tax hikes.

The coming year should also determine whether Ecuador can commit to the tough fiscal austerity necessary to defend dollarization. The frontrunner status of CREO candidate Lasso and an influx of multilateral funds that should reduce budgetary and economic stress both look constructive. However, the prospects depend on polls and whether candidate Lasso maintains a significant lead. The current bond yields on the ECUA’40 discount perhaps a 65%/35% outcome Lasso/Arauz if we assume binary outcome of 8% yields for Lasso against 15.4% yields for Arauz (30 cash price) or perhaps a closer race at 55%/45% if we assume a less worse Correista reaction at 14% yields (40 cash price). This seems reasonable considering the latest polls and warrants a neutral recommendation. It is difficult to have high conviction on the typically unreliable polls and the high election stakes. The investment strategy will remain opportunistic depending on the polls, with a bias to sell into strength on what remains high execution risks even under a favorable electoral outcome. The near zero coupons deliver almost zero carry returns with the upside optionality depending on not only a centrist candidate victory but commitment to ambitious fiscal reform.

The ‘B’ credits and commitment to IMF programs in 2021

Costa Rica

Costa Rica faces imposing deadlines for society to commit to an IMF program. The current normalized yields of 7.6% to 8.4% seem complacent. There is risk of a domestic funding accident and broader economic stress. There has been wide discussion about the fiscal problem but no consensus on spending cutbacks and tax hikes. The timing could not be more inopportune with only a sluggish economic recovery so far. The delays and indecision could backfire with large gross financing needs next year at 15% of GDP. It is not necessarily a question about default on Eurobonds that represent only 10% of GDP. But rather the mark-to-market risk for a country that may face a domestic funding crisis if locals are unwilling to rollover the large gross funding needs.

It is difficult to measure saturation risk, but more important is the willingness of locals to fund the government if there is no progress on the fiscal adjustment plan or if the proposals shift towards progressive measures like distressed debt exchanges. The next deadline is the November 21 conclusion of the “multi-sector dialogue of 805 proposals.” The track record back in late 2018 shows that consensus for fiscal austerity is only possible in moments of financial stress. The jitters are already visible through foreign exchange weakness and foreign exchange reserve loss. The legislative rejection of an IADB loan reaffirms complacency about large financing risks and limited access to external credit. It is complacent to think that local investors will continue to fund without a solvency plan, especially if local debt is at risk for a distressed exchange. The risk-and-reward balance is not attractive for the spread discounts to ‘B’ peers considering the uncertain commitment to fiscal adjustment and high execution risk. The market should assume high rollover risks on the prospects of a funding accident with risks for curve inversion and double-digit yields.

El Salvador

El Salvador is Amherst Pierpont’s top pick and a relative overweight to a Costa Rica underweight. El Salvador trades with 100 bp to 300 bp spread premium and still an inverted and distressed curve with 9% to 11% yields. There has been a lot of speculation on whether President Bukele will commit to an IMF program. For weeks, the Bukele pessimism has been overdone. The high yields are quite compelling with positive optionality from an IMF program. The better question is why would President Bukele reject an IMF program? That’s the more difficult argument to rationalize. The alternative is trying to source enough non- IMF multilateral loans (think Ecuador after 2009 default) to avoid the forced austerity of cutbacks to an underfunded budget and minimal sources of domestic funding. The worst options are high risk strategies that could threaten dollarization and backfire into economic crisis and political suicide. The bottom line is that dollarization forces pragmatism. You can’t spend what you can’t borrow, and external credit is only accessible through policy pragmatism. There are a lot of lessons learned from Ecuador with center left Moreno administration forced into pragmatism to defend dollarization. This reinforces a bullish view of positive event risk following elections if the country confirms intentions for an IMF program. That should create normalized yields and bullish curve flattening. The execution risk of an IMF program might also decline if governability improves post-elections and economic recovery matures.

The high inflation carry trade

Uruguay

Uruguay remains our top pick for high carry with near-10% returns. There are not many high carry and low volatility alternatives across local or external debt markets with a dominant trend of negative global rates. Global local bonds, and specifically inflation linkers, are the exception on prospects for slow improvement of structurally high inflation and low foreign exchange risk for diversification from global financial markets. The solid investment grade credit fundamentals and risk-on trade should provide an anchor for the foreign exchange rate on what has been mostly sideways price action that allows investors to maximize foreign exchange-adjusted returns. The breakeven inflation (UYU28/UI’28) has recently reached a plateau at 5% with no room for disappointment on an aggressive 5% inflation target and yet still high 7% actual inflation. The BCU survey expectations have also reached a plateau at 7% for 12- and 24-month forward inflation to coincide at 7% annualized monthly inflation rates. The risk-and-reward favors the UI linkers for higher potential carry on inflation inertia as expectations stabilize at 7% against low breakeven inflation of 5% and UI bonds also offering defensive characteristics on partial hedge to foreign exchange risk.