Uncategorized

New Ginnie Mae pooling rules cut incentives for buyouts

admin | July 10, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Ginnie Mae took action on June 29 to reduce the risk that mortgage servicers might buy loans in forbearance out of MBS pools and drive up prepayments. The agency has acted in the past to limit occasional prepayment risk, but the most interesting aspect of the recent move was the decision to target servicers’ profits from buyouts. The outsized returns available under the old rules should fall sharply for all servicers and especially for non-bank servicers. But banks could still see enough profit to stay in the game.

Ginnie Mae servicers under the agency’s old rules could buy a loan in forbearance out of a pool after three missed payments and immediately repackage it into TBA-eligible MBS. Now servicers will have to wait at least six months after the buyout to resecuritize those loans into pools that may trade at a lower price than TBA. This sharply lowers potential profits from buyouts, helping address investor concerns that servicers will buy out loans and generate fast prepayments.

Concern about buyouts has increased with 11.5% of Ginnie Mae loans in Covid-19 forbearance as of June 1. Many FHA loans with forbearance will likely cure after having their missed payments deferred at zero interest until the loan matures or pays off. If the loan is in an MBS, it can remain in the pool since the loan terms do not change. However, Ginnie Mae gives servicers the option to buy out delinquent loans after three months since servicers must advance principal and interest for as long as a loan is delinquent. It is likely difficult or even impossible for Ginnie Mae to unilaterally alter this option on existing pools.

Ginnie Mae last week instead opted to change requirements for new pools, making it less economical to buyout loans. For loans that entered forbearance on or after March 1, are bought out on or after July 1, and subsequently cure without a modification, new requirements apply:

- Pay history. These loans must make six consecutive payments immediately preceding resecuritization.

- Custom pooling. These loans will not be eligible for delivery into TBA-deliverable pools. Ginnie Mae is creating a new custom pool type, “RG”, to hold these loans.

- Seasoning. The new pool must have an issue date at least seven months after the loan was last delinquent.

Modified loans, which could include many VA loans, can still go into TBA-eligible pools as soon as the borrower completes the trial plan. But modified loans should constitute a small percentage of FHA loans coming out of forbearance since the deferral option is easier for the borrower and has no impact on the borrower’s credit score.

Conversations with servicers identified the requirement for six months of clean payment history payment and potential delivery into RG pools as the biggest hurdles. Holding these loans for an additional six months substantially lowers the return on capital invested to repurchase the loan. Requiring custom pooling likely reduces the premium earned when resecuritizing the loan. Custom pools have lower liquidity than TBA-eligible pools and should trade at a discount to TBA.

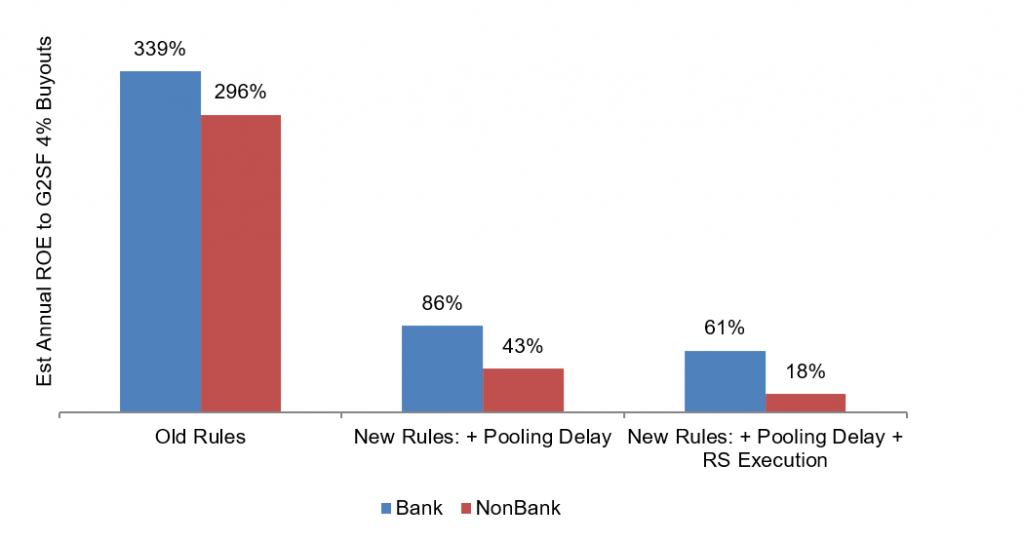

The impact of the new rules shows up clearly in the estimated return on equity from buyouts for banks and non-banks. Banks under the old rules, with a lower cost of funds, could earn an estimated annual ROE of 339% from FHA buyouts in 30-year 4.0% pools with non-banks earning 296% (Exhibit 1). The requirement to delay pooling for six months cuts bank ROE to 86% and non-bank ROE to 43%. Selling the loans into pools that trade $1 below TBA—or at $105-00 in the case of G2SF 4.0% pools—further reduces bank ROE to 61% and non-bank ROE to 18%. Returns would fall further on buyouts with lower coupons since proceeds from resecuritization would fall as well. Banks would have to see above $103.40 to hit a 20% ROE.

Exhibit 1: New pooling rules sharply lower likely returns on G2SF 4.0% buyouts

Source: Amherst Pierpont Securities

Estimated return on equity from any buyout depends on a host of important assumptions (available for download in the spreadsheet here):

- Time to cure. The faster a loan cures, the faster the servicer receives proceeds from resecuritization and the lower the expenses for financing, hedging and administering the loan. For a pool of loans in forbearance, a servicer needs to make some assumption about the share that will cure in anywhere from one to 12 months, although the servicer can only buy out loans that take more than three months to cure.

- Time to repool. The faster a servicer can repool and sell, again the faster the servicer receives proceeds and the lower the expenses for financing, hedging and administering the loan. The servicer can offset some expenses with the carry from holding the loan between buyout and resecuritization.

- Cost of funds. The lower the cost of funds, the lower the lower the cost of holding the loan to resecuritization. The impact of cost of funds compounds over time.

- Advance rate. The higher the advance rate for financing buyouts, the lower the equity required for the buyout.

- Hedging costs. The servicer needs to hedge against the risk that the future TBA price declines. The longer the time to resecuritization, the higher the hedging costs.

- Repooling price. The higher the coupon on the loan, the higher the proceeds from resecuritization. These loans now must be sold into custom pools, which may trade below TBA.

- Not every loan will cure, which lowers the return. While the servicer faces this cost whether or not they buyout a loan, entities considering financing buyouts need to consider the return including losses.

- Fees and expenses. Servicers can incur a variety of other costs to administer loans in forbearance and to mitigate losses on loans that eventually default.

Under the old Ginnie Mae rules, a bank servicer could buy out loans from Ginnie Mae II 4.0% pools and potentially earn a 339% return on equity under some reasonable assumptions:

- That half the pool would cure within three months after buyout, and the rest between four and nine months

- That the servicer could repool immediately

- That the bank’s 0.73% cost of funds matched the average cost of larger FDIC-insured banks at the end of the first quarter this year

- That the bank funded the pool with a 95% advance rate

- That the annualized cost of hedging matched the annualized carry on G2SF 4.0% TBA contracts

- That the servicer could sell into a TBA pool at $106-00

- That average losses on all loans would amount to 1%, and

- That fees and expenses would amount to 2.5% of principal balance

By changing the delay before repooling to six months, the ROE falls from 93% to 86%. And by changing the pool execution to $105, the ROE falls further to 61%.

For non-banks, a higher cost of funds drives returns down dramatically. A typical warehouse funding line costs 3.00%. Under all the other assumptions used for banks and assuming six months to repool and pool execution at $105, the ROE is 18%. For buyouts at lower coupons, ROE would likely fall below a non-bank servicer’s cost of capital.

The new rules have clearly changed the incentives for buying loans in forbearance out of Ginnie Mae pools, especially for servicers with relatively high costs of funds. Since more than 71% of Ginnie Mae servicing sits in non-bank hands, the rules should protect a healthy share of the market. Servicing in the hands of banks, especially servicing on 4.0% and higher pools, still looks vulnerable.

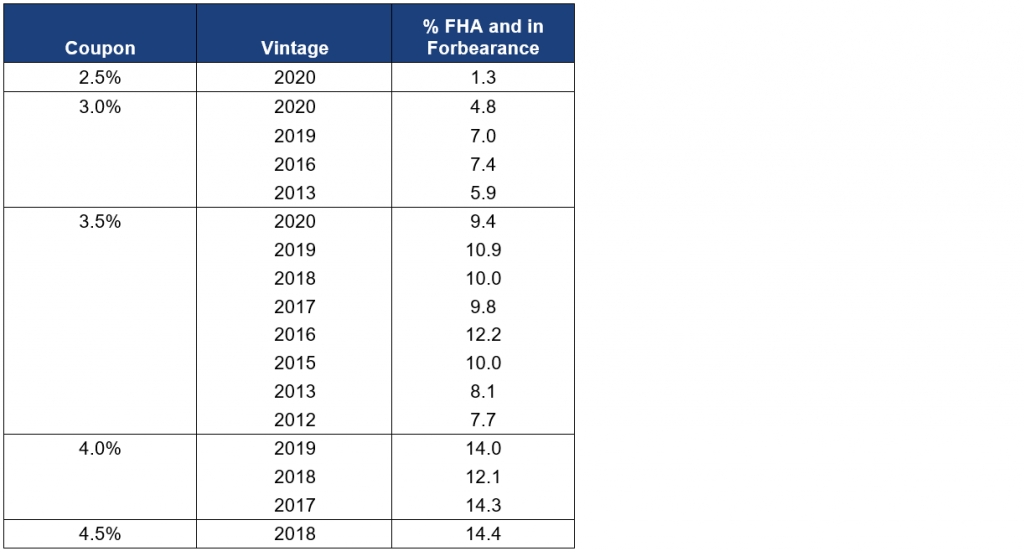

Overall these changes should be a positive for Ginnie Mae pools across the stack. Low coupon pools should be the least attractive target for buyouts, but contain fewer loans in forbearance. Higher coupon pools could benefit the most, since these pools have a higher share of FHA loans that are in forbearance.

Exhibit 2. Higher coupon pools have more FHA loans in forbearance

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

Servicers may be worried about pressure from Ginnie Mae if buyouts push prepayment speeds up too fast. For example, in 2018 Ginnie Mae suspended some lenders from selling their VA loans into multi pools due to fast prepayment speeds. Lenders would have to factor in the potential cost to their ongoing origination business if Ginnie Mae took similar action on forbearance buyouts.

The Ginnie Mae announcement is here and their discussion of the changes is here.